We have all heard it before – past performance is no indicator of future performance. All things considered, no one can really predict the market. All we really control is the price and fees we pay. So does that mean Low fee index style investing the best way to go?

Stock market Index funds like some ETFs (or even old school LICs) are a type of investment product that allows investors to get certain exposure to ideally align their portfolio’s performance to a certain part of the market. For example total stock market index funds – in this case, rather than trying to ‘beat’ the stock market, you ARE the stock market.

In this article, we will explore just what is a stock market ETF, what is a LIC, why some investors love them and include them as part of their investment strategies.

CaptainFI is not a Financial Advisor and the information below is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Exchange Traded Funds

An Exchange Traded fund is just a parcel of shares, you can think of them as a wrapper. What really matters, is whats inside the wrapper or basket. Just because something is an ETF, doesn’t automatically make it an index fund. Many ETFs track various indexes, and some track total stock market indexes such as the Standards and Poors indexes.

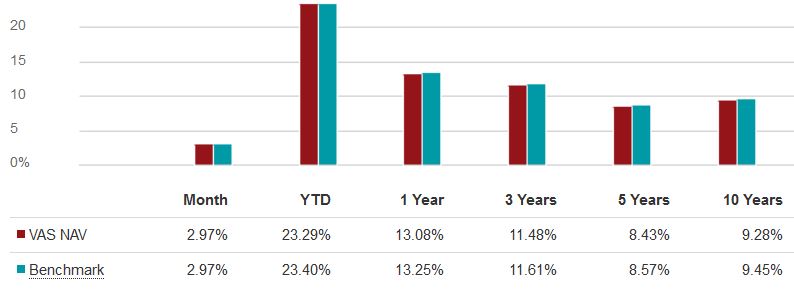

An example is the Vanguard Total Australian Market (ASX:VAS), which tracks the performance of the top 300 Australian shares according to the Standards & Poors Australian Stock Exchange (ASX) 300 Index. Another is the BetaShares A200 (ASX:A200) which tracks the top 200 Australian shares according to the Solactive Australia 200 Index.

Both of these two stock market index funds are types of ETF – Exchange Traded Funds. Think of them as parcels of shares – each share of VAS or A200 is actually a representative share of each of the hundreds of company that the fund owns. Lets use VAS as an example to learn more: VAS is comprised of the top 300 Australian companies by market capital, according to the S&P/ASX 300. When you buy a share of VAS, you are actually buying a small share in every company in the ASX300 – the below table lists the top 10 major companies owned by the fund which make up just over 43% of its total holdings.

| 1 | Commonwealth Bank of Australia |

| 2 | BHP Group Ltd. |

| 3 | Westpac Banking Corp. |

| 4 | CSL Ltd. |

| 5 | Australia & New Zealand Banking Group Ltd. |

| 6 | National Australia Bank Ltd. |

| 7 | Telstra Corp. Ltd. |

| 8 | Woolworths Group Ltd. |

| 9 | Wesfarmers Ltd. |

| 10 | Macquarie Group Ltd. |

So by purchasing one share of VAS, in one trade you have accessed hundreds of companies and widely diversified your portfolio. So then what happens? Well if you hold the ETF long enough, as you might expect, the underlying shares will produce returns (both capital gains and dividends) just as if you had owned each of the individual shares directly. The fund collects the dividends on your behalf, automatically re-balances itself according to the S&P/ASX300 Index, and then pays you the dividend.

An ETF like VAS is an example of an ‘open ended’ fund. When you purchase a share of VAS, the fund creates and allocates you that share, and your money is pooled with other investors to purchase the underlying shares (in line with the current market indices) which are then added to the funds holdings. The share price of VAS will vary according to the variation of the share price of its constituents, or Net Asset Value (NAV), and in line with efficient market theory, it will always trade at a Price equal to its Value (share price = NAV).

Most ETFs have ultra low fees due to the simple, and mostly automated nature of managing the funds. For example VAS has a Management Expense Ratio (MER) of .1%, or 10 basis points – that is, to administer your portfolio, Vanguard will charge you a .1% management fee every year, or $10 for every $10,000 you have invested. Given an actively managed portfolio may have MERs of around 2-5%, you .1% is bugger all! In comparison, A200 offers an even lower MER of .07%, 7 basis points or $7 for every 10,000 invested, as they track the top 200 companies rather than the top 300 companies (the returns of which are mostly identical, but more on this later).

So in summary, an ETF is a parcel of shares which gives investors access to a diversified list of holdings at rock bottom prices. But that’s not the end of the story – what if I told you that you could have your cake and eat it it too: Enter, the Listed Investment Company.

Listed Investment Companies

A Listed Investment Company behaves similarly to an ETF, but it has one fundamental difference: it is a closed ended fund. That means there is a limited number of shares. To buy into LICs, it means you have to buy someone else’s share, or buy a new share the company has created if they are trying to raise capital. LICs vary immensely, and can range from small companies with only a handful of board members or employees, to the complete opposite of the spectrum. In this discussion I will limit our discussion to the former, as they tend to have the lowest fees and offer the best value for money.

The Australian Foundation Investment Company (ASX:AFI) is one of Australia’s oldest LICs. It offers a relatively low MER at .13% or 13 Basis points ($13 for every $10,000 invested) and is a fantastic value for money investment, producing consistently good returns for its shareholders.

Similarly to the ETF, the a LIC has a Net Asset Value (NAV) which is essentially the sum total of the funds holdings divided by the number of shares (this is an approximation as there is for example complications involving tax but lets use this definition for beginners). However being a closed ended fund, it is subject to market pricing. Depending on investor sentiment, the share price may rise or fall according to standard economic principles of supply and demand. This means a LIC can trade at a premium (in excess) or at a discount (below) its NAV.

