Here it is Ladies and Gents, the first podcast for Captain FI! This Podcast is the first in the series on Financial Independence which kicks off with a discussion on Financial Independence for Beginners.

- Podcast also available on Whooshkaa if the embed fails

Show notes

- Vanguard Research on Lump Sum Investing versus Dollar Cost Averaging in a .PDF here

- Mr Money Mustache: The shockingly Simple Math behind Early Retirement

Script

Ladies and Gentlemen this is your Captain speaking, welcome aboard Captain FI the financial independence podcast.

G’day guys and welcome to an episode of Captain FI, the Financial Independence podcast where I open the cockpit to chat to some of the best and brightest in personal finance as well as those who have reached Financial Independence or are on their way to reaching financial independence.

Today’s forecast is financial independence for beginners.

So what is financial independence? Financial Independence occurs when your investments generate enough income that it exceeds your cost of living. You can really do this two ways; you can have a really high income from your investments, or you can have a more moderate income from your investments and a fairly low cost of living – you can see there actually an infinite number of combinations to meet the criteria of reaching financial independence

really though, what does it do for you? FI gives you choice to direct your time and therefore energy into the things that you truly value rather than the things you don’t (like working 9-5 grind) because your income is coming from passing investment sources such as real estate of low cost index funds you don’t actually need to go out and earn a living you don’t need to get that paycheck you don’t need to have a boss and you don’t need to spend all the money you would trying to earn the money like a car professional subscriptions, insurance all that stuff. and its hard, I think the FI movement is really just about uhh commonsense really using the core principles of mindfulness good old efficiency and optimisation and minimalism, really living below your means is how you achieve FI

it can seem pretty daunting at first and when you start getting into the financial independence community and start reading online there are some pretty impressive stats out there from people like Mr Money Mustache and the Mad Fientist, and closer to home the Aussie firebug from Australia. they have some pretty amazing saving rates and investments cad it can be really daunting for someone who is looking at it for the first time. Investments really are a snowball though and once you get started and that ball gets rolling it gets massive, and umm when you see those dividends and you see the growth in your assets – it changes the way you think. I know personally the first dividend payment I got I was hooked.

I was like oh my god your telling em I can buy this thing and 4 times a year its just going to give me free money like it just throws off free money and that just comes straight into my account and I can use that and spend that on anything or reinvest that and take advantage of compound interest to get those investments to grow even quicker. I guess when you start it can be so daunting and people are inherently afraid of something that’s new and afraid and you know change even in my role as a professional pilot something we often joke about in the cockpit is that there is two things we hate and that’s change and the way things are – pilots usually find a way to complain about stuff

You don’t need to be afraid to break out of the formation with everyone else – just because everyone else does something doesn’t mean its a good idea. really when your looking to take your first steps to financial independence its an introspective period you need to review your own personal goals and values and figure out if its for you – not everyone does want to quit their job, but reaching financial independence certainly provides a big factor of safety. me personally its something I want to achieve before starting a family.

Some people will often say money isn’t everything alright Captain FI you seem to love optimising an compounding and buying investments and shares, and your very good with numbers but you know money is not going to buy you happiness. first of all id say if you think money cant buy you happiness I’d say your clearly shopping at the wrong places because money can buy me an aeroplane I have a lot of fun flying aeroplanes I can tell you that! Actually flying instructing has been one of the most awesome, rewarding jobs I have ever done unfortunately its not very lucrative but maybe after I reach FI that could be something that I look at..

So yes ultimately I agree money doesn’t buy you happiness per se, but what money can do is help you avoid things which are unpleasant – for example working lng hours or living away from home away from your family. so At its core I think happiness is a result of good health, relationships and wealth. So you really if you want to take a step back with psychology and I am NOT a psychologist by any stretch of the imagination but I do remember learning as an instructor about Maslows hierarchy of needs

so Maslows hierarchy is about fulfilling basic requirements first and then progressing up the pyramid or hierarchy to more creative / fulfilment endeavours for example shelter and food come in right at the bottom of the core foundations and then as we go up we are looking at relationships and finally self actualisation.

