My experience with a residential joint venture property development investment; what it takes to finance and manage a subdivision and build for a small residential property development

Introduction

My residential joint venture property development investment was a stressful but ultimately profitable journey in learning how to successfully manage the subdivision of residential land and build multiple properties from the ground up – we purchased land, subdivided, and built two modest duplexes on a fairly small property in a regional east coast town. With many risks involved and a complex project full of snags that had to be overcome, this process was tricky for me to understand from start to finish, although I would describe my participation as primarily that of being from the passenger seat rather than the driver’s seat.

From site selection, real estate negotiations, financing and engineering design all the way through building codes and permits, development approvals, construction management and marketing of the finished product for rent – I want to share with the FI community, investors, and early retirement hopefuls what it takes to finance and manage a subdivision and build for a small residential development project.

CaptainFI is not a Financial Advisor and the information below is factual review information, not financial advice. This website is reader-supported, which means we may be paid by advertising on the site, or when you visit links to partner or featured sites. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer

Residential investment properties

One of the most popular asset classes in Australia is residential investment properties – houses, townhouses, duplexes and apartments which are rented out by people as a place to live.

Investment properties benefit from a huge number of tax benefits such as negative gearing1, leverage (borrowing money from the bank to buy the asset with only usually a 20% deposit) and the 50% CGT discount when held for over 12 months. When managed by a good property manager and tenanted by suitable and stable long-term tenants, and selected in the correct areas, Investment Properties can provide great investment returns, especially when considering the cash-on-cash return of the initial investment.

They can, however, provide a fair bit of headache – especially when building or developing property, and poor tenants can be a nightmare. There are also a lot of hidden costs, significant transactional costs, and a significant level of risk when it comes to maintaining the property – for example, things break, and when it’s a water heater, plumbing leak, air conditioner etc, these can be expensive. If you are negatively gearing an investment property portfolio too hard (i.e. hoping for too much growth or investing in high COL areas such as Melbourne or Sydney), you may also quickly reach your serviceability limit or borrowing capacity (usually around 2 or 3 properties for most people). Leverage can also cut both ways, as losses from downturns in the property market are magnified for those that borrow.

Notwithstanding, the correct property(s), managed with an appropriate emergency fund, insurance, the right professionals in your circle (i.e. property manager, tradesperson, brokers) can be a recipe for financial independence.

Captain FI’s joint venture property development investment

As I have mentioned many times in my net wealth updates – I am a novice when it comes to property investing, especially property development. I was only able to do this project because I joined a friend who has experience with several property development projects in Sydney under their belt. If you want to read more about shared property investing or shared property ownership, you can read my review of Proppie HERE.

We found the project through the Bob Andersen property development network after doing the Property Mastermind training course, and used a small ‘core’ team of a mortgage broker, building contractors and project manager to work on the project. Along the way, we also used a surveyor, solicitor, laywer (for contract negotiations due to the builders threatening to walk off-site and break contract), building inspector, property manager and a few other ones I’ve probably already forgotten by now.

It was a small project, only involving two duplexes on one site. My friend and I both stumped up the costs 50:50, and provided each half of the serviceability. However, we both took on 100% of the risk as we had to co-sign as guarantor for each other. I guess I didn’t fully appreciate the risks of doing so at the time, especially for what was going to be such a drawn-out process (we initially expected it to be a 18-month project, and here I am blogging about it as we finish just shy of our fourth year after a two-year schedule blowout – thanks pandemic!)

The project took place in a rapidly growing major regional city in the East Coast of Australia.

Quick Lessons Learned on my property development investment

It has taken a long time to get to this point, and boy have we made some embarrassing mistakes. Rolling lessons learned include but are not limited to…

- Thinking we *HAD* to do a subdivision and development to make money (when actually it can be quicker, less risky, less effort, and more profitable to simply buy and hold an established investment property).

- Not understanding just how significant the risks are by doing a Joint Venture where you basically cosign as ‘co guarantors’ on the project and associated loans.

- Thinking we could save money by NOT using an architect on a house and land package we bought from a developer *WITHOUT DA from council*

- Falling for the oldest trick in the book re: portable fencing hire (the fencing hire company stole the fences back and then tried to charge us for having them stolen)

- Endless delays by not having DA and needing to relodge with council three times meant we were one of the last blocks to be built on, and hence became the neighbourhood ‘free rubbish dumping ground’ when the fence was “stolen” (we then had to pay to get the rubbish removed and pay tip fees for – a big fuck you to any dodgy builders reading this who have ever engaged in this practice).

- Because we were the last to build, the ‘new neighbours’ objected to our build being two story due to shadowing – and we were forced to build single story instead at a reduced profit margin. Despite us being relatively early on the land release!

- COVID-19 delays, subsequent supply restrictions and union activity meant the builder essentially got a free pass to break contract schedule, in total putting us back by an extra 18 months with no penalty, compensation or damages payable (they even billed us for this extension!!) – this further took money away from the ‘bottom line’ as we had to pay more interest, had capital tied up, and was not earning rental income – all making the build less profitable.)

- Lots of small (but not insignificant) expenses such as council fees, independent inspection fees and rates (even though the house isn’t built yet, apparently you still have to pay rates…) add up to significant amounts over the project’s lifetime. I was amazed to see just how everyone gouges you for things you don’t even think about, and brokers / builders don’t mention these costs so you just have to cop them when they arrive. In the end, we had nearly $140K worth of interest charges and additional fees!

- Independent inspections2 and checks are worth their weight in gold. I am talking design and plan reviews, soil tests, site inspections, construction and building inspections etc. Do not cheap out or try to skip these, and don’t trust anyone or any builder – they are very cheap insurance and great piece of mind and give you (legal) leverage over the builder, especially if someone is trying to pull the wool over your eyes.

