December’s monthly update is here with a few tweaks and improved graphics, as well as an article redesign. I am aiming to focus a bit more on ‘accuracy, brevity and clarity’ in these updates on the advice from my website mentor, so expect to see me pare these updates back and leave you with the good stuff: the juicy goss, my progress to financial independence and my financial portfolio – all the information you came here to see.

December update

Unfortunately my sabbatical has come to an end, and I have made the trek back to NSW to return to work. Ahead of me is a month or more of gruelling simulator training, late-night study sessions, and some stressful operational line checks. Still, the trade-off for this time and hard work commitment means money, which will be welcome after a long-ish period of reduced income. It also means I get to take to the skies again – and boy oh boy have I missed advancing those throttles and having my powerful engines thrust me skyward! (It is honestly a rush only those who have flown will understand – and I highly recommend you do it at least once in your life!)

I have debated with myself whether I should share this publicly or not, but I think I will feel better if I do…

After some long, and fairly heated discussions with my father, it looks like we won’t be seeing each other any more. Only two weeks out from his hospital discharge, and after hundreds of thousands of dollars in public taxpayers’ money spent on his 7 major surgeries (including several amputations, heart and artery operations), about 2 months of hospital stays and 18 months worth of chemo (costing $6000 per month fully funded by the PBS – my eyeballs watered when I read the script prices), he was back home and falling back into bad habits – the smoking, drinking, diet abuse (diabetic), and other unsavoury behaviours have returned.

Unfortunately, I left the farm fully understanding that it could be the last time I ever see him. I stacked up as much firewood as I could fit into his box and made tracks. I don’t know if it is his twisted sense of humour, or just a lack of ability to communicate, but the last thing he said to me was “alright fuck off then, sms me when you get to Melbourne” – and then no reply when I messaged him. Seems very reflective of our entire relationship.

Still. That is not the thing that is bothering me.

The thing that is bothering me is how 2020 had one final sting in its tail. Something that brings me to tears to even type. On NYE, my beautiful mum went in to hospital for her most recent chemo session only to be told “your cancer is incurable.” Four words that have me feeling like a lost little boy again. My sister rang me to tell me the news, what felt like only minutes after I got through the door to my apartment in Sydney.

I don’t know how to fully explain this, but despite what you might think of me and what is essentially a highlight reel I seem to publish here, I’m actually a bit of a fuck-up in real life. I bounced between schools with expulsion after expulsion (I think the number is 17) due to behavioural issues, have been through juvenile behavioural therapy a number of times (and, no, ‘juvy’ is not what you think it is), I am more familiar with the back of police cars than I would like to admit, and somehow I manage to ruin every romantic relationship I get in to.

Through it all, my mum was always there for me. She always nurtured me, supported me, helped to raise my self esteem. She sacrificed so much of her time, life and energy and is such a devoted mother for our family. She received bugger all help from my dad who did not contribute financially or otherwise, and yet she still made it happen and never complained. You have to understand that my mum is just the most amazing, beautiful soul and lovely person you would ever meet. So to hear those four words just crushes me.

A ‘big night in’ planned with friends for NYE turned to basically just crying on the couch alone all night. Not the kind of flashy thing you want to advertise on your blog, or on Instagram, huh? Since then I have kind of fallen into a bit of a heap, and not really done much. Seemingly on cue, I have managed to pick up the sniffles meaning getting a COVID test and self isolation. As a very social, extroverted person, I dislike this situation.

With borders being closed to NSW, me being sick, and needing to return to work, things do feel a little overwhelming right now. However, This is exactly why I have been working towards Financial Independence. I am drawing my plans to return home – and will be applying for roles closer, potentially looking at being rostered in the same state at least! But, of course, COVID has made anything in aviation incredibly difficult and to be honest I am lucky to still have a job.

For now, since I can’t do anything else, I am working as hard as I can on both regaining flying proficiency and Financial Independence, while we wait for more specialist medical advice regarding my mum’s health. For now, the docs will continue her treatment to prevent the spread and try to shrink the cancers, and as far as we know this will be an ongoing thing required for the rest of her life.

So, with that out of the way, I guess you probably want to dig into some more of the financial stuff!