A really good example of Maslows hierarchy in action i saw when I was teaching a young lady to fly. She was having a little buit of difficulty with landing the aircraft, and as yo might imagine landing an aircraft is one of the most if not the most important skills that a pilot can have to safely bring the aircraft down after a long flight. Its usually the thing your remembered by whether that’s a good thing or not haha! Maybe you’ve gently greased the wheels onto the runway and its a nice smooth landing and nobodies felt it or maybe you’ve messed up and just plonked it on and everyone’s felt it.

So it took a couple of sessions working with her to really fix the issue, what was happening was her fear and stress of hitting the runway was actually kicking in her bodies natural fight, fright or flight mechanism which is a physiological thing its physical not a mental, but its pretty unfortunate for a pilot. As she was approaching the flare and the landing she would freeze up on the controls and as a result I would need to take over. So one of the ways we overcame that was I thought gee shes afraid of hitting the ground – lets just show her what hitting the ground feels like! So I just had a bit of fun, we just came in and did some harder landings which you know you usually try and avoid, just to demonstrate that hey the worlds not going to end if you bang it on.

So after a few of those she realised that its actually a bit of a non-event and the distraction really went away. she was able to complete the landing training module and went on to successfully complete her pilot training and she is now even flying for the air force. it just goes to show focusing on the basics, based on the foundations of Maslows hierarchy means first means you can easily progress to those higher rungs

so why is this relevant to FI? Well money cant buy you happiness but things It can buy – it can pay your rent, it can buy your food, it can pay for gas in your car, it can pay to register your car, it can buy you FOOD (I love food). the fact is that money in our society is a way that we exchange our time. So when you think about currency as well actually this isnt a Dollar, this is ‘X’ amount of my time – if your earning $20 an hour in retail, and you decide to go out to see a movie and your choc tops and popcorn and the ticket the bill comes to $40 somehow, you go wow I am not buying this with $40 I am actually buying this with 2 hours of my time. And its actually more than that because remember you’ve paid income tax- but that’s a whole another story and we can leave that for another podcast

so the money might not make you happy per se, but its going to allow you to satisfy the foundational criteria of Maslows hierarchy – food, safety, shelter, and therefore it lays the preconditions for happiness. Its going to allow you time to focus on those creative endeavours or passion projects

A lot of times in the FI or the FIRE community you hear about people wanting to achieve Financial Independence so they can quit their job. Now you know not everyone wants to quit their job, so when you think about it financial independence could give you the flexibility to work the hours that suit you – such as part time or reduce the hours – some people even choose to have a 5 day weekend. If your boss doesn’t like it well – there’s a reason its almost universally referred to as FU money. That’s the whole semi retired, kinda care, kinda don’t mentality

another benefit to reaching FI is that it gives you the ability to redirect your employment. This means you have the option to branch out into a new career field, commonsense a course of study or even start a business without the worry or time constraint of having to earn a wage and having to put food on the table. For many people, the opportunity to redirect their time and energy into this new forms of creative employment can be incredibly satisfying and has led to the creation of many successful businesses, which in-turn can produce an income and be systematised and put on autopilot to make passive income

ultimately who doesn’t holidays? reaching financial independence means that you can go on holiday forever if you want. Geographic arbitrage is detailed in the four work work week book [add to show notes] is the process of living on a permanent vacation and taking advantage of the difference in exchange rates and the prices of goods and services. For example in Australia a lot of people look at moving or holidaying in South East Asia where you can stretch the Aussie dollar a lot further- just like how American vacationers may choose to head south down into Mexico or other parts of south america where they can stretch their dollars even further

