CaptainFIs financial and personal update for the end of Quarter 1, 2023

One year of (Semi?) Retirement… Has it really been this long? Read the full article below to check in on my investments and life post-FI

Captain FI is not a financial advisor, does not hold an AFSL and this article is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer

Captain FI’s personal update

A lot of things have changed since my last update… I moved in with my dear Mum to be her full time carer, but unfortunately she passed away at the end of last year. I was, and still am just absolutely heartbroken and would give anything to have her back. She fought to the very end, and it was only a few weeks after they stopped treatment that she passed.

To make things even more complicated, my step brother (who is an Australian citizen) from my father’s latest ex-Wife (in Indonesia), turned up in Australia the day after Mum died, and I got a series of panicked messages from his mum asking for me to pick him up from the airport and look after him – so he initially came and stayed at my mums house.

Mums passing really sent shocks through our family, and its sad to say a lot of our family relationships seem to be severely impacted. After her funeral, my siblings decided to ‘lawyer up’ and evict me from the family home – leaving me homeless (couch surfing with good mates and living in hotels) amidst a pretty savage housing crisis, and our step-brother having to live with (and now care for) our estranged father. Everyone I have spoken to hasn’t been surprised though, apparently, this is pretty standard behaviour after a family member dies if there is any form of estate or inheritance involved.

A really sad thing is I know one of my siblings mother in law is now facing her own battle with a similar type of cancer, and I do want to help and be a part of the family support system especially looking after my nieces and nephews, however it’s gotten now to the point where there isn’t communication between us siblings. I honestly don’t know if our family relationships will ever be the same again.

It got me thinking about reviewing my own last will and testament, which I have now redone along with advice from my lawyer, as well as a Binding Financial Agreement (pre-nup) between my partner and I, and I also completed an Advanced Care Directive, and used these documents to update my old ‘Barefoot Investor Fearless Folder’ (folder full of information for my partner just in case I die). I will post a separate article about my Fearless folder and everything it contains.

I have been pretty concerned for my brother’s wellfare as he has now basically been forced into the role of caregiver to our estranged (and abusive) father who has a terminal illness and drug addictions, when he should really just be enrolled in school and getting an education and you know, being a kid. I voiced my concerns to the greater family unit and unfortunately didn’t get a lot of offers for help, so I ended up having to make a mandatory report to the Child Abuse Report Line and getting a social worker involved. Thankfully they took this seriously and he has support from a social worker, as well as from myself and from a couple of our uncles that live in Adelaide and are able to drop in and check on him from time to time. Together we were able to organise basics such as a bank account, identification, Centrelink etc and he is now enrolled in high school and doing well. It’s good to be able to hang out with him and reconnect.

In terms of living arrangements, my partner and I basically found it nearly impossible to get a rental – which was just insane. I spent weeks madly searching and applying for over 200 rentals whilst couch surfing, and just got knock back after knock back. Two people – one medical professional in full time employment, combined net worth in the multiple seven figures, flawless rental history, and one small dog. No one wanted us, we ended up having to resort to rent bidding (which is apparently illegal for landlords to do) and even then we still continued to miss out on dozens as they seemed to just get snapped up.

All of this stress, plus this giant black hole that formed after mums passing really took its toll on me. To get away from everything, my partner and I decided ‘fuck it’ and to take a break we packed up and went to the Philippines to travel for a few months. This was relatively easy as she was living in a sharehouse and I had given away all of my furniture when I moved in with my mum anyway, so it was only a matter of selling a few things of ours (and all my plants!) and putting a few treasured possessions into storage at a friends house. It was sad to leave our dog behind but she stayed and boarded with a trusted friend of the breeder and actually, she had an awesome time and did a fair bit of training so when we came back she was actually much better behaved and knew some new cool commands like Roll-over, Spin, and Turn.

The SE Asia trip was a great chance for me to connect with my partner’s family. They are lovely people, they run a Hospital and a School in Manilla, Philippines. She has a large family there and they are all medical doctors and its kind of cool to see how they chose different specialisations and can basically work in every department of the hospital and run medical missions as a team. They are very kind, generous and their hospitality was wonderful. We spent time in the family home in Manilla, but we also did some travelling as a large family unit including a trip to Singapore, Malaysia and Thailand and a cruise throughout SE Asia, as well as domestic travel within the Philippines where we learned to SCUBA in a tropical paradise. I had never done a cruise before and it was pretty epic, we will definitely be doing it again.

I plan to post a separate article talking about our experiences and costs and the possibility of doing this either full time or living abroad for part of the year. Anyway, after two months travelling the Philippines, Malaysia, Singapore and Thailand, we had roughly each spent $14K. My total was $14,220 – Approx $230 per day. All in all, nearly triple my usual living costs – we definitely weren’t cheaping out on experiences and had a great time. If we did this more frequently the costs would of course be much less.