End of financial year tax return is still outstanding…

Yeah I can’t believe I still haven’t done this… now that I am back in Sydney, I have printed my Sharesight tax summary for the 2019-2020 financial year and am booked to take this down to the accountant. Hopefully I will get some money back which will be much needed, since I have been a bit spendy and haven’t been earning much lately.

Saving rate: 84%

My saving rate in November across all of my accounts was 84%. Again, I am surprised I managed to keep it this high, based on the large amount of spending and travelling. However, I did not pay for accommodation as I stayed with family and friends at each location (usually in exchange for some labour in the form of doing certain DIY or renos) which meant all I really had to pay for was fuel and food.

Income

Income was down in December, of course, due to not working (however I am now back in Sydney and scheduled to go back to the simulator soon). Also, income from the websites was down a bit due to a bit of a drop-off in the traffic. Curiously, this was also replicated across my social media channels. This is likely due to a combination of the latest Google and Facebook algorithm updates, as well as people going on holidays and spending time with family (and not reading about FIRE lol). I also made some more money by selling things, as well as picking up some casual contract work.

Spending

Spending in December was above average, especially because of Christmas, and Travel back to Sydney. I am too scared to check my budgeting app for the accurate breakdowns, but it was reassuring to know I only spent around 16% of my reduced income on these things.

Investing decisions: $7420

This month I invested $7420 across mortgage principle repayments and the websites.

Embarrassingly, I missed the boat on shares this month. I didn’t have any surplus cash left over after the property and the websites, and so I didn’t make any share purchases. I’m kicking myself about this but honestly just lost track of time and prioritised the money going into my website business.

Property

I paid $1,000 into the property project. Nothing special here, this is just my normal additional ‘build + mortgage’ commitment.

P2P lending

I did not do any P2P lending this month. Once I have some more surplus funds, Plenti Peer to Peer lending will be my P2P platform of choice.

Business

$6420 went back into the business. This month I invested in a bunch more awesome tools, some more educational content from from the eBusiness Institute, as well as wages on contractors and services for the website portfolio. The majority of the money is going into this website, followed by one other specialist site, and then the remainder is equally spread into three ‘starter sites’. I also have partial interests in some other sites which are jointly owned and ticking along nicely being managed externally – so no need to invest any of my time or money into those – as passive as it gets!

This is basically just Exchange Traded Index Funds and Listed Investment Companies. In my mind, this is a ‘defensive’ asset that I am building as ‘insurance’ (ironic, given most financial advisers say that shares are aggressive) so that I can then go ahead and invest in other, more risky ventures such as the websites and property development (spoiler alert – probably avoid property development).

The aim of the Financial Independence portfolio is to provide a solid base of income to cover my cost of living from Early Retirement until the time I can get my superannuation ‘conventional retirement’ benefits – through a combination of dividend income and selling small parcels of shares (expecting roughly 4% dividend income, and then to sell 3% of the portfolio value each year to supplement dividends).

The Financial Independence share portfolio is split across the three share trading platforms that I use (the link will take you to my dedicated review of each):

I track my share portfolio using Sharesight, which means my portfolio accounting is completely hands free. I have got automatic trade confirmation emails set up with SelfWealth, and am using the API plugin with Pearler. This means I pretty much just need to log in to confirm all the trades and dividends over the year when needed for my tax return, and also to produce these monthly updates for you guys. The following section contains Sharesight reports for:

- Monthly

- Rolling 12 months

- Since inception (since I started tracking it with Sharesight)