- Pay a lawyer or legal professional to read the contract. You think you can read through it yourself and spot everything but you can’t. The builders legit make it their BUSINESS to know how to weasel their way out of things as well as suck more money out of you.

- Builders can blackmail you and threaten to walk off site after you release large payment milestones, because you have less leverage. They are banking on you not wanting to go to court because of the cost and time expense. Be judicious about approving large payment milestones, and it’s better to only release small progress payments frequently, which keeps the money in your account and power in your control.

- Be careful if there is a project manager appointed by the lender or the builder. Because they are actually not working for you, they are working for the builder. Fairly self-evident how important that last bit is, as they will put the other party’s interest ahead of yours (i.e. you pay more, and the project gets delayed more). We did not have an independent project manager and ultimately, we were over 2 years behind schedule.

“When you build a house it is not a cheap process, it will be one of the biggest financial commitments you make. Therefore, it is well worth engaging a quality and independent inspector to give you the peace of mind that everything is to the highest standard.”

Zoe Langenberg – ibuildnew.com.au/blog/building-new/how-to-build/building-inspection-build-a-house2

Considerations to a residential property development

I have written the following in an attempt to distill my experience into a few relevant topic areas below, which might hopefully give you a better understanding of the process, risks and considerations should you decide to attempt something similar.

Pre-planning – research the area and analyze numbers

Pre-planning is essential in any project or endeavor, and it only makes sense that it’s crucial as well when traveling to a new place. Before hopping on a plane interstate or saddling up for an epic road trip, it’s essential to research the area you’re going to, especially if it’s unfamiliar terrain. Analyzing numbers such as crime rates, property values, demographics, rental vacancies, rental yields and socio-economic factors and climate can help you make informed decisions and plan accordingly. Knowing what to expect can ensure not only a smoother process but also a safer and more enjoyable experience.

After all, the more you know about your target area, the more you can prepare for whatever surprises come your way. So, take the time to pre-plan, research, and analyze numbers before starting your detailed search. You want to use a phased or iterative approach, initially casting a wide net and then incrementally increasing the detail.

Setting up the project team– hiring professionals, engineers and surveyors etc.

Building a successful project team is a crucial step toward achieving the ultimate goal. Hiring professionals such as engineers, architects, property managers, mortgage broker, building inspectors, solicitors, project managers and surveyors are essential to ensure a smooth and efficient project. These individuals bring a unique skill set and expertise to the team, allowing for a diverse range of perspectives and ideas. It’s important to carefully select team members, ensuring they possess the qualifications, experience and passion required for the project.

Building a cohesive and collaborative team is not an easy task, but with the right individuals and guidance, it can lead to successful results.

Communication through all stakeholders and service providers is really important, so using an online project management software and cloud storage system where everyone can access files is really important.

When it comes to navigating local council planning processes, things can quickly become overwhelming. Our project was delayed by over 12 months due to bureaucratic shit from councils and neighbours complaining about overshadowing (even though we were the first to commence building!).

At the end of the day, there are strict regulations to follow and mountains upon fucking mountains of (mostly unnecessary) paperwork to complete. Most of these papers never get seen, however god forbid you forget to dot the i’s or cross the t’s on one of them because sure as shit, this will lead to a DA rejection.

However, despite the challenges, it is important to remember the end goal – bringing your vision to life, and making the cashola to bring FI closer.

Whether you are planning to build your dream home or do an investment development, the local council planning processes can feel like a daunting task. But with the right information and support, you can successfully navigate the process and achieve your goals. The best bit of advice is to invest in experienced professionals to be part of your project team.

You can read about Commercial Property Investing in my article HERE.

Building timeframes & budgeting – setting realistic goals to meet deadlines

Timeframes and budgeting are essential components in achieving any project, whether it’s your personal finances, running a business, doing a home renovation, building your PPOR or a multi-property development. Setting realistic goals is the key to meeting deadlines and achieving desired results. Careful planning and budgeting can help avoid unexpected costs and delays.

When creating your timeframes and budgeting plan, it’s important to take into consideration the scope and complexity of your project, as well as any potential obstacles that may arise. By breaking down your project into manageable phases, you can prioritize tasks, allocate resources, and monitor progress to ensure you meet your goals. With a well-planned budget and timeline, you can stay on track, make informed decisions, and ultimately achieve success.

I wrote this article on goal setting for smart investors, which is well worth revisiting.

Setting goals provides a sense of purpose and direction and allows us to focus on achieving what matters most to us. It is a way we can practice mindfulness, become more efficient with our resources and sharpen our focus onto exactly what is required for healthy progression and development.

What do you do when you are asked to eat an elephant?

Why: Why am I going to do this?

How: How am I going to eat this elephant?

What: I’ll take one bite at a time. Starting with the scotch fillet…

For larger tasks (like eating the elephant), you’re going to have to break this larger goal into many smaller, actionable steps that you can take to work toward that higher goal. Our brains naturally release the pleasure chemical Dopamine when we experience success, so chunking or breaking down larger goals into many easier smaller goals is an easy bio-hack to keep you motivated!

Expanding on the Golden Circle is the complementary concept of setting SMART goals. For a Goal to be SMART, they need to be;

- Specific

- Measurable

- Achievable

- Relevant

- Time-based

Setting SMART goals increases the chance that you will achieve them.

Anyway, don’t expect your 9-month build to take 9 months. If a builder says they can do it, they are probably lying. Our project took nearly 4 whole years from start (agreeing to do the project) to finish (tenanted and refinanced). Apparently, the ‘norm’ for builders is considered to be around 12 months, however, our builders took over double this from when we engaged them to start building. Obviously, the pandemic occurred right when we started the project which caused massive delays, but the ongoing repercussions from this pandemic, including global supply and labour shortages, inflation and the collapse of many Aussie building companies has really pushed out build times, so I would say you probably wouldn’t want to bank on anything less than 18 months from when you engage the builders.