- $3550 Airfaires

- $1520 food, restaurants and groceries

- $1200 hotels / resort accomodation

- $900 entertainment, activities and tours

- $840 tips and giving

- $700 Royal Caribbean cruise (all included)

- $520 dental work (cracked tooth repair, clean and scale, several fillings)

- $500 on SCUBA OWD course

- $380 drinks (alcohol, smoothies etc)

- $310 on taxi fares, grab (ubers) and shuttles

- $230 medical costs when I got covid

- $200 clothes

- $195 petrol, tolls and parking

- $150 on gifts

- $120 on mobile phone roaming plan

- $5 for some 4:20 in Thailand

- $2900 Pet sitting and vet bills: $2900

On the bus ride home from the airport I got a call from someone regarding an interview I agreed to a while ago, which I didn’t know at the time but actually turned out to be a Reporter from News.com which published this feature article of me ‘Quite Simple’: How Aussie Man Retired at Just 31 – I was pretty shocked it made front page news and it resulted in a huge spike of traffic which really slowed down my website (so I ended up having to upgrade my hosting plan again haha).

When we finally came home we sighed as we still didn’t have anywhere to live – cue extreme anxiety and begin the rent bidding process again for dozens of properties. In the end, we managed to call a property manager and as chance would have it score an inspection for this small 2bdr house in the Adelaide foothills which took place at the same time she was doing the vacating inspection from the previous tenant. I think we got it because we jumped at it, handing her all our documents, renters resume and were able to transfer the deposit and a few month’s rent in advance on the same day. We ended up paying the advertised price which was good I guess, but as it turns out we are paying 50% more per week than the previous tenant (who does occasionally pop by to get her mail and voice her disgust at the ‘greedy landlord’ to me). It seems the landlord saw rents skyrocketing and booted her out knowing he could get a new tenant (us) in for a much higher rent.

Whilst I can sympathize with her – it is a shit thing to happen, we really needed somewhere to live and this was literally the first place to accept us in hundreds of rental applications and we had no control over the situation, we just desperately wanted housing and didn’t want to be forced to buy a property in a rush. This has really got me considering my stance as being a long term ‘Rent-vestor’ and got me really wanting to get this hobby farm and lock down some housing security.

After we settled in to the new house, and my partner settled into her new job, her parents came over to Adelaide to visit for a month, and we went for a family trip down to Tasmania.

We got to see a lot of beautiful stuff in Tasmania including the Aurora Australis, the West Coast Wilderness Railway and Bruny Island as some favourites, and can highly recommend it as a holiday spot. We only spent a week there and hired a car and used AirBnBs which is barely enough time to do it justice, so we will head back after winter with our campervan and spend a few more weeks really focusing on enjoying the areas we liked, and checking out the areas we missed. I will post a separate blog article about the trip and our itinerary for anyone whos thinking of planning a trip. I would have loved to have done a bit more hiking but as it turns out the old fitness isn’t what it used to be and I have stacked on a few kegs – so a good wake-up call to remember to prioritise my own health and get back into shape.

My partner and I celebrated our one-year anniversary whilst in Tassie with her folks, which snuck up quickly – we went out for a nice seafood dinner and splurged on an expensive platter at the Drunken Admiral at the Hobart docks, it was a great anniversary dinner (even if we had to share it with her parents haha!)

We actually also got away to the Gold Coast / Brisbane area for a week too as we wanted to start checking out the area, as well as visit some good mates who now live up there and we are seriously contemplating just going up there too. We hired a rental campervan from JUCY (I will do a full write up soon) which was a good experience and we actually bought a rooftop tent for my Stationwagon after this. The short of it is that the JUCY Crib’s kinda suck – they are really cramped and the bed isn’t that comfy – hence why they are so cheap (about $1000 a week or half the cost of a larger more ‘standard’ campervan). We still had a great time and it was really fun, exploring the hinterlands and pristine beaches around there.

Another thing my partner and I started doing regularly was blood donation. When I was younger I used to do whole blood donation, but after becoming a professional pilot we weren’t allowed to give blood within 3 days of a flight, so it made it hard to do. To be honest it kind of gave me an excuse not to do it, as life got increasingly busy and well donating blood is a hassle, so we just put it off and didn’t think about it.

Well, my partner’s sister had surgery recently and complications with internal bleeding meant that she needed several bags of blood to save her life. It really was a wake up call and we realised yep, we are blessed with good health and time and money, and we really need to be getting back into this. Weirdly, donating blood is actually beneficial for your health – particularly for me being male as a pilot with PFAS exposure at work, since donating blood is the only way to reduce your body PFAS contamination levels (this shit is also in non-stick cookware and a bunch of other stuff so probably have a read about PFAS online). I also have high blood pressure, and donating blood fixes that one a bit too haha (dropped by 10mmHg last time). Whole blood takes about 30 minutes, Plasma about an hour and platelets about 2 hours, and the staff manage your appointments and everything – you even get offered cookies, milkshakes, pies and pastries. I forgot about the citrate (anti-coagulant agent) reaction with Plasma donation and got a bit nauseous towards the end but chewing a ‘tums’ fixed it (the citrate causes a calcium/magnesium deficiency that makes you feel nauseus, but the antacids fix this).