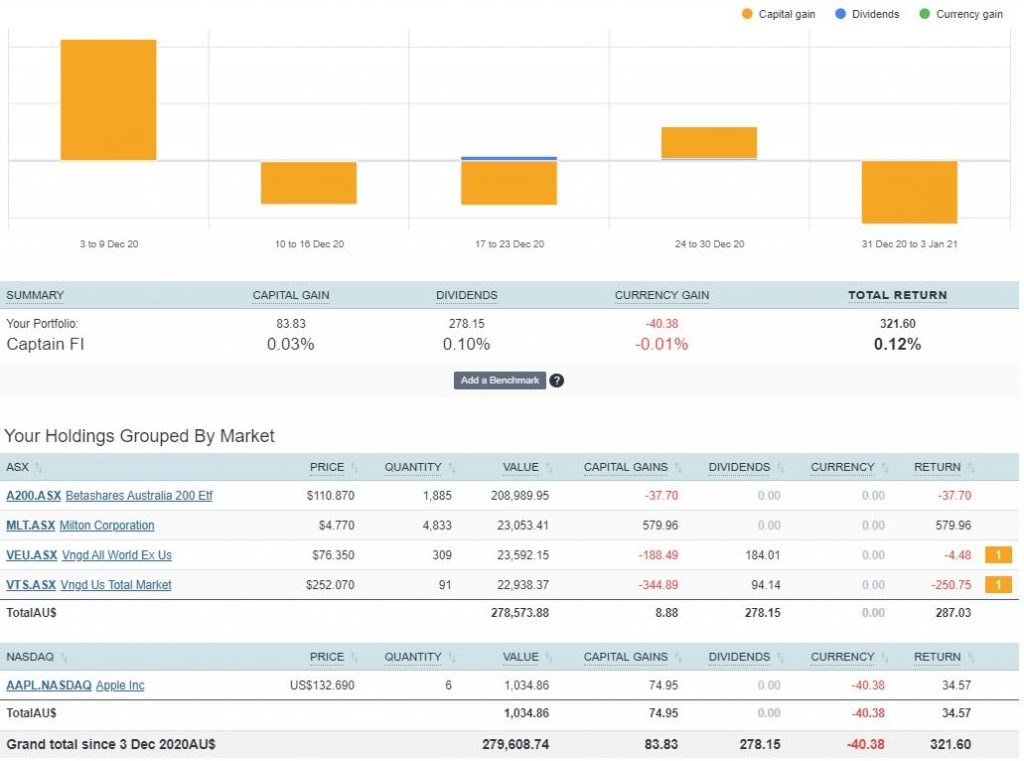

You might see something a little strange in this month’s share portfolio update (something that rhymes with schmapple) due to me testing something out for SelfWealth with my own funds – but rest assured I have already put in an order to ‘kill my darling’, take a nice 10% profit (14% capital gain less 4% currency loss on the USA to AUD front due to a weakening Aussie dollar) and then shove it into index funds.

From the Sharesight reporting, not much happened here. Some rallies early in the month, offset by drops in the rest of the month. Nearly $300 in dividends (ex-dividend date around the 20th or so) which will drop into the brokerage account at some point to be reinvested with January’s share purchase.