I guess the last bit about reaching FI is you can always retire eventually – as we said quitting your job is not for everyone, but the numbers don’t lie and when your passive income from investing exceeds your cost of living – you don’t need to work anymore. You’ve reached FI. That’s it. you’ve hit it. Its huge jump and not something everyone is ready to go for straight away. You might have hit FI but there is still a little lingering doubt or ‘is this really going to work, have I done my numbers correctly’ thought – if this sounds like you this means FI might give you the option to retire eventually, when your ready. So the side bonus to that is because your already financially independent your portfolio is just going to grow larger and larger each day you continue work, giving you a bigger cushion and reducing your risk and even more cash flow and passive income. So it can be a very insidious situation, which really raises the question ‘when is enough enough?’ and it can lead to analysis paralysis, delay and hesitation so that’s just inherent some of those personalities but eventually you’ll have enough to take the leap

So thats a little bit about FI and happiness and why do it, the next question is how do I do it? So smart investors are able to reach FI by living below their means and continually investing in assets. Assets are productive and are basically things that make you money. That could be an investment property where you are renting out a house to a tenant that’s providing some cash flow and paying down your mortgage whilst your receiving capital growth – hopefully its cash flow positive so its providing you cash each week which you can be paying your groceries with. assets also include the stock market and everyone will probably know by the site I am an avid fan of low cost stock market index funds – these are ETF or exchange traded funds and LIC or listed investment companies which you’ll hear about quite a lot. Other assets can include intellectual property – maybe you have written a book or course and you are offering those for sale and you get the royalties from thats ticking over in the background. Other forms of assets include bonds and fixed cash but those are two things in the current climate of interest rates aren’t super lucrative but the point is , an asset is something that makes you money.

Directly opposed is a liability is something that costs you money. A liability for example could be credit card debt, a loan on a car or even a ridiculously big car that you don’t need – like driving around a big 4WD in the city when really all you do is drive 2Ks down to the shops and back on Sunday. By living below your means and investing in assets, eventually your going to hit FI.

When it comes to the steps the first thing is to educate yourself. That includes an introspection – you need to review your level of knowledge at the moment and be honest with yourself. You shouldn’t be investing in things you don’t understand. That is one of Warren Buffets best pieces of advice. For anyone who doesn’t know Warren Buffet he is sometimes referred to as the Oracle of Omaha and is undoubtedly the worlds best investor.He says you should never invest in something you don’t understand. Step one is educating yourself, review your knowledge, your values and your goals

Step two is make a budget! This is really key because this is part of the whole living below your means thing. You need to track your budget, track your expenses and track your needs. Creating a budget can be difficult but the first step really always is just getting a print out of your bank statement. I would say go electronic for everything and ditch the cash just use your card for a couple of months to get a really good understanding of your purchase history and go through your budget in detail to figure out where your spending your money. That’s going to give you a really good understanding of where that money is going. even the most sturdy ship can be sunk by lots of little holes in the hull – which means you can have a really high income,e, you can be a professional on 6 figures but if your going out and spending, 10, 15, 20 here and there regularly on crap like food or whatever, that really does add up over time. what does it cost to waste $10,000 a year? its something like $27 a day so it adds up.

Once you’ve got a really good understanding of just how much your actually spending, you need to reign it in. Step three is reduce your expenses. You want to be mindful with your expenses, but you still got to have fun. If you start being really brutal with your budget its probably not going to work out. You need to do these things sustainably, so maybe just aim to reduce your expenses by 20% or even just start with 10% and then each month or each couple o months your gonna aim to review this and bring it back by another 5% or another 10% until you get to a position that you are happy with. For example my goal i am striving for at least an 80%+ savings rate. So that means I want to save at least 80% of the income that hits my account plus my super contributions – I want that to be equal to or more than 80%. I’ve not been doing too bad, unfortunately a few months I’ve taken a few blows to the old savings rate but on average we are actually around the old 80% savings rate which is where I set my goal – remember back to step one educating yourself included really setting some of those goals

There are great ways you can get really creative with reducing expenses, I’ve published a lot of articles about reducing your cost of living and you know get more efficiency out of your purchases as well as maybe some things you can live without (iced coffee?) on your journey to Financial independence.