My partner and I enjoyed Ramit Sethi’s new Rich Life series on Netflix. It was entertaining with the drama aspect, also shocking as the people are all so irresponsible and being US based it’s all about freaking credit scores and debt, so maybe not as relevant to Australia or the FI community. However, I still think it’s great as it’s helping to normalise talking about money and my partner and I watched it and it’s helped her to be more open to talking more about finances, and compliments our Barefoot date nights.

One change we made to our finances after watching this series was talking about our cash flows and our contributions. We do a ‘hybrid’ approach to our finances with both joint and separate finances (joint checking and a joint saving account, and then our individual checking and saving accounts and individual investing accounts). We think this has worked out well for us and previously, we had decided to just split our joint bills 50:50 (rent, utilities and groceries), but going forward we will split it 66:33 so that she has more cashflow available to put into her superannuation and starting her index fund snowball.

Even though she’s technically out earning me in terms of taxable income, she has a lot less invested so we want to prioritise her being able to invest more, so I will pay a bit more.

In addition to that, from the rich life series, barefoot investor and reading some blogs lately (MMM and mad fientist articles on spending) we’ve noticed a big theme around being able to actually spend and enjoy our money, so we’ve also doubled our joint splurge account (mostly for cafes and restaurants) to $200 a week, which brings our monthly joint budget to $2400 and $1200 respectively (I also have $220 of other personal expenses per month, and she has personal expenses of $250).

Once we eventually get married we will probably shift to just having both our incomes going into a joint saving account, and set up an auto transfer for regular bills into the joint checking account, an auto transfer for spending money into each separate individuals checking account, and then the balance going into investments in the lower taxable income earning spouse account.

We are still on the lookout for our dream hobby farm property, but we are not so sure it needs to be located in the Adelaide hills anymore. So we are expanding our search to include areas around a few hours from Brisbane to see what’s available. I have been amassing cash now, collecting dividends rather than reinvesting, and hopefully we find something this year.

I’m pretty grateful for having some close mates that I could lean on during these tough times

Anyway so yeah that’s my update, fair bit of drama in the CaptainFI household, but adjusting to the new life of semi-retirement, and enjoying now being settled and pottering around the home doing the garden, spending time with the dog, reading (still got 120 books on my ‘to read list’ – will be posting reviews as I complete them) and of course getting back into a bit more regular writing for the blogs and doing a bit more podcasting. Life is so much better now without the stress of work, and if I am brutally honest, the stress of caring for a dying parent with an unhelpful family unit.

If you want to see what I am doing on the more day to day stuff, you can follow me on social media where I regularly post what I am up to.

Captain FI’s Investments

I try not to calculate a Net Wealth or Savings Rate Figure much anymore, because they are a bit of a useless metric for me now post-FI, and they are also not that helpful from a mental health perspective. I became very fascinated by my (and other peoples’) net wealth and savings rate figures during my journey to FI – border lining on unhelpfully obsessive at times.

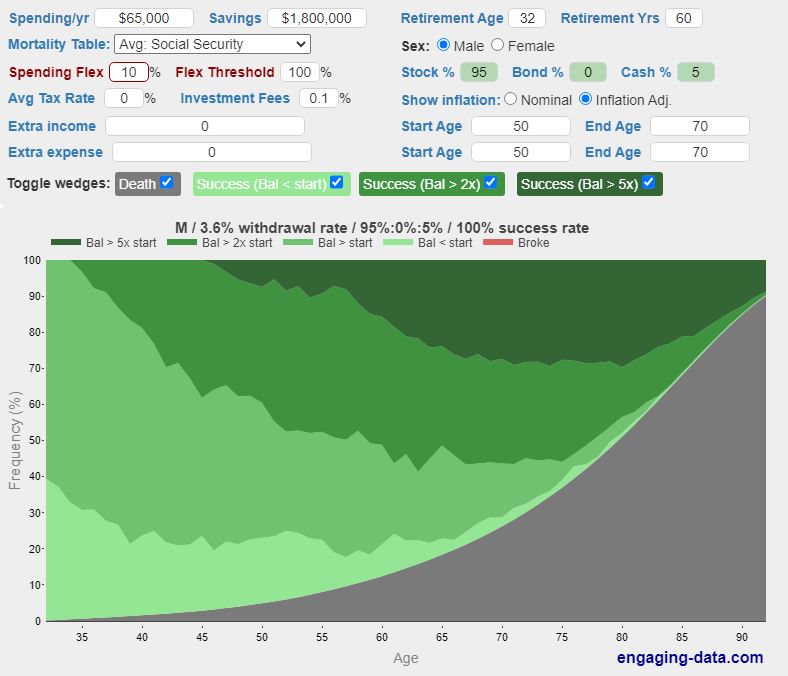

This was one manifestation of a somewhat chronic money anxiety borne out of my upbringing, and a desire for certainty and stability. Nevertheless, they were good metrics for tracking my journey to FI, they made for good blogging, helped my accountability, and the figures showed I made exceptional progress on the path to FI (the historical summaries can be found at the end of this update). However, going off the rough figures for investments I have access to currently, the below calculation from ‘Rich, Broke or Dead’ calculator shows that with my current risk tolerance, portfolio, planned ‘Family FIRE’ drawdown (over double my current lifestyle spending) and a very modest flex rate of only 10%, I will die before I run out of money. When I add in revenue from my website business in the ‘Extra Income’ tabs, it only makes the result go darker green, meaning there is a higher chance to end up with a portfolio balance at a higher multiple when I die.