Also, consider the quality you are prepared to accept. The old tenant of project management is “Quality, Time, Cost – Pick Two” – so if you want it done cheap and fast, the build quality will be shit. And if you want it cheap and quality, then the project schedule will be fucked – which actually ends up costing you more as delays translate directly to cost overruns with costs involved including additional interest repayments, fees, council rates etc with no rental income coming in. As an investment property, you want it to obviously meet design standards, and it helps to have your own independent, qualified building inspector doing your own separate inspections for each phase before releasing milestone payments to the builder – that way if they pick up any dodgyness, you can correct it before construction continues.

Documentation and financial management – staying on top of accounting, legalities and tax

When it comes to running a successful business, keeping on top of documentation and financial management is essential. A property development is no different – you are running a property business, just in your name rather than a company entity.

From accounting, council submissions and legalities to taxes, there can be a lot to juggle, making it easy to overlook important details. However, by prioritizing organization and attention to detail, you can stay on top of everything and avoid costly mistakes.

Consistent and accurate record-keeping, document submission and filings will not only help ensure compliance but also improve your overall financial health. While it may require some effort and discipline, staying on top of these important aspects of management can set you up for long-term success.

To make this process easier with multiple stakeholders all interstate, we used a Google drive to store all of our documentation in the cloud, which got scheduled for backups each day. We also allocated jobs to specific people and nominated one representative to communicate with the project manager to reduce duplication. We also used project management software which the project manager oversaw.

Stress Management, Problem Solving and how to stay calm

Stress can be an invisible enemy, affecting us in ways we never thought possible. Whether it’s due to job pressures, family issues, or simply the chaos of daily life, stress can cause us to feel overwhelmed and anxious. Managing your stress and using problem-solving flows can help us stay calm under pressure and remain focused on the end goal, avoiding making bad decisions or ‘Snaps’ to get the best possible outcome.

So many times I wanted to ring up that shitty contractor or pedantic paper pusher at the council offices and put them on blast, but after taking a deep breath (and probably over-venting to whoever was closest to me) I realised that giving someone an ear bashing wasn’t going to help my cause. A couple of times as well, we thought the entire project was dead – like when we received our second council DA rejection. Rather than throwing our hands up, the first thing we did was actually do nothing. Knowing when you need to act and when you can do nothing is an important skill to have, and something I have honed over my 15-year flying career – many complex emergencies can be made worse by snapping and jumping in without fully understanding the situation.

So, take a deep breath, and follow the ‘G-A-D-I-E‘ flow: Gather evidence, Analyse the data, Decide on a course of action, Implement the course of action – Evaluate the result’

In many cases, once we took the emotion out and put our heads to it, we were able to problem solve by doing things like hiring professionals, redoing the engineering drawings (moving from two story to single story, then on the second rejection we were able to change the floor plan, and add additional features (like double glazing windows and insulation to meet environmental score performance) and calmly negotiating with builders and suppliers when they wanted to break contract.

Taking action in the face of adversity can help us feel empowered and in control. Whether it’s taking a deep breath, exercising, or talking to a friend, finding ways to cope with stress is key to maintaining our mental and physical well-being.

So, the next time you find yourself feeling stressed, take a step back, evaluate the situation, and focus on the end goal. Remember, you are capable of overcoming any obstacle that comes your way.

In general though, this process was extremely stressful. It took place during a really hard part of my life which was towards the end of my career when I had insane levels of responsibility and commitment to my role as a Pilot, relationship troubles and break down, the Black Summer bushfires, several family health emergencies including the passing of my mother from terminal cancer, and my own physical and mental health issues.

In hindsight, I would say, yes we made a lot of money out of this project, but it was definitely not worth the additional stress which I think contributed towards my feeling of burnout and exhaustion – feeding into my ‘FIRE’ addiction.

If you are easily stressed out, have a complex living situation, or if you are like me with extremely high standards and frugality and expect good performance from contractors, or maybe if you are experiencing mental or physical health issues, I would suggest steering clear of a property development or building a house. Just buy one that is already finished and do away with the stress.

Captain FI’s Joint-Venture property development figures

I will split this up into a few sections – Schedule, capital value, and cash flow (income), the cash-out refinance and future plans. Remember that we are novices with property development and this was my first project with limited guidance. The figures I have chucked down are our rough plans and results.

Schedule and planning

Initially, we had planned roughly an 18-month project (1.5 years) – which was roughly speaking;

- Phase 1: Finding project – 3 months

- Phase 2: Financing project and purchasing land – 2 months

- Phase 3: Planning permission – 3 months

- Phase 4: Construction – 9 months

- Phase 5: Refinancing – 1 month

- Phase 6: Marketing and rent – 1 month

This was probably an oversimplification, but we figured this contained significant fat for overruns, and it was generally in line with the property development guidance we had received from the property development course my business partner had done with Bob Anderson Property Mastermind.

How it turned out;

The project ran over schedule by 2.5 years, ending up taking just under four years from conception to complete refinance with paying tenant.

- Phase 1: Finding project – 6 months (3 months over schedule)

- Phase 2: Financing and purchasing land – 6 months (4 months over schedule)

- Phase 3: Planning permission – 9 months (6 months over schedule)

- Phase 4: Construction – 24 months (15 months over schedule)

- Phase 5: Refinancing – 3 month (2 months over schedule)

- Phase 6: Marketing and rent – 2 weeks (2 under schedule)

Phase one – finding the project

As it turned out, it took us over 6 months to even find an appropriate project because every time an opportunity presented itself, we ran the figures and they just didn’t stack up. I think this was a factor in our final decision to ‘go ahead’ on this project because we were getting sick of searching and were just really wanting to get started – so we agreed to start this as an “acceptable” project (it wasn’t ever going to be amazing from the get-go – not just “good” but “good enough”). This should have been a warning sign to us – remember the old adage “haste makes waste”. Whilst you never want to rush into anything like this, at some point you do have to pull the trigger or else you end up with analysis paralysis.