Step four is to create a savings buffer. This is really important. Because you’ve budgeted and reduced your expenses hopefully you’ve free’d up a little bit of cash, or maybe you already had a bit of surplus cash in savings tucked away somewhere. Maybe you can even sell some of your things and I’ve even published an article on how to sell your things online. Online classifieds like eBay, craigslist and gum tree are fantastic ways that can you not only get money to create a savings buffer but your also just getting rid of your crap and old junk. I cant believe it but people buy it – one mans trash is another mans treasure

You need a savings buffer, its going to be critical in dealing with lifes ups and downs, or the volatility and you should really aim for about $2000 before considering even spending on non essentials. One of the benefits of having a decent savings buffer like that is that you can really start to save on your insurance. That savings buffer actually forms a sort of self insurance policy or own insurance policy- an example is my auto car insurance. I had previously a fully comprehensive policy which is full insurance which means if there is any accident I am covered, regardless of who’s at fault. Now I thought that was a really good deal and it gave me peace of mine, but it was costing me over $1000 per year in premiums and oh by the way i f i do have an accident there is still a pretty sizeable excess of I think $1500. When i realised that actually my car probably doesn’t need comprehensive insurance and I transitioned to a third party only insurance or ‘the other person insurance’ which means if i have an accident and damage someone else’s car then there car is covered but mine isn’t. I saved a heap of money on my premium – I went from spending something like $1000-$2000 a year all the way down now I pay just under $200 and that gives me the peace of mind knowing IF i hit a Porsche or Lamborghini that its n ot gong to financially ruin m,e

and that’s what insurance should be – protection against something that is going to financially destroy you! that’s a rally important realisation on the path to FI because it allows you to free up a lot of cash flow that you would have normally spent on fear which essentially what insurance is. Remember insurance companies aren’t dumb. They are full of highly trained actuarians are very educated people, statisticians that basically work out the likelihood of your catastrophic event happening, how frequently will it happen, what is the likelihood of them having to payout and how can they adjust your premiums so that if they ever do get a payout that they still make a profit. In the long term, if you just kept that money in your pocket your actually going to come out on top. For some things the like say a home or real estate investment property I would have that insured because I don’t have the money sitting around to just buy another investment property or rebuild, when I can work the cost of insurance into the cash flow into the deal I always add it. I am insuring against something that will financially destroy me

Taking it back to the car example, because I was saving over $1000 a year in premiums by switching from comprehensive to third party insurance, I was able to take that money and put that into my savings buffer which meant if i did have an accident and my car is written off then I’ve got that cash to just go out and buy another car, whilst that third party policy would cover the other party. It is super important to have a savings buffer and emergencies happen – this might mean booking tickets to fly overseas or interstate for family, car accidents, specially if you have a family with kids or pets its essential you have a savings buffer and emergency fund. And that should be at least $2000 and then grow as appropriate to your circumstance.

Step 5 or the next step to FI is boosting your income and this is a great one you can have a lot of fun with it. Basically making more money from your job and start hustling. Create a side hustle or two or three or four! Be mindful of your time commitments though. Make more money, people generally get what their worth, and if you improve your self worth and self recognition and mindset and take that to your employer you may successfully negotiate a raise.

I did this with my job as a pilot – I actually had a pretty big case where I went to my supervisor through HR and said Nup I want more, this isn’t right, this what the award wage should be, this is what the company policy should be, and this is how much I am worth and deserve. It took a while and was a lot of effort but I can tell you it was 100% worth it. I actually got a raise of gosh it was over 30% (it was actually 43%) and it was a huge increase and not only did my salary go up they actually back-paid me which isn’t normal it often wouldn’t happen,. I actually got back-paid a chunk of money which went into my investments, and I actually recently got a settlement with my superannuation – my retirement accounts – through the company where that’s going to provide me some security for later on in life.