My current investments (outside super) are split between 6 main areas;

- The FIRE Portfolio: Global, USA and Aussie Index fund ETFs

- Real estate – Duplex

- My business – Portfolio of content marketing websites

- Angel Investment

- Cryptocurrency portfolio – Bitcoin and Ethereum

- Cash (Australian Dollar, held in mortgage offset account)

NB – Approximately a year ago I ended up divesting in various things such as RoboAdvisors, Managed funds, Metals/resources, and a few other speculative investments or experiments I had in order to simplify my finances.

The ‘FIRE’ Portfolio (Exchange Traded Index Funds)

My ‘Financial Independence Retire Early’ ETF Portfolio is a simple, passive share portfolio split between three parcels of low-fee, index-tracking Exchanged Traded Index Funds (ETFs) to achieve global diversification. I began switching to this passive index approach to investing in 2018, firstly by adding new contributions, and then over time by divesting in other assets (individual shares, managed funds, LICs etc) and rolling the investments over to it.

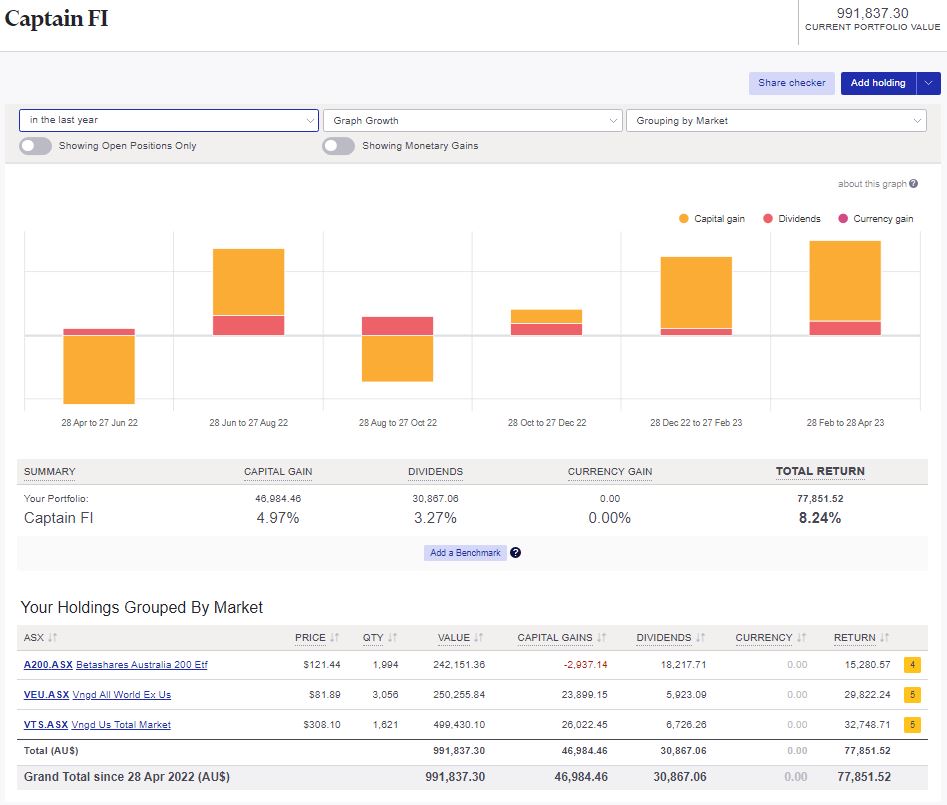

- I track my share portfolio using Sharesight, which means my portfolio accounting and tax reports are completely automated.

I am considering lowering my portfolio weighting of Australian shares in A200 to 10%, and increasing the weighting to international shares in VTS to 60%, and in VEU to 30%.

Since I am doing these updates less often, I decided to ditch the monthly portfolio data. Really, it is too short of a time period to even bother looking at or commenting (speculating?) on. Interestingly, at the end of April the portfolio did spike up to the $1M level, but as we know the market moves and its sitting at approximately $992K now. I did get the milly on a screnshot though haha!

The rolling 12-month performance shows the FIRE portfolio is trending back up towards long-term averages, recovering from some earlier dips in the first half of the year. Aussie shares capital values are down slightly (1.3%), but compensated by a record 7.5% or so dividend yield. Obviously, the elephant in the room here is inflation which is currently much higher than the sustainable long-term averages (around 7% or so), meaning the portfolio actually went DOWN in terms of real purchasing power in Australia in the last 12 months. Personally I have been a bit shocked at the price increases since I am naturally a pretty frugal person, but realistically we still live a very modest lifestyle so these price increases haven’t really affected us too much.