Phase two – financing, and purchasing land

The second major delay was the financing delay due to my joint venture partner not having their finances appropriately in order for this project. I mean basically, they were bringing the property development skills and I was really just bringing cash and serviceability. They were completing an earlier property development which I believed ran over schedule and left them in a tricky spot where they were unable to secure finance for the next one (this one), so had to work closely with the broker until they were at a stage with the previous project where they were finally able to secure finance for this project.

This wasn’t something we had really talked about in detail or that I had really appreciated the risk of, and I definitely felt out of the loop. This is itself one of the MAJOR risks of doing a joint venture property development (or any joint business venture or investment). You just never have 100% oversight into or over the other party, and you have to just trust them. A lot of people get burnt this way – even Mr Money Mustache did and wrote about in Mr Money Mustaches Big Mistake.

Purchasing the land was fairly straightforward as it just came from a large property developer doing a land bank release. We had to put down 40% for the loan and got a great deal on an interest-only loan (which we eventually rolled into a construction loan with another lender once my business partner had the serviceability). Being a JV it added complexity to every deal as we had to have both names on everything.

Phase three – planning permission / DA

As I mentioned earlier, planning permission for our project was a shocker, getting rejected twice and dragging the process out to almost a whole year. I did not realize just how long it took councils to respond to DA requests, and had no idea about what was required. Our first rejection was based on environmental standards – our plans didn’t have enough ‘eco points’ to be considered environmentally friendly enough to be approved. As a result, we had to go back to the drawing board and have the design altered to make the windows smaller and add double glazing, and that kind of thing to improve energy efficiency (variations which we had to pay for out of pocket for the build!).

Because of the delays, neighbors had already started their builds and now started complaining about overshadowing when we lodged our second DA, so the council rejected our new plans and forced us to abandon a two-story build. After our second DA rejection, we were already over 1.5 years over schedule and we seriously considered selling the land and abandoning the project. We decided to push on, amending the design to single story 3/2/1 duplexes which got approved.

It was during this time we had a lot of issues with rubbish dumping, the fence ‘incident’ and a bunch of other small hassles. The construction loan process was also tied up in getting DA approved so the broker could pitch the project to the lenders, so this stretched out into Phase three. I had my suspicions that perhaps one of the reasons it took so long may have been because my partner might have been still shoring up their finances from their previous project. But we got there in the end!

Phase four – Construction

It was exciting to see the soil finally turned and the slab poured, but once construction started it pretty much all came to a grinding halt thanks to the Covid-19 pandemic and the lockdowns. We started to see a huge shortage in the labor workforce, equipment, and supply shortages, and basically non-stop excuses from the builder as to why they were breaking contracts. Prices started to skyrocket and our building stagnated. In the end, it got a bit ridiculous and the builder started to be very liberal with excuses, variations, and schedule extensions, and we could see they were taking advantage of the situation and going off to work on other builds with newer contracts where they were getting paid more. They also did some quite sloppy work they tried to hide and sneak through payment milestones which we were glad we had independent building inspectors keeping tabs on.

We got to a point where the relationship with the builder had deteriorated and the trust was gone, and it was either go to court, fire the builder, and find another builder, or just cop it on the chin and keep going accepting the lost profit. We got legal advice and weighed up the risks, and it just wasn’t worth fighting the advice was it’s cheaper to keep going and to use independent inspectors and hold them accountable to the contract as much as possible. Getting a new builder would mean even more delays, plus paying the newly inflated prices due to the increased demand and shortages. So we paid the variations, accepted the extensions, and had to argue the minutia which was very frustrating.

I wrote about it in my monthly net wealth updates – in November 2021 when got to the enclosure stage I had a bit of a chuckle when I saw some of the standard of work that had been done – They say a picture is worth a thousand words, so here are three….

All I can say is that I am very glad we spent an extra thousand dollars on an independent third-party building inspector to check the builder’s progress. When I showed this to a few tradie friends of mine they said “Looks like it was built by a blind person”, and then “A kid could probably do better than this” and then finished up with a much more realistic “It looks like they have let the apprentice have a go unsupervised and then thought they could sneak it past a payment milestone – ask to see their qualifications and check the sign in log to see who was on-site”.

Eventually, though, after taking over double the planned schedule, all of the defects were rectified and the property was finished.

Phase five – Refinancing

The refinancing aspect was stressful for me as I needed to secure financing whilst I still had an income for serviceability. This was occurring around the time I was ready to leave the workforce , much to the dismay of my JV partners. Originally, we had planned for the refinance to occur before I left my flying job, but the project running over schedule by so much had really pushed this out of the question.

Thankfully I had a pretty good Mortgage Broker who was able to sort it out in a couple of months, and actually by the time we were starting the refinance, we actually already had a full occupancy of tenants in paying rent which helped the process. My broker used the rental income, as well as my business income and share portfolio as collateral to secure the loan (more on valuations below).

Phase six – Marketing and rent

This was by far the simplest aspect as we had entered a housing crisis. As this was interstate, we contracted a property management company to run the rentals. They came out, took photos, created the online listing, and screened the tenants. We just had to pick from a shortlist of applicants the property manager had screened, and we ended up just going for the one they had recommended – which was a group of medical students with no pets. The rent achieved was over $100 a week higher than initially planned at the start of the project, and we had tenants in basically as soon as we had advertised.

Capital value

Going off the bank’s initial completed estimation of $560K, with the mortgage the way it is ($360K) leaves me with about $200K of equity in the duplex, and after accounting for expenses I planned to make just under $70k of ‘manufactured equity’ with an investment of about $130K over two and a bit years (not all of the cash was required upfront so these return figures should be conservative). This is an approximate projected annualized return3 of about 10%, which is the figure we decided to go ahead with when we initially calculated the risks – however, in hindsight, you shouldn’t really start a project unless the profit figure is at LEAST 20%.