Performance: So what are your expected returns – this all depends on the index you are tracking. The S&P/ASX300 ten year return has been approximately 9.5%, that is an annualized 9.5% return on investment. The index isn’t perfect however, and although it aims to track this index, it may fall short or even outperform it. Usually though, the drag caused by portfolio management will cause a small under-performance, usually fractions of a percent.

ETFs vs LICs

So Index funds – often purchased through LICs and ETFs these no frills investment strategies just aren’t all that profitable to those with their hands in the biscuit tin! Many brokers and financial planners would rather sell you actively managed funds which come with higher fee’s or management expense ratios and performance incentives, all of which erode the performance of your investment.

Even the Barefoot Investor himself made a LOAD of money selling the stock tipping website ‘The Barefoot Blueprint’ which gave paid barefoot investor subscribers tips on which hot stocks they should load up on. It is interesting that he also suggested investing in ‘Breakfree portfolio’ of stock market index fund ETFs as a smart investor strategy.

It’s not without its risks, however. It’s always worth remembering that an index is a representative share in a real world company. These could do great and expand, producing profits for shareholders, or they could go bust. But realistically by owning an index of hundreds of companies, the likelihood is not all will collapse simultaneously.

Also, by owning the index, you won’t have control over the assets in your portfolio – as ETFs and LICs are often weighted by market capital, and as a result large bank stocks can make up a high percentage of your portfolio. It has also been suggested that investors lose the ability to vote with their feet with regards to poor management or corruption in a company; investment in ETF is one on ‘autopilot’ and many investors are blind to goings on within those companies.

So which is better?

There is a fairly fierce ongoing debate in the FI (Financial Independence) community over which is better.

LICs have the ability to trade below their Net Asset Value – meaning you can pick them up at a discount sometimes. This is an attractive feature. LICs also are actively managed – which can be seen as both a pro or a con, depending on your personal investing attitude. Old school Aussie LICs try to optimise their investing for increasing dividends to outpace inflation, and pass these (often) fully franked dividends to shareholders as a tac effective growing passive income stream.

The transparent, extremely simple, basic and ultra low fee nature of index tracking ETFs is hard to pass up though. These funds still pass on big franking credits, but may not be as tax-effective as dividends can be ‘lumpy’ (they aren’t allowed to be retained to be smoothed over time – they must be paid out to ETF shareholders). By tracking the index, you also don’t get someone tampering with the portfolio and potentially stuffing it up. Long term performance also shows that the basic, low-cost index-tracking do ETFs outperform LICs in terms of total return, although the LICs tend to have more stable, smoother and higher dividend yields.

At the end of the day, I tried stock picking at the start of my investing career. It was kind of fun to start with, but the novelty wore off. On average my wins and losses got confusing and hard to track. After sussing it all out in Sharesight I worked out that I (like the majority of investors) underperformed a basic stock market index fund so I embraced being average and decided an index-style investing strategy was for me. I did this through both ETFs and LICs, and after learning a little more about LICs and investing in some over several years, I decided to stick with some of the most basic index fund ETFs available.

Summary

Stock market Index funds like some ETFs (or even old-school LICs) are a type of investment product that allows investors to get certain exposure to ideally align their portfolio’s performance to a certain part of the market. For example total stock market index funds – in this case, rather than trying to ‘beat’ the stock market, you ARE the stock market.

LICs are companies that typically actively manage their funds work as closed-ended funds which can trade at a discount or premium to their underlying asset values, and they can retain capital for dividend smoothing and tax-effective income. ETFs are typically passively managed index funds that use an open-ended trust structure that must distribute all dividends from underlying shares held. ETFs tend to outperform LICs in terms of total performance in the long term, but some people choose to invest in LICs because it can be a smoother ride and because of their active management or dividend focus

If you want to delve a little deeper into the field, check out Paul Rickard’s (former CEO of Commsec) explanation in the video below.

Financial Disclaimer

Financial Disclaimer: CaptainFI is NOT a financial advisor and does not hold an AFSL. This is not financial Advice!

I am not a financial adviser and I do not hold an Australian Financial Services Licence (AFSL). In this article, I am giving you factual, balanced information without judgment or bias, to the best of my ability. I am not giving you any general or personal financial advice about what you should do with your investments. Just because I do something with my money (or use a particular service or platform) doesn’t mean it is automatically appropriate for your personal circumstances. I do not recommend nor endorse any financial or investment product, and my usage or opinion of any product should not be interpreted as an endorsement, advertisement, or intent to influence.

I can only provide factual information based on my journey to Financial Independence, and that is provided for general informational and entertainment purposes only. I make no guarantee about the performance of any product, and although I strive to keep the information accurate and updated as it changes, I make no guarantee about the correctness of reviews or information posted.

Remember – you always need to do your own independent research and due diligence before making any transaction. This includes reading and analysing Product Disclosure Statements, Terms and Conditions, Service Arrangement and Fee Structures. It is always smart to compare products and discuss them, but ultimately you need to take responsibility for your use of any particular product and make sure it suits your personal circumstances. If you need help and would like to obtain personal financial advice about which investment options or platforms may be right for you, please talk to a licensed financial adviser or AFSL holder – you can take the first steps to find a financial advisor by reading this interview, or by visiting the ASIC financial adviser register and searching in your area.

For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

2 thoughts on “Get rich by Investing in LIC and ETF index funds?”