Total long-term performance sitting at where I would expect at around 10% – split between 4% of dividends and 6% capital growth. I am a bit surprised at how high the dividends are to be honest, because 75% of my portfolio are global shares which typically have much smaller dividends. There have been some surprisingly large dividends being paid out of the Aussie index funds over the life of this portfolio which has definitely skewed the total dividends up (in the share sight report below you can see 40k from A200 versus 8.5K from VEU and 8.2K VTS respectively).

With this split, long term I was kind of expecting closer to 3% dividends and 7% capital growth – however it is worth noting that it’s only in the past few years that I have started changing my portfolio splits to be much more heavily weighted in international shares (in the beginning the reverse was true and it was mostly Australian shares) – so over time I expect the dividends to come down a little bit.

When all is said and done, the long-term total return of 10.12% since inception is great, and it is much higher than both the current (7%) and the long-term average (2-3%) for inflation, meaning the portfolio has increased its real-world purchasing power, and has thus grown my wealth.

Investment property

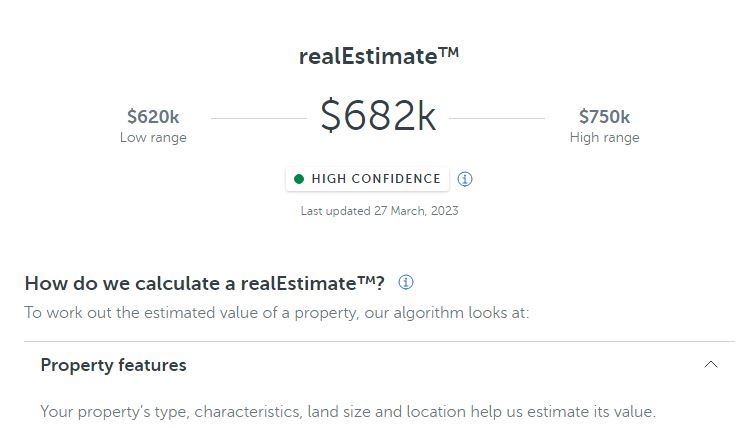

I recently wrote a full separate article on the IP build. The current online estimate is $682K, although the bank has currently accepted the ‘High Range’ estimate of $750K for financing purposes, and we have seen some similar properties sell for over this in the area – which is really just blowing my mind given they are tiny duplexes. Honestly with the increased cost of construction (up 50-100% annually due to inflation, labor and supply shortages) and healthy immigration numbers, this makes sense (and we have upped our home insurance accordingly).

I currently have the IP mortgaged with a split loan, and currently have been saving up in the offset – accumulating cash for our PPOR ‘forever home’ whilst we decide what to do (as I mentioned in the personal section above, we aren’t sure we are fully set on the Adelaide Hills anymore). One course of action is to sell a big chunk of shares, and draw the IP offset accounts down to fund the aquisition of a PPOR (new home loan would be tricky for me not working, but my partner is earning a decent wage so will have to see what the broker comes up with). Either way, time will tell.

Currently I have a 5.4% Interest rate, and with the property tenanted and the mortgage the way it is fully drawn it would be cashflow neutral – although with depreciation and claiming expenses at the EOFY I would get some tax back – but not heaps considering I am on a 21% tax bracket, so its would actually be slightly positive cash-flow after all is said and done. However, as I mentioned the offset account is growing which reduces interest payable and by definition makes it more positively geared.

Online Business (website portfolio)

I have a small business that runs a website portfolio of 16 content sites that make money from display Advertising through managed ad networks such as Adsense, Ezoic and Mediavine, and affiliate programs such as Amazon Associates and other direct affiliate deals. I’ve written a pretty detailed article here about how to make money online.

Does this mean those lurkers in Reddit and other internet trolls are correct and that I am a scam, and not doing FIRE as I haven’t “really retired” ? Sure! I like to think of it as Semi-Retirement anyway, because we all need something productive to work on thats fun to do. FIRE is more about the FI and less about the RE, but as I have always said, RE has many different versions (Retire Early vs Redirect Effort, Recreational Enoyment, Redirect Energy…Retire… Eventually?)

Anyway, after getting a pretty gobsmacking valuation on a couple of my sites bringing the portfolio valuation into the Seven Figures region, I started to consider the possibility of selling some and stashing that money towards the farm. I had not really thought about the possibility of ‘selling out’ in much detail before, but have decided to sell some of the smaller sites to reduce workload, provide additional revenue and improve cash flow and profits. This ‘pruning’ lets me focus on writing for my passion sites (CaptainFI, the gardening site and my aviation site), as well as raises some cash towards the dream hobby farm.