However, despite rising interest rates and inflation and a lot of speculation on asset prices, over the years we did the build, there has still been a strong upward trend of property values in the area. I was hoping we could get it revalued on completion at higher than our initial $560K estimate, and as luck would have it, the sworn valuer came out with a $650K valuation after inspecting the property on completion – which was pretty great to hear – an additional $90,000. This brought the manufactured equity up to $160K which resulted in an approximate annualized return of 22%. This makes the project return a ‘Go ahead’ based on the risk/reward factor (however the profit figure is not the only factor – you need to consider the other risks and things such as area, demand, rental yields, builder, supplier, council, complexity amongst other things).

When trying to get an updated valuation for the latest refinance after the completion of the project, the mortgage broker and I looked at property transaction data in the area along with using their various online appraisal tools, and saw that property prices had experienced another jump in the area so we ended up getting another valuation done. The bank agreed on the updated valuation of $750K, which when calculated to an annualized figure gives a return of 31.6% – HOLY SHIT BATMAN – why don’t we all rush out and do a property development?!

Well, of course, these returns and figures don’t really mean anything and are all of course subject to the property ever getting sold in the future and then subtracting selling costs (and then paying the capital gains tax liability), but they are the ‘guestimate’ of what I could get on sale. And remember, it is in a bank’s interest to overvalue, as it means they can dish out a larger loan (to a customer with appropriate collateral – like my $1M share porfolio!) and rake in more interest repayments.

Construction supplies and labour have also inflated hugely since we finished building, with some companies estimating between a 50% to 100% price increase to build – which is reflected in the current market valuation (and also annoyingly we have to insure it for twice as much or we wouldn’t be able to afford a rebuild if it does burn down!)

Cashflow (income)

The property has now been tenanted through a property management agency. Based on the current mortgage and interest rates, council rates, water, insurance and property management fees, it is now basically cash-flow neutral producing about 20 bucks per week. If interest rates continue to rise above 5.5%, it will start to become cash flow negative.

However, on paper with the associated tax deductions (such as the depreciation schedule), I can claim a tax refund, which makes it actually cash flow positive after tax. This would be a higher tax break if I was on a higher income, however, I am now on a low taxable income (Under $45,000 with a marginal rate of 19% + 2% Medicare levy = 21%) so it’s not as lucrative as someone still in the accumulation phase on higher marginal tiers. I haven’t calculated just how much of a refund I will get at the EOFY, but I plan to just throw all of the documentation and some money at my accountant at tax time and make it their problem!

The bottom line is it is making a small amount of money, so it isn’t costing me anything, and being in a rapidly growing east coast major regional city in a housing shortage and building supply crisis, means the capital value of the house is continuing to increase. So in that respect, it almost worked out to be a unicorn property investment, or in other words a bit of a ‘Have your cake and eat it too’ scenario. It is also providing exposure to property, so that my investments arent just purely in shares. This is good for a bit of diversification (although some might argue that this is an insane concentration risk – just one property, with one set of tenants, in one city, in one country…)

One of the most frustrating things about the pandemic and the build stretching out, is that we essentially lost about 2.5 years worth of rental income

Cash out Refinance – the next property

Something very useful during the refinancing post-completion and tenanting was my mortgage broker was able to do a ‘cash out refinance4‘ based on the highest valuation and allow me to get at some of the manufactured equity.

“A cash-out refinance is a mortgage refinancing option that lets you convert home equity into cash. A new mortgage is taken out for more than your previous mortgage balance, and the difference is paid to you in cash. In the real estate world, refinancing in general is a popular process for replacing an existing mortgage with a new one that typically extends terms to the borrower that are more favorable. By refinancing a mortgage, you may be able to decrease your monthly mortgage payments, negotiate a lower interest rate, renegotiate the periodic loan terms, remove or add borrowers from the loan obligation, and, in the case of a cash-out refinance, access cash from the equity in your home.”

James Chen – investopedia.com/terms/c/cashout_refinance4

We actually did two loans to accomplish this (one loan to replace the construction loan, second loan for the equity cash out). Taking this equity out and putting it into the offset doesn’t actually cost me anything yet since this cash is currently offsetting the loan 100%, but when I draw it then of course I will start paying interest.

It is definitely cool seeing such a huge offset balance – but I also did wonder if this balance is protected by the $250K government bank balance insurance – perhaps any experts can let me know their thoughts in the comments. Could a bank go bust and disappear, stealing your offset account, but leaving you with the mortgage? My thoughts are that logically, they would have to discharge the mortgage if they took the cash. Someone smarter and more experienced than me can answer that question!

Anyway, having additional funds in the offset account means I can take this cash out of the offset and put it towards a deposit for buying my own personal place of residence – the farm dream – however when I do so the loan repayments for the I.P. will go up and it will no longer be cash flow positive. Also, I have read that if you are drawing that offset out for a PPOR, then it can get messy re: tax as the interest for the loan isn’t tax deductible anymore – so I will need to speak to the mortgage broker and accountant to work out the optimum way forward for debt recycling that ticks all the rules.

What am I doing with the loans?

I have no intention to quickly pay off the investment property loan because it is tax deductible, and will instead prioritize obtaining and then paying off my PPOR (future hobby farm) as soon as possible. However, in the meanwhile, I will pause any further share investments or dividend reinvestments, and begin to accumulate a large cash stockpile for the farm deposit and be keeping this in my offset account with my (now larger and healthier) emergency fund of 2 years living expenses. I am ideally targeting a cash pile of over $200K so I can get an LVR below 80%5 on the farm, and then will recommence investing any surplus cash.