That helps me now too because really when you consider FI and FIRE, if you do choose to FIRE and retire in your thirties, that early retirement portfolio is going to support you from your 30s into your 60s, well when your 60 that’s when a conventional retirement would be planned so you still need to survive from 60 onward. so having those traditional retirement accounts whether that’s your 401k 403b IRA, Roth IRA or Aussie superannuation it is super important to have those and take the advantage of maxing out your contributions. That’s a very smart move and it will save you quite a bit on your tax as well. So step 5 – boost your income and don’t be afraid to negotiate – remember everything is up or negotiation! if anyone tells you otherwise they don’t know what they are talking about

Side hustles! so you are limited by your imagination. What are some side hustles that I did – we talked about eBay selling I got rid of junk and used that to fund a savings buffer/emergency fund, there’s nothing stopping you from buying something deliberately with the idea that you are then reselling it – called arbitrage and a lot of people do it. I’ve seen people loading up on toys at the supermarket because they know its a limited run. They are loading up and then well sell them for more online – just like ticket scalpers. They buy the tickets, wait for the price to go up and sell them. I’m not gong to argue about ethics if that’s right or wrong but that’s an option that’s available to you if you want to make more money

I know other people in the area that started dog walking businesses, walking dogs every morning. She was going to do that anyway, waling her own dog for her own health, but now she takes other dogs with her and gets paid like $20 per dog per week extra for a couple of walks per week – something she enjoys in her leisure time. Just think about anything that you have skills in or anything your good at or like which other people might want. For example if your good at graphic design then you could look at freelancing some design work – there are a heap of free or cheap tools for example Canva is pretty cheap which you can use for graphic design. You could get to work using outsourcing apps or websites such as Fiverr or Up-work where people will post tasks that they want done and you can bid for them.

IF your looking for more inspiration for ways to boost your income check out the site CaptainFI.com I’ve written a few articles on that and YouTube is also your friend -0 there are literally hundreds of thousands if not millions of videos on passive income and side hustles and how to make money. Literally just get at it, your limited by your imagination – figure out how to make some more money

The next step is to really pay off any debt. Step 6 is ditching liabilities. If you have debt other than say productive debt from a mortgage or home loan which is a good debt (working for you as long as you’ve appropriately cash flowed it). Remove any debt like credit card debt, personal loans, financing a car, payment plans those kind of things. That’s what you want to get rid of. When you pay off debt there are a couple of ways you can do it – two of the most popular methods of paying down debt are the snowball method and the debt avalanche method.

the snowball method its stars buy paying off your small debts first and then using the surplus cash flow that was going into that small debt to then tackle the next biggest one. That’s sometimes been referred to as domino your debt and using momentum. That’s super important from a psychological point of view because your seeing the benefits and seeing that extra cash flow which is basically less money coming out of your personal accounts.

The second way of paying off your debt is the debt avalanche technique this is probably more of an analytical one which is paying off the debt with the highest interest rate first, for example say you had a $200 interest free period on some furniture you bought which is interest free, and you have a credit card debt of $1000 being charged at 20% – the debt avalanche means you pay down the high interest rate credit card first and save the most money.

The debt avalanche is better in the long run but it doesn’t give you the warm and fuzzy sort of psychological feeling you accomplishment by domino your debt with the debt snowball. Either way, step 6 pay off any debt and get rid of liabilities – this doesn’t have to necessarily strictly be financial debt. if your driving a car that’s quite frankly ridiculous for your needs – if your driving a big 4WD around the city and its just you in the car and you never go off-road- then that’s a liability. Your much better off driving a small economical petrol powered car or even better cycling around. IF you have to drive, drive something sensible.

Step seven. Lets recap first. You’ve educated yourself, made a budget, cut your expenses, created a savings buffer of at least $2000, you’ve boosted your income and you’ve paid off your debt and got rid of liabilities. Now this is where the fun starts! This is where you get to start investing. Step seven is to start to invest your savings!