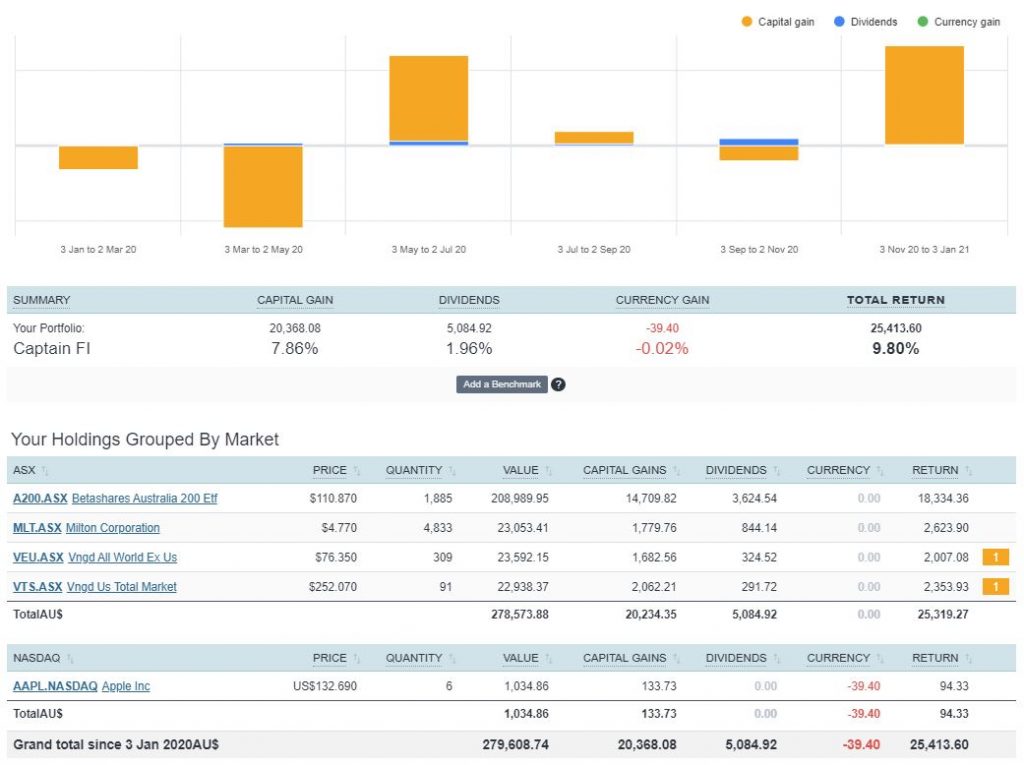

The rolling 12-month figure shows market returns roughly in line with the long-term average of around 10%. But what a wild ride it was in 2020! The figures show roughly 8% capital gain and 2% dividends – which I think is probably because dividends got cut due to the COVID issue (and this was mostly Australian banking dividends due to government regulation). I am sort of expecting the long-term dividend split to probably be closer to 4% and capital growth to be another 6% on top of that – but who knows!

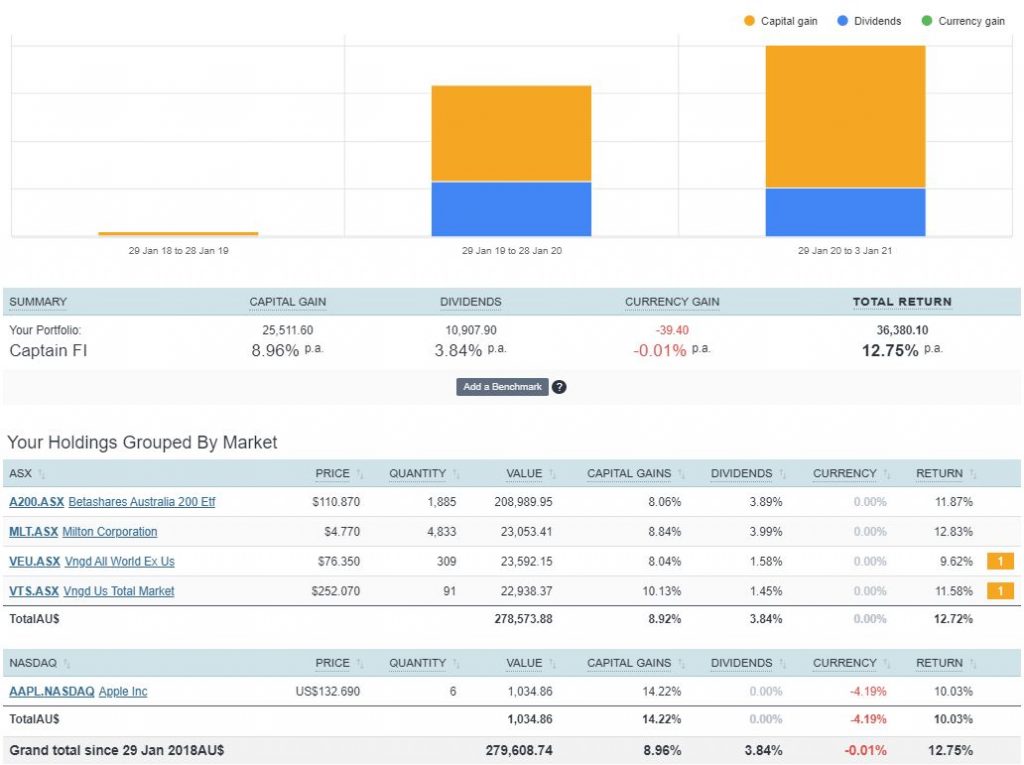

This is the total return since I started using Sharesight to track my portfolio, and switched to a core holding of A200, VTS and VEU complimented by LICs (currently Milton). Don’t let the returns on this graph fool you – history is written by the winners here. What you don’t see is me underperforming the market prior to 29 Jan 2018 when I was trying to pick stocks. Overall, nearly a 13% gain which is good – but I expect the long-term trend to be a bit less and closer to 10%.