Captain FI’s property development trainer: Bob Andersen – Property Mastermind

I first heard about Bob from my JV partner. From our semi-regular chats about business, finance, and investing, where we both planned out our paths to Financial Independence and ‘wargamed’ and critiqued each others strategies, it became clear that we were both interested in real estate investing. When we initially talked on the phone about it that night, he made a point of mentioning bobs courses as his knowledge source and provider of a lot of the professional networks he had used previously.

Although at times it was a stressful experience for me (because I was a novice developer), my JV partner had successfully completed several property development projects beforehand – a combination of a few renovation ‘flips’ as well as three ‘from scratch’ builds. Having an experienced JV partner, plus access to the information and network from Bob Andersen’s property mastermind course definitely put my mind at ease.

Probably one of the biggest take-aways for me was that having a set of established procedures and a great network are probably the two most important things in property development. Put simply, you don’t know what you don’t know, and when you are dealing with potentially millions of dollars the last thing you want to do is to be making it up as you go along. Having a set of Standard Operating procedures (SOPs) or Guidelines is pretty important, as well as knowing who to contact and when – especially when things don’t go to plan.

We actually struggled for a long time to even FIND a project, and it was only thanks to the network we had access to through Bob Andersen that we were able to source a development project via a buyers agent (who we paid a finders fee to), as well as other professionals such as our Mortgage Broker, Building Inspectors and Builder (as well as a few other obscure professionals which I didn’t know we would need including conveyancers, project managers, surveyers, solicitors and property managers).

Whilst the global pandemic obviously had a profound impact on my first property development (and ultimately delayed us by two years), based on market valuation of $750K (per unit) at the completion of the development, initial invested capital of $130K, a manufactured “stress equity” of $260K, and a mortgage for the remaining balance of $360K, I was able to realise an annualised 32% cash-on-cash return over the four-year long project.

Whilst that might sound like good returns from the development – it’s worth pointing out that DA rejections, schedule delays, and subsequent cost overruns massively ate into our profit margins. Whilst the pandemic had a significant impact, a large responsibility also falls onto us and our lack of experience as novice property developers. Even though we made a few mistakes, it was very helpful to be able to speak to Bob and Hillary, as well as others in the Property Mastermind network, for advice and mentoring when we got stuck.

Property development vs buy and hold property investment

So, at the end of it all, was it worth it? Well, one way is to compare how we did to other asset classes over the four-year period 2019-2022 (inclusive). This will show me how ‘well I did’ in this four-year period, but its worth noting that buying and holding property is a long-term investment strategy and four years is a pretty short timeframe to really be looking at anyway, so keep that in mind. Obviously there is going to be some rounding and approximation here, but its a good start.

Buy and hold property in this area

In the area and timeframe where we did our development, on average, median house prices rose from $630K to $835K – giving (before selling costs and taxes) an Annualised Percentage Return figure of 7.3%. Using a standard leverage figure with a 20% cash deposit of $126K, and a $524K loan (including stamp duty, similar figures for what we put into the development) would have led to a $311K equity position (plus approximately $104K in rental income over the 4 years which would have mostly serviced the loan), which would have been an annualized ‘cash-on-cash’ (total equity to starting capital) rate of return (before selling fees and taxes) of 25.34% – that’s a cumulative 146% return on investment in 4 years.

At the completion of our project, the final valuation of $750K meant an equity position of $390K, which when calculated to an annualized cash-on-cash rate of return (before selling fees and taxes) ended up as 32%, for a cumulative 200% return on investment in four years. Which is obviously higher than if you just had bought and held a property in this area for this time period, however, the buying and holding of a property is a lot less risk, effort, and stress than doing a development.

Buy and hold property (Australia)

I am not an expert on property or historic property prices, but the following is an average of data I have read from Trading Economics, Domain, Real Estate, Rams, CoreLogic, ABC and NAB. According to RAMS, the consensus is that over the past 25 years the annual percentage change in Australian house prices was just shy of a 6.8% increase (and then obviously increase that figure by calculating a cash-on-cash return figure for the amount of leverage you are using).

According to figures I have had to mesh from TradingEconomics.com, ABC and CoreLogic;

- The median Australian dwelling price in 2019 was approximately $540K, and at the end of 2022 it was $708K. An annualized return of 7.04%

When we dig deeper to try and separate Capital and Regional properties from the national average, we see

- The median combined capital property price in Australia in 2019 was approximately $767K, and at the end of 2022 it was $1,008K. An annualized return of 7.07%

- The median Sydney property price in 2019 was $1,069K, and at the end of 2022 it was $1,413K, an annualized return of 7.22%*

- The median combined regionals in Australia in 2019 was approximately $412K, and at the end of 2022 it was $567K, an annualized return of 8.31%

Taking the best performance here of combined regionals of 8.31% annual growth, when you do the Cash-on-Cash calculation it ends up being 27.26% or a cumulative total percent return of 167.5% – not bloody bad at all if you ask me, and only 4% lower annual returns than what we achieved with all our work, stress, and risk on the development. Perhaps I would have been much better suited to simply buy and hold an investment property in a regional city?!

*Obviously we now know Sydney boomed in 2023 after the 2022 correction, meaning if we expanded this analysis past 2022 Sydney real estate would have been the most attractive – if only I had my crystal ball at the start of the development!