As a result, I have a few sites I am open to selling to anyone who wants to get started with this side hustle with their first starter site or older, more established content site. They range from 2 to 4 years old, with various backlink profiles, number of published articles, and traffic. You can check out this article on website operation if you are keen as I’ve listed all the details in there. Feel free to send me an email through the contact form or get in touch on social media if you are interested.

I learned these skills through the eBusiness institute over the past 4 years – I have done a pretty comprehensive review of the eBusiness institute as well as interviewed Matt and Liz Raad about this on the podcast about online business and websites if you want to learn more about this. They provide a free introductory course for CaptainFI readers. I have also recently recorded a few more interviews with Matt which I will be publishing on the podcast in due course.

Angel Investing

I have a small ‘Angel Investment’ in the Financial Independence brokerage platform Pearler. This was the maximum allowable private investment of $10,000 (AUD) which was made in July 2021 with the total number of ‘private equity’ shares based on their June company valuation. This was all documented, recorded and disclosed as per ASIC requirements. I also disclosed it in my NW updates and my Pearler review.

I am not tracking the exact company valuations for Pearler, but I know the company has had its valuation more than triple and has raised over $10m through initial VC rounds, with more to be raised in later rounds, so I assume the shares are worth a bit more. How much exactly though? I am not sure. I expect probably around $30,000 at minimum.

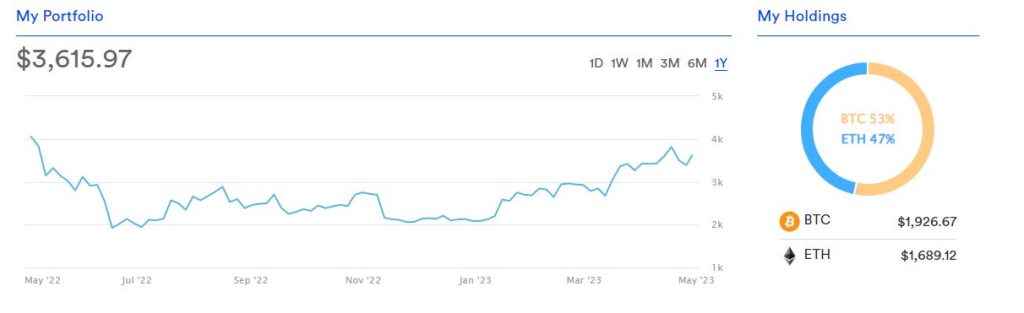

Cryptocurrency Portfolio

A bit of a bounce back and upward trend which is good, but still sitting at about a 28% capital loss on the crypto.

- Total invested to date: $5056

- Current Valuation $3615

- Current loss = -$1441

Cash – Mojo and emergency fund

Cash reserves is are well and truly replenished, as I mentioned I have started accumulating cash in my mortgage offset account, and haven’t drawn down any of my second split loan. This cash will be used for the PPOR when ready, and I will be keeping approximately 1-2 years cash balance a minimum, which will be at least $50k.

For day to day spending, I am still just keeping a few thousand in my personal transaction account, and my partner and I have a joint bank account we each contribute to for household bills.

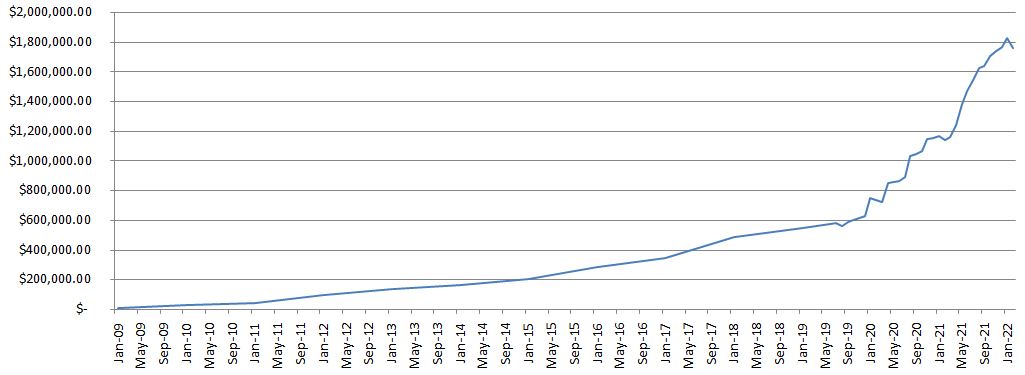

Captain FI’s Net Wealth progression

During my journey to FI I kept track of my net wealth progression via monthly updates and a graph which was rather crudely constructed in Excel. It demonstrates the ‘somewhat exponential’ journey over the past 14 years. You can access the archives for my Net Worth updates here to see how it’s gone over time. Check out the graph and all the updates below to see how it has gone since the beginning.