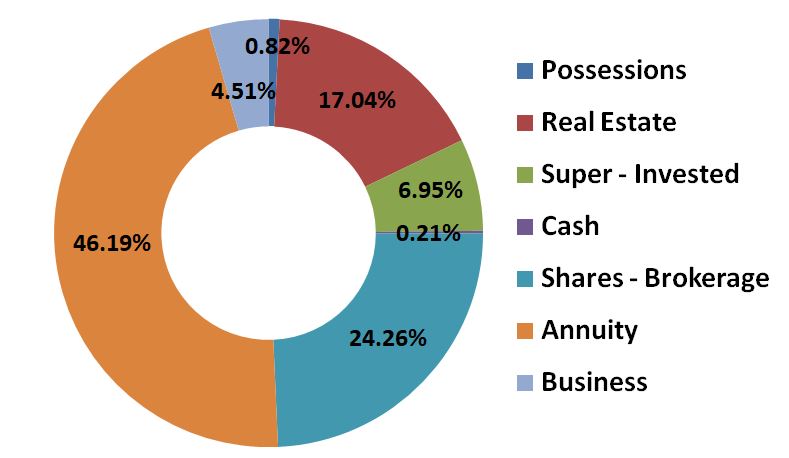

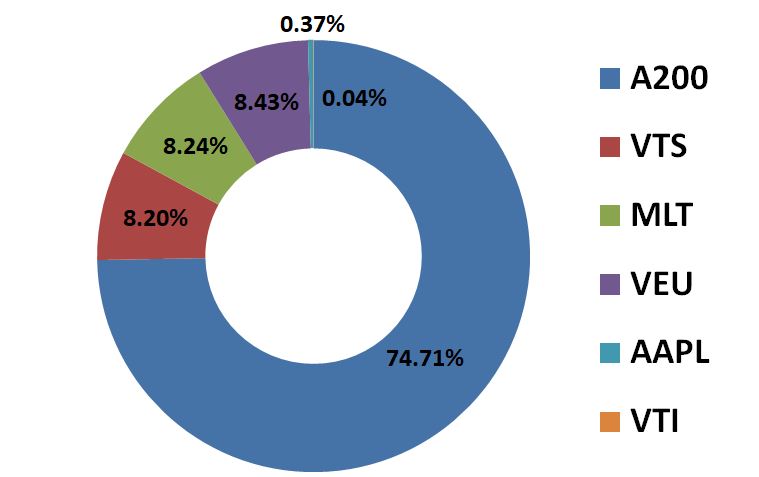

Pie chart

Because sometimes you just need a pie chart to visualise what the portfolio looks like. For your viewing pleasure I cut out a hole in the middle of the pie this month.

Investment Property

Literally nothing has happened with the investment property and for all intents and purposes it appears to be just a black hole that I throw money in to. Still… “HOLD” is the advice I get from my team of ‘co-investors’ on the joint venture. As soon as DA is approved, we will be able to move earth and pour the slab and will surely see some progress.

Had I known the project would have taken this long (as in… 6 months delays before we even started, the theft and the site vandalism) I may have reconsidered this whole process. Nevertheless, wheels are in motion – but I can’t help but feel a little ‘helpless’ about it all. This is one of the reasons I like shares and businesses as my preferred investment vehicles: I have full ownership and control of direction.

P2P lending

Earlier this year I withdrew all of my P2P funds from Plenti. This was because my budget was a bit tight and I needed to deploy those dollars. I also don’t really need any ‘fixed interest’ at the moment and if I am honest, it was more of an experiment than anything. I do like P2P lending because it gives me a higher interest that I would get from my online bank account, and investing in the long-term markets can actually be a way to create your own income stream.

Business portfolio

This has been a hot topic and the source of some great debates over the past few months since I let the cat out of the bag. I also wrote a dedicated article about how I make money online, as well as interviewing Matt and Liz Raad from the eBusiness Institute on the CaptainFI podcast about online business and how I started and am growing mine.

I have started to shift from trying to do everything myself and have embraced the benefits of outsourcing and the use of contractors. I probably went a little bit overboard, however since $6400 went into the business in December. This was way more than I expected!