Property development vs other investments

To keep the comparison interesting, I thought I would compare my development return to my other investments

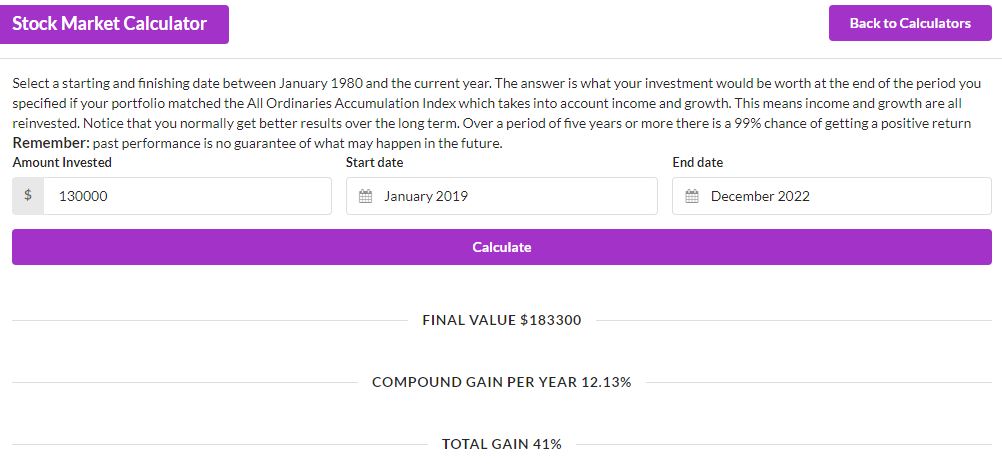

I love investing in boring, passive, total market index funds with low fees. If, Instead of doing this property development, I had invested the $130K deposit I used into shares that matched the All Ordinaries Accumulation index (which takes into account both income from dividends being reinvested and capital growth of the share) over this period (2019-2022) I would have gotten an Annualised Percentage Return figure of 12.13%, with a cumulative 41% return on investment in 4 years.

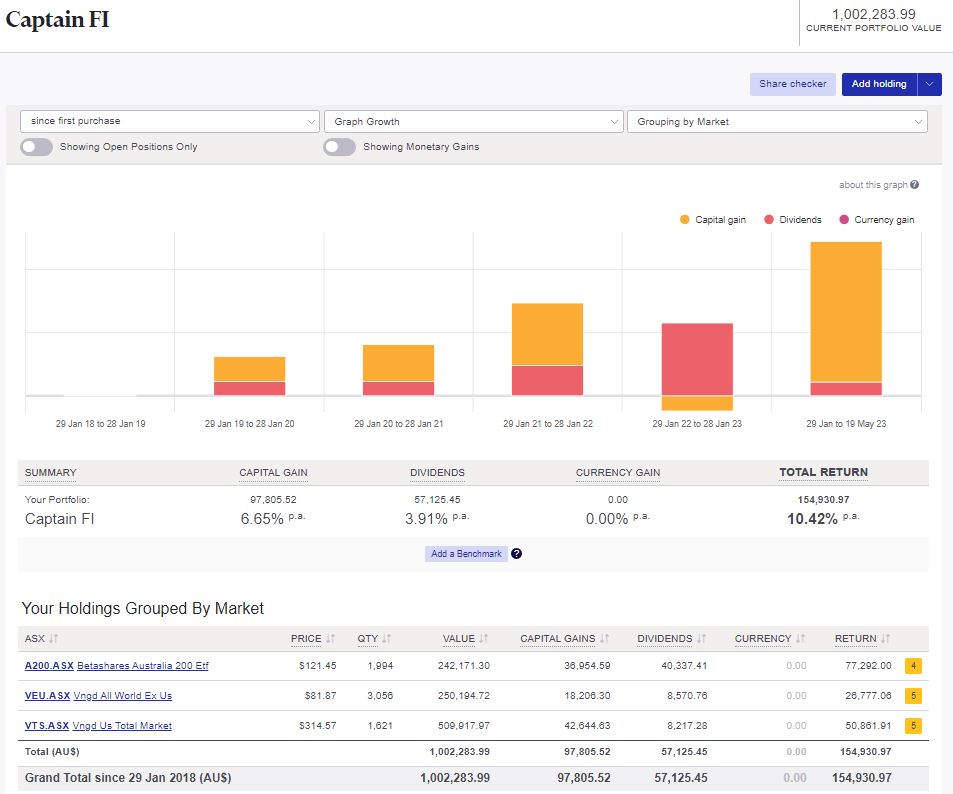

You can see my total share portfolio below, noting that I use a mix of Australian and international shares which has a long-term total return of 10.42%, so, thats a pretty reasonable figure, and I try to hang my hat on a figure of about a long term average of 10% annual returns for shares (capital growth + dividends) before inflation (which means a *real purchasing power* return of around 7-8% on average).

Whilst shares outperformed property growth in this area by about 5% on a ‘like for like’ basis, the real thing to consider here is leverage. It isn’t easy to leverage shares, and when you can, the best you usually get is around x2 leverage (and this itself is risky due to volatility and something called margin calls). Whereas in Australia it is almost a religion to have a mortgage on a property. Usually, you can leverage property by x5 using a 20% deposit, and borrowing the other 80% from the bank.

So that’s why even though shares have outperformed property in this area and time period with an average 12% annual return against 7% for property, when you consider leverage and total cumulative return, buy and hold property in this area would have returned 146%, the development returned 200%, and shares would have only returned me 41%.

The benefit of the shares though is they are the only true passive income – no serviceability requirements, no stress, no maintenance, no tenants etc!

Crypto currency (Bitcoin)

Bitcoin in January 2019 was trading at AUD $5,335 per coin. In December 2022, it was trading at $24,289 This represents an annualized return of 46.07%, and a total cumulative return of 340.7%. Had I held it instead of doing the property development, I would have made over double the total return ($592K vice $260K)!

However, if only I had known to time the market correctly and invest my $130K into BTC in January 2019, and sell at the peak in Nov, 2021 at $87,843, I could have made 154.4% annualized return or a 1546% return over three years – and pocketed a cool $2.14 Million to live out my fat FIRE best life.