I haven’t continue to update a Net Wealth figure monthly post-FI because it isnt that helpful and starts to cause me money anxiety. Instead, I will continue to put out semi-regular updates about my investments and life post-FI.

| Date | Net worth | Difference | Saving Rate | Notes | |

| Jan 09 | $5,000.00 | ? | Estimate NW based on historical Super, Bank statements and assets at the time | LINK | |

| Jan 10 | $24,000 | +$19,000 | ? | Estimate NW | LINK |

| Jan 11 | $40,000 | +$16,000 | ? | Estimate NW | LINK |

| Jan 12 | $92,000 | +$50,000 | ? | Estimate NW | LINK |

| Jan 13 | $130,000.00 | +$38,000 | ? | Estimate NW | LINK |

| Jan 14 | $161,000.00 | +$31,000 | ? | Estimate NW | LINK |

| Jan 15 | $200,000.00 | +$39,000 | ? | Estimate NW | LINK |

| Jan 16 | $281,000.00 | +$81,000 | ? | Estimate NW | LINK |

| Jan 17 | $340,000.00 | +$59,000 | ? | Estimate NW | LINK |

| Jan 18 | $482,000.00 | +$142,000 | ? | Estimate NW | LINK |

| Jan 19 | $542,000.00 | +$60,000 | ? | Estimate NW | LINK |

| Jul 19 | $578,900.00 | +$36,900 | 84% | Finally began tracking NW this like a proper adult. | |

| Aug 19 | $560,100.00 | -$18,800.00 (-3.2%) | 78% | Share market slight correction, Ok savings. | |

| Sep 19 | $584,744.88 | $24,644.88 | 72% | Share market rebound, savings rate not so good. | LINK |

| Oct 19 | $600,386.00 | $15,641.12 | 84% | Good saving this month. Normal salary, plus allowances, dividends from index funds, tax refund, eBay selling and was working abroad in asia where things are cheap. | LINK |

| Nov 19 | $612,917.21 | $12,531.21 | 76% | Falling short of my savings goal of 80%. Mostly domestic legs this month with higher costs. Also invested in hydroponics. | LINK |

| Dec 19 | $625,350.00 | $12,432.79 | 76% | Good savings of cash (for development) and investment, however higher spending due to Christmas period (Travel and Gifting). | LINK |

| Jan 20 | $865,212.00 | $239,862.00 | 55% | Super settlement was a HUGE boost to NW. $9K growth from stock market. Expensive month lots with lots of unexpected bills – weddings, travel, Booking flights, fines etc. | LINK |

| Feb 20 | $851,802.0 | -$16,592 (-1.9%) | 52% | Large increase in spending on myself this month, still managed to tuck away $5K to put into shares and property. Corona Virus market scare resulted in a correction and gave NW a small negative trend. Time in the market not Timing the market! Became Single again. | LINK |

| Mar 20 | $819, 354.6 | -$31,806.95 (-3.7%) | 80% | Another small step backwards in the NW due to the ‘corona crash’ in full swing. FIRE Portfolio of ETF/LICs down about 15% this month, however due to high savings rate and structure of my superannuation annuity the NW is only down 3.7%. Savings rate good at 80%, higher than usual income (with some slightly higher spending, too). Picking up shares on discount – this is the best outcome for someone in the accumulation phase with good income! | LINK |

| Apr 20 | $847,023 | +$27,668 | 85% | $11,000 in rebound of stock market capital prices alone (up 6%), plus first quarter dividends paid (heavily reduced due to banks withholding dividends). Great savings rate due to COVID-19 lock-down = no spend. Increased entrepreneurial efforts and selling down of physical possessions provided side hustle income. Two standard paychecks from flying activity; domestic day trips only so no allowances. All cash unfortunately had to go into the property development due to contract timing, I am chomping at the bit to buy some more index funds before they go back up in price too much – hence why I am selling most of my toys! | LINK |

| May 20 | $857,859 | +$10,836 | 92% | Some Great sales as I let go of my Super Sport Motorcycle, Some gym gear, expensive flying equipment and a few other various bits and bobs and invested this money. Flying still reduced, but increasing from April. The share market grew as I continued to make my fortnightly investments. I also wrote down the ‘value’ of some of my possessions (liabilities) such as my car, tools and furniture by around $10K to align them to market price (“tell him hes dreaming…!”). | LINK |

| June 20 | $858,650 | +$791 | 90% | Small Net Worth gain as I continue to declutter and simplify my life, despite being off work due to a family emergency. Share market not doing much. | LINK |

| July 20 | $888,218 | +$29,568 | 68% | Majority gain due to share market going back up, low spending due to being on the family farm and at home because of lock down. | LINK |

| Aug 20 | $1,029,293 | +$141,075 | 74% | Became a millionaire. Achieved this massive milestone I set out for myself in Dec 2019. Included unrealised gains in my property development as well as website business. Good savings rate due to not much spending, invested in Aus and total world shares. Investing in my web business. Starting to shift focus away from $$$ and more into looking after my mental health. | LINK |

| Sep 20 | S1,045,486 | +$16,193 | 60% | Officially took time off work for the rest of the year to be close and look after family during major operations. Continued to sell down physical possessions and work on digital business while at home. NW gain mainly due to valuation of websites. | LINK |