Unfortunately I did not reach my goal for 2020 of a monthly revenue of $10,000 – but I will be continuing this goal into 2021, and I am quietly confident to reach it by mid year. Currently it is hovering around $2000 per month. I have been working on a lot of ‘core’ areas such as layout, corporate structure, content plans, writers, graphic designs, and social media across the portfolio – and the final piece in the puzzle is the income from affiliates and sponsors – which is something I will be working on as a priority over the next few months to bring the business into a positive cash flow state.

Retirement

I am still working toward my ‘Family FIRE’ goal of $6,000 per month (after tax). When looking at the future trust structure, to earn $6,000 per month after tax it will more or less take $6,800 of gross portfolio income. Currently, with some gains in December from the business income I am still conservatively at $3300 out of the $6,800 goal, or almost halfway to ‘Family FIRE’!

It is worth noting though, I am not actually taking any money out of the business (or my share portfolio for that matter). I am reinvesting this money to grow this revenue stream faster to secure Financial Independence sooner – as you can read my dedicated transition to retirement financial planning process article.

However, as a good quick and dirty, I plan to live off a 7% draw-down of my Financial Independence Share Portfolio (4% dividend and 3% selling parcels of shares each year) from when I choose to start early retirement, through to when I am eligible to receive my superannuation lump sum payment and my annuity starts paying me.

So how do I value my superannuation? Well it is an interesting topic and up for debate (let me know your opinion!).

The invested portion is super easy – it is literally just all invested in shares (Australian and international shares) in index funds. If I contribute nothing more and let it tick away, I will have just under $1M by preservation age. To get to the $1.6M cap, I could either stuff in another $50K to super right now, or closer to $70K of contributions over the next 2 years or so (which I am on track to do and reach before FIRE thanks to compulsory 9.5% wage input).

My annuity component is a pension that is indexed to CPI for life, and it is a bit trickier to value. The Australian average male life expectancy is 82 years, and I think I can eke out a few extra years on that based on my health and lifestyle habits of weightlifting, cardio exercise, a (mostly) plant based diet, minimal alcohol consumption and yearly comprehensive medicals. I think at least 30 years of the annuity payments is a safe bet. When I looked online and got some quotes for this, the prices ranged from 25x to 30x annual payments. Interestingly, the Australian Tax Office values my annuity income stream product much less than this, and I am not sure if this is counted towards my $1.6M super cap or not.

I therefore conservatively value my annuity at 25x annual payments, which coincidentally is also in line with the 4% rule from the Trinity Study regarding investment portfolio balances and retirement.

Captain FI net worth Dec 2020

The net worth pie chart is a great visualisation of my total financial portfolio breakdown. Weirdly enough, these splits seem to stay roughly the same, despite each sector growing at a different rate (bearing in mind these are rounded up to the closest percent for ease of visualisation).

Captain FI net worth progression

Tracking your net worth over time is one way to monitor and compare your progression to FIRE. A better way though, is to track your passive income – such as dividend income. Because that is what you are going to be using to live off if you do choose to retire early.

Because of how I have my finances structured as an Australian investor with a significant amount invested in superannuation, my net worth number isn’t really all that reflective of my ability to FIRE, but I still think it is an important metric to track since its growth is representative of performance – the rate of change of net worth is more important than net worth by itself, in my opinion.

Eventually, I will produce a second graph below which will track my passive income over time – something I don’t have data on (except for perhaps going back over these blog posts maybe).

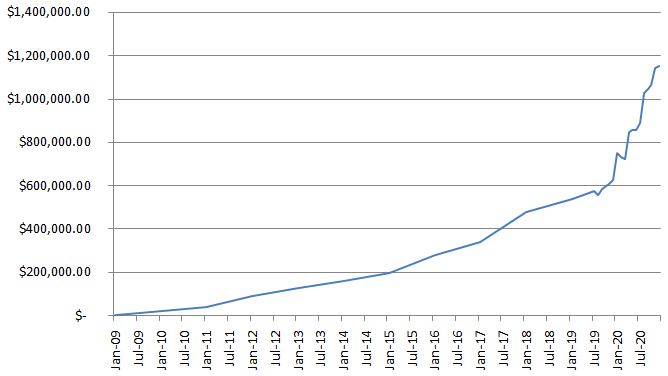

CaptainFI net worth progression – graph

The net worth progression graph is rather crudely constructed in Excel, but still demonstrates the ‘somewhat exponential’ journey over the past 12 years.