Of course, life doesn’t work this way, and no one could have possibly predicted the price movement up (and then down) of Bitcoin. I held a small amount of Bitcoin and Ethereum and went along for the ride, somewhat dollar cost averaging in, and am now currently sitting at a 25% loss! Haha hows that for following the herd! I do still think there is a potential upside worth the risk (for me) so will continue to hold long term and see what happens.

Websites

Now this is opening a bag of worms. The interesting thing is the whole time I had been doing this property development, I have also been learning about websites – working on collaborations, building many my own sites, and then buying a website.

Say I had used my $130K to buy a profitable online business such as a content site (monetized through advertising and affiliate marketing) I would expect to get on average a 33% annual percentage return in business profit (approx $3600 per month based off a standard website valuation of 3 times yearly profits) without using any leverage. Straight off the bat, that’s a pretty good return, especially since at this point you haven’t actually done anything, and there is no leverage required to buy that website business.

But the real multiplier comes out after you renovate and improve the site. By adding content, optimizing on-page SEO, and optimizing off-page SEO with networking, backlinking, and social media activity, I have been able to grow my portfolio of websites exponentially. Starting from SCRATCH, that is, ZERO investments, and bootstrapping my way forward (that is, reinvesting all earnings from the business), over 4 and a bit years I have managed to build a website portfolio with several attractive brands, combined reaching on average over 100,000 visitors per month (and much higher at times).

At one point, I had a valuation of the portfolio of a whopping $1M – however this has since slid back a lot after not prioritizing (basically ignoring) the business for 9 months due to family and personal health issues, and selling some of the sites. Which is an important lesson about the nature of any business, including online business.

So, how would a $130K investment in a website go if you actually worked on it consistently in the evenings or weekends? It’s hard to say. It depends on the site, niche and competition but I would be pretty confident I could get at least a 5-10% annual increase in traffic (and hence monetization) each year on a mid-level site around the $50-150K mark, but it depends on how much work you put in and how skilled you are at your due diligence, SEO, content production and outsourcing.

Earning a 33% annual percentage return in the form of monthly cash-flow profit is pretty cool, and add growth from any web renno’s to that could give you a figure of over 33% returns! But! beware, if you don’t know what you are doing you could easily tank a site too, ending up wasting your precious time and losing your money.

I have written about this extensively in my article on how to make money online, as well as my review of a couple of training providers in this space.

Conclusion

Pre-planning, setting up the right team, understanding the local council regulations, setting goals, scheduling and staying within budget and schedule are all normal parts of any development project. But managing stress and problem-solving can be particularly challenging, I personally found this the hardest part and looking back in hindsight, yes we made money but it was probably not worth the stress.

The final figure was a 32% annualised cash-on-cash return based on an initial $130K of invested capital, $260K worth of manufactured ‘Stress’ Equity, the current $750K bank valuation and a current mortgage for $360K. The project ran over schedule by over two years, and in total took just under four years from conception to refinancing with a paying tenant.

We almost abandoned ship half way, but in the end, managed to stay the course despite several crises occurring in the project, including a global pandemic. As a result of good margins, contracting buying our building supplies early before the pandemic price hikes, strong housing demand and price growth in the area, and a bit of good fortune, we ended up slightly outperforming buy-and-hold investors in the area with a +7% annual percentage cash-on-cash return increase (32% rather than the projected buy and hold investment property investors CoC return of 25%), and outperforming buy-and-hold investors in combined regional centers by a +4% annual percentage cash-on-cash return increase (32% rather than 28%).

This additional return came at the expense of significant stress and effort, and its probably fair to say that we probably just got lucky, as many developers including some of our friends have actually lost money over this same time period. The significant delays, schedule overruns, DA rejections, multiple variations, and cost increases significantly ate into our profits, but thankfully we still finished with a solid return.

This is obviously all predicated on my ability to sell the property for the latest appraised value, and then subtract the selling transaction costs and capital gains tax due which would then reduce the total profit figures. So in a sense, all of these numbers are kind of useless, or probably better described as a ‘best guestimate’ untill that actually happens – so I will update this article when we do sell the property.

Now that I know the figures and have been through it, I think I would probably be much more inclined to simply invest in a regional center buy-and-hold investment property than to do another property development (and as I said above, I would prefer to build online properties than physical ones). Quite frankly, I am somewhat loathsome of the idea of ever building a house again, and will most likely look to purchase a PPOR that’s pre-existing or turnkey to avoid having to deal with builders *shudders*.

Have you thought of buying or building an investment property? If so, then just be very careful if you do decide to build as some builders have been going bust, and many industry commenters are suggesting you should not be starting a new build right now due to critical supply shortages.

Reference List:

- ‘What is negative gearing?’, Treasury.gov.au. Accessed online at https://treasury.gov.au/review/tax-white-paper/negative-gearing on April 20, 2023.

- ‘Should You Engage a Building Inspector When You Build a House?’, Zoe Langenberg, iBuildNew. Published: Oct 4, 2017. Accessed online at https://www.ibuildnew.com.au/blog/building-new/how-to-build/building-inspection-build-a-house/ on April 20, 2023.

- Annualized Return Calculator, BuyUpside.com. Accessed online at https://www.buyupside.com/calculators/annualizedreturn.htm on April 20, 2023.

- ‘Cash-Out Refinancing Explained: How It Works and When to Do It’, James Chen, Investopedia. Published: May 26, 2022. Accessed online at https://www.investopedia.com/terms/c/cashout_refinance.asp on April 20, 2023.

- Home loan-to-value ratio (LVR) explained, Bank SA. Accessed online at https://www.banksa.com.au/personal/home-loans/LVR-loan-to-value-ratio#:~:text=A%20lower%20LVR%20means%20less%20risk%20for%20us&text=A%20lower%20LVR%20means%20less%20risk%20to%20the%20bank%20too,the%20balance%20of%20the%20loan on April 20, 2023.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.