Start investing your capital to get rich slowly. Now this is the thing that really blew my mind when I discovered FI and investing – your telling me I can take my money and buy this thing, I can invest in this thing, and its just going to give me back money. So i started investing in exchange traded funds and ETFs, and four times a year I got dividends from Vanguard and from AFIC and they just threw off cash. Really it just changed my mind and I was hooked and I knew that this is real and this is something that can really improve my life. I actually went back to step one and did it all again, and I did it again and again trying to get more and more efficient and have more savings so that I could really throw as much as possibly into investing whilst I am younger and whilst I have time for compound interest to really work its magic.

where to get started investing? Well like we said in step one you need to read. Read everything. Immerse yourself in it. That’s something not everyone is prepared to do. Get started investing. Get started! Just get some skin in the game! Whether that’s just a small amount of money – I started with about $1000 which I put into the Australian Foundation Investment Company AFIC which is a funny story about how I Actually bought that. I was a bit silly, for some reason I thought it was like a concreting company, I thought foundation meant like they invest in concrete and pouring foundations and I actually bought the company thinking that that’s what it did (laughter) I laugh about it now but remember Warren Buffets golden rule is dont invest in something you dont understand

I learnt not to do that, refer to step one educate yourself but you’ve got to start somewhere. Don’t let analysis paralysis get you, just get some skin in the game. Weather that’s a small amount of money your prepared to lose and don’t need for the next 5-7 years, my advice is either look at AFIC, they are not a concreting company by way, they are a Listed investment company so they take your money and invest it in other productive businesses -we will talk about AFIC another time.

My recommendation is start small, get some skin in the game and once you get that first dividend I tell you you will be hooked. So investing, you don’t have to just invest in stock market ETFs you’ve got real estate, websites there is all sorts of things you can invest your money in. But like I said I’m not a financial adviser I’m not a professional, but where I have personally invested my money is a combination of those three things. If you do want to get started buying stocks, buying low cost index funds ETFs, of course your gonna need a broker. Don’t go off and spend money at a financial institution you can get an online discount broker really really easy its going to take 30-60 minutes online filling out some application forms you’ll need your ID and it might take a couple of says for the security background checks to get done, and then you can transfer some money into your brokerage account and you can be buying those index funds in your name as easy as that.

IF you are interested to get started or that’s the limiting step for you, jump onto CaptainFI.com there is a pretty comprehensive guide there about how to start investing in the stock market.

Of course the last step step 8 is managing your portfolio. You regularly have to add a bit more FUEL to the FIRE if you want to reach FIRE as per your investment strategy. Donkt forget periodically go back to step 1 and work your way down the list again looking for improvements each time. I’ve lost track the amount of times I’ve gone through this procedure in iterations and learned more and realised hey maybe I should look at something else like when I was trying to pick stocks and thought I cold beat the market, to now where I know if i invest in index funds that I AM the market where its so much easier so much less stress.

Educate yourself and work your way back down the list. I t might take you a few iterations to work out what kind of investor you are: what is your risk tolerance, how much effort are you prepared ti put into your investment, those kind of things you only found out through experience, So step 8 manage your portfolio -me personally I have a regular investment strategy where IF i have any money i just lump sum invest that into index funds straight away – you can read some papers I’ve got links on the site, lump sum is statistically the best way to grow your money. whenever you have money lump sum invest it

the flip side to that is dollar cost average or slowly drop feeding your money into the market. That’s a bit of risk avoidance measure, obviously your worried about say investing everything in the market and it drops ‘AHH I’ve lost all this money’! Maybe if your worried about that maybe you shouldn’t be investing – because smart investors know your investing for the long haul. If your investing for overnight gains you really have to understand that FI is not a get rich quick scheme, its boring, its a slow, game. It’s a marathon not a sprint. My strategy is if I get any windfall you know dividends, extra payout from work or I sell something, that goes straight into the brokerage account and ready for my fortnightly investment decision