CaptainFI net worth progression – table

I decided to include a net worth table which provides a bit more information on my journey for anyone wanting to go back and see how individual years or months went at a quick glance.

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jan 09 | $5,000.00 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK | |

| Jan 10 | $24,000 | +$19,000 | ? | Estimate NW | LINK |

| Jan 11 | $40,000 | +$16,000 | ? | Estimate NW | LINK |

| Jan 12 | $92,000 | +$50,000 | ? | Estimate NW | LINK |

| Jan 13 | $130,000.00 | +$38,000 | ? | Estimate NW | LINK |

| Jan 14 | $161,000.00 | +$31,000 | ? | Estimate NW | LINK |

| Jan 15 | $200,000.00 | +$39,000 | ? | Estimate NW | LINK |

| Jan 16 | $281,000.00 | +$81,000 | ? | Estimate NW | LINK |

| Jan 17 | $340,000.00 | +$59,000 | ? | Estimate NW | LINK |

| Jan 18 | $482,000.00 | +$142,000 | ? | Estimate NW | LINK |

| Jan 19 | $542,000.00 | +$60,000 | ? | Estimate NW | LINK |

| Jul 19 | $578,900.00 | +$36,900 | 84% | Finally began tracking NW this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! Became Single again. | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘corona crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! | LINK |

| May 20 | $857,859 | +$10,836 | 92% | Some Great sales as I let go of my Super Sport Motorcycle, Some gym gear, expensive flying equipment and a few other various bits and bobs and invested this money. Flying still reduced, but increasing from April. The share market grew as I continued to make my fortnightly investments. I also wrote down the ‘value’ of some of my possessions (liabilities) such as my car, tools and furniture by around $10K to align them to market price (“tell him hes dreaming…!”). | LINK |

| June 20 | $858,650 | +$791 | 90% | Small Net Worth gain as I continue to declutter and simplify my life, despite being off work due to a family emergency. Share market not doing much. | LINK |

| July 20 | $888,218 | +$29,568 | 68% | Majority gain due to share market going back up, low spending due to being on the family farm and at home because of lock down. | LINK |

| Aug 20 | $1,029,293 | +$141,075 | 74% | Became a millionaire. Achieved this massive milestone I set out for myself in Dec 2019. Included unrealised gains in my property development as well as website business. Good savings rate due to not much spending, invested in Aus and total world shares. Investing in my web business. Starting to shift focus away from $$$ and more into looking after my mental health. | LINK |

| Sep 20 | S1,045,486 | +$16,193 | 60% | Officially took time off work for the rest of the year to be close and look after family during major operations. Continued to sell down physical possessions and work on digital business while at home. NW gain mainly due to valuation of websites. | LINK |

| Oct 20 | $1,064,399 | +$18,913 | 80% | Base income (retainer) and leave loading, dividend and websites provided income, as well as raiding my P2P lending capital. Significant bill for property due to design not meeting standards which effectively lowers my equity position, as well as fence being stolen. | LINK |

| Nov 20 | $1,143,433 | +$80,394 | 82% | Big gains came from share market growth (influencing both the Financial Independence share portfolio and Invested superannuation), Business gains (due to increased earnings) and a $30K boost to my annuity thanks to me logging in and checking the fine-print on the accumulation stats. I only invested around $7K. Insane that in one month, I accumulated nearly more net worth than I did in four years from 2009-2012 | LINK |

| Dec 20 | $1,152,920 | + $9,487.32 | 84% | Share market slight drop, Earnings from Business, Contract work, Selling possessions. No share market investments this month (oops! I forgot and money was tight). Invested a lot into the website business this month (way more than planned) and it is still running at a decent loss (plans to turn it cash flow positive in 3 months). |

Monthly question from the Captain

Have you ever donated to charity? If so, which charity did you choose and why? Did you donate your time, services, products or money?

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Hey Captain FI,

I’m so sorry to hear these awful news about your Mum, I think you are very brave for sharing this news and also the upsetting news about your Dad.