| Oct 20 | $1,064,399 | +$18,913 | 80% | Base income (retainer) and leave loading, dividend and websites provided income, as well as raiding my P2P lending capital. Significant bill for property due to design not meeting standards which effectively lowers my equity position, as well as fence being stolen. | LINK |

| Nov 20 | $1,143,433 | +$80,394 | 82% | Big gains came from share market growth (influencing both the Financial Independence share portfolio and Invested superannuation), Business gains (due to increased earnings) and a $30K boost to my annuity thanks to me logging in and checking the fine-print on the accumulation stats. I only invested around $7K. Insane that in one month, I accumulated nearly more net worth than I did in four years from 2009-2012 | LINK |

| Dec 20 | $1,152,920 | + $9,487.32 | 84% | Share market slight drop, Earnings from Business, Contract work, Selling possessions. No share market investments this month (oops! I forgot and money was tight). Invested a lot into the website business this month (way more than planned) and it is still running at a decent loss (plans to turn it cash flow positive in 3 months). | LINK |

| Jan 21 | $1,165,678 | +$12,757 | 79% | Great returns from the share market. Earnings from Business, Dividends, Flying wage, flipping items on consignment. Regular share contribution, investing in micro investing platforms, P2P lending, Investment property and big reinvestment into the business (still running at a loss) | LINK |

| Feb 21 | $1,135,272 | -$30,406 | 76% | Significant write down on property development due to council DA rejection and redesign requiring more money and creating less equity. Offset by small increase to Business value and investments. Simplified my investments and switched over to Pearler. | LINK |

| Mar 21 | $1,155,594 | +$20,322 | 71% | Continued investment into the portfolio as well as growth of investments and business. Gave my notice at work and looking for part time job at home for ‘Barista FI’ | LINK |

| Apr 21 | $1,242,220 | +$86,727 | 74% | Property development back on track | LINK |

| May 21 | $1,379,469 | +$137,248 | 72% | Massive gains in the website portfolio due to revaluation based on recent business income, big growth of superannuation due to annuity increasing (salary increment) and shares generally went up. Crypto went down by about 40% or so. | LINK |

| June 21 | $1,469,989 | +$89,757 | 41% | Quit flying role and moved to Adelaide. Great month for investments, websites producing serious income so accordingly they are valued higher. Spent a lot on furnishing the new apartment and on enjoying some more luxuries. Seeing a therapist to help deal with anxiety from leaving work. | LINK |

| July 21 | $1,543,959 | +$74,732 | ??? | Set myself up in Adelaide. Did basically nothing for the whole month except spent time with family, relax, sleep and go to doctors appointments. Massive boost to website portfolio AdSense and affiliate incomes, as well as general share market performance. | LINK |

| Aug 21 | $1,624,116 | +$70,156 | ??? | Relaxed again, focused on mental and physical health, and spending time with family and my partner. Big increases to spending (too afraid to calculate a ‘savings rate’) but also big increases to NW through website portfolio income growth. Finally got the slab poured on the investment property (foundation). | LINK |

| Sep 21 | 1,640,663.85 | +$16,547 | ??? | Stocks, super etc went down, but business income from websites increased, plus business valuation increased. Property build. got to frame stage, and I also got a dog! Expenses for vet surgery well worth it. Moved into a nicer apartment | LINK |

| Oct 21 | $1,705,907 | +$65,243 | 30% | Big boost from website valuation due to securing new affiliate contracts for recurring income, shares went up nicely. No massive changes to this month. Calculated a savings rate and found myself pretty low due to spending a lot on my garden and going out quite a lot – I don’t think I will calculate this savings rate figure any more. | LINK |

| Nov 21 | $1,739,144.23 | +$33,236 | N.A. | Great month. Relaxing (somewhat). Spent a lot of money doing ‘fun’ things like winery tours, a fine dining experience and self education. Shares moved sideways (well slightly down) but everything else went up. Building got to enclosed stage (roof, walls, windows and doors) but have had some issues with build quality and weather / covid delays. Put a $1000 deposit on the puppy. | LINK |

| Dec 21 | $1,764,516 | +25,372 | N.A. | Spent nearly the whole month with family, did some work on the website portfolio. Traffic recovered from google algorithm changes. Invested $10K into Stockspot and Sixpark, $1K into ACDC, $100 into Comsec pocket and $100 into Bamboo, $260 into BTC, $4K into ETFs through pearler. Paid the $3000 balance for the puppy. | LINK |

| Jan 22 | $1,826,633 | +$62,117 | N.A | Stock market slightly down, Massive boost to website traffic (overall its more than doubled). Invested $10K VTS, 2K VEU through pearler, Paid for Angels cancer surgery, bought more BTC and ETH, bought a parcel of ETHI on commsec pocket. | LINK |

| Feb 22 | $1,757,210.57 | -$69,422.93 | N.A | Stock market down, Website business revenues down and additional spending on content and staff for business, Additional property development bills, some unexpected expenses, Wrote down the value of some of my personal property (and gave stuff away). |

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.