Please don’t be so hard on yourself, you are doing really well now and I’m sure that your beautiful Mum is super proud of you.

As for your Dad. *sigh.

I can relate, a little, my Dad had his first heart attack at 55, followed by double bypass surgery and was told to change his lifestyle, but he just couldn’t do it, we lost him two years later, to another fatal heart attack. My grand father was an alcoholic and my 26yr old niece too. With my niece we tried and tried to help, but she had become toxic. She didn’t want help, so to protect our immediate family unit we made the decision to walk away and told her she wasn’t welcome in our life, after she threatened to have us killed and to break my daughter’s neck. It was horrendous. We made this decision to protect our mental health and our kids. And it was the best decision we’ve made.Life is more peaceful now. Sometimes, sadly, it’s necessary to walk away from people we love. I wish you all the very best. Just keep going. You’ve got this!

Hey Jodie, I am sorry to hear about your Niece – that is a bloody difficult situation. It is like you were at the end of your tether and she didn’t really leave you with any options. I am also trying to avoid the negativity and just focus on the positive, and thankfully I have some fantastic loving relationships within my family still.

I’m not sure what to write other than to say I’m so sorry to hear of your mum’s diagnosis. It’s so lovely to read of your awesome relationship with your mum, both here and on Instagram, and that you have each other’s backs in challengingly times. That takes love, work and commitment and you’re anything but a fuck up where it counts.

Thanks Flir, I am pretty darn lucky to have such an awesome mum. I just wish circumstances could be different, or there would be more time. I guess that is the condition called life though!

Great change comes from great trauma.

Keep it up, and dont let negative thoughts / emotions hold you back

JP

Thanks JP. I try to keep them in check with positive affirmations and gratitude statements!

I’m sorry to hear what you and your parents have to deal with. I wish I could say ‘the new year will be better’, but with what you’ve written, I doubt that will be the case. I wish you the strength and support to go through this and to spend as many moments as possible with your mother. Thanks for sharing.

Hey Joe, Thanks for the kind words mate. My strategy is to keep super busy, but I am also trying to focus on prioritising my personal life a little more. The next month I think will be a bit of a blur

Very brave of you to put this out there mate and sometimes it can be therapeutic to write it down.

I’m glad you’re back and getting stuck into work that you have a passion for. It’s the ultimate reward for people smart with your money… to be able to dictate what your life looks like.

Looking forward to the next update 🙂

Hey AFB, Thanks mate. It definitely feels good to talk about it and there is a very supportive community here, so its nice to know everyone has my back. I would be lying if I said I wasn’t a little bit nervous about heading back into work, I have had a decent break from flying and continuity is pretty important in aviation. But the simulator training staff are pretty good and my supervisor has already said they can be flexible on the time frame, so it is nice to know there isn’t a huge rush to get me back online. To be honest, I think industry wide aviation has seen a huge down turn in the number of flights, so I expect my rate of flying to be much lower than previously anyway which sort of helps that work/life balance. Unsure how the international flights are going to be running with COVID, but I guess all things I will read up on the company policy on when I get back into it and back hanging out with my colleagues. Fingers crossed all back online for the next update!

Another great post, brave of you as always, to ‘put it all out there’ but you appear to wear your heart on your sleeve and the honesty is refreshing

That Annuity must be a thing of beauty

Your savings rate always amazes me, similarly with hishermoney, you must’ve nearly run out of things to sell :o)

Thanks Baz, Yeah it has been a bit of an emotional time and I am probably guilty of writing here as a bit of a release. Re the Annuity, it was a bit of a stroke of luck to end up in that scheme to be honest, and I only realise now after getting interested in FIRE how valuable it is. You are dead right though haha I am almost out of things to sell, and I have stopped buying new things to flip as I have been focusing more on the website business now as a long term sustainable side hustle. Alex and Em from Hishermoney have some incredible savings rates, I dont think I have ever seen there saving rate below 90% lol! They must have some hefty income

84% is massive – I’ll have to work mine out one day. You are just working it out as savings rate by dividing your monthly savings amount by your monthly gross income?

Thanks mate – and yes Thats how I do it, but I also add super contributions to both sides of the equation – so its (monthly savings/investing plus super contribution) / (monthly income plus super contribution)