That leads me to the next thing which is when I get my pay the first thing I do is pay myself first and take a chunk out and set it aside for investing. I regularly buy and am trying to buy $3000 of index funds each paycheck, it doesn’t always work out that way unfortunately sometimes life gets in the way. Recently I got whacked with pretty horrendous fine, and you know a few wedding so lots of expenses for gifts and travel but I want that and having my finances the way it is gives me the choice that you know that’s not an issue and it can be paid and I don’t have to resort to a credit card or borrowing money

That strategy when you think about it is a form of DCA, but it is also a form of LSI because your investing it as soon as you get it. That’s the best way to go. I’ve got links to Morningstar and Vanguard Research papers showing the statisticians work – they have done some pretty awesome work to show the numbers, over time with many different case studies they show why getting your money invested early is in your best interest.

When you look at managing your portfolio your gonna need some kind of tools to administrate. I’d recommend for Aussie shares you look at share-sight its a pretty awesome tools as long as you got less than 10 holdings its completely free. it does everything for me it generates my tax returns for my portfolio and there slinks to that on the website if your interested

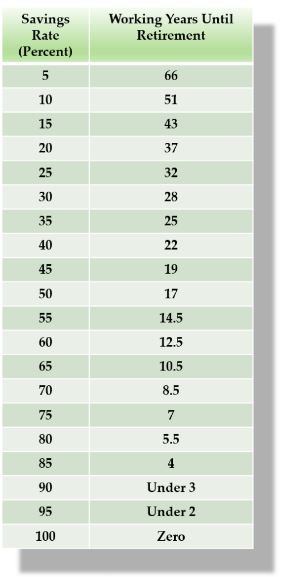

with those 8 steps you can pretty much set yourself up for FI, the next step is how long do you have to do it for. There is a pretty cool graphic on the website which kind of shows you just how much or just how long rather you need to invest and just how much you need to save to reach FI. For example the national savings rate across western societies, US, Canada, AUS and UK is actually under 10% so using the example of a savings rate of 10% it actually takes you over 50 years to retire. That’s pretty horrendous. normally people are tucking away money into their retirement accounts 401K IRA, superannuation which isn’t all that much but it usually boosts them to about a 20% savings rate which is still around 37 years of working until retirement. That’s your typical finish school, finish studying, get a job and work until your in your 60s, 65 years old and then you get your free time then when your old

That never really sat well with me it never made a lot of sense, why would I spend my whole life working for some else or someones business making someone else rich and then what have i got to show for it at the end? that never really stuck right by me so when I discovered FIRE and started reading Mr Money Mustache it really just changed the way i really thought about working, It made me feel a lot more happier that well there is actually people that share this kind of mindset. Having a look at the working years until retirement graph if you can save 100% of your wage then somehow your living for free and that means you can retire right now. But more realistically you know if you’ve got a 50% saving rate so your able to live on half your income, if you work for 17 years the growth of your investments and assets that you’ve bought with the other half of your income will provide you enough to retire safely at 4% which is pretty amazing

if you boost your savings rate even higher and your more mindful about spending you cut back on some of the excess and some of the things you don’t really need and you can start boosting that savings rate you can really get that years working number down. Personally I target 80% which equates to just under 6 years of working till retirement. Of course that’s just a fairly rough calculator lots of assumptions, and you might not want to live as frugally in your retirement as you are now as you are building up towards FIRE.

An alternative way of calculating this is to basically look at what is your goal or projected level of spending in retirement. You can work out a budget and how much you’ll spend per week and fortnight and then carry that out over the course of a year. Make sure to include the things you might not think about in your day to day spending so obviously food and accommodation and transport but you might also need to include additional health insurance as you get older that cost is going to increase. All those annual bills which you might not pay on a fortnightly basis your gonna have to really consider all of those. Thankfully when your on the path to FI your pretty aware of all these bills

Take your annual living costs and a really simple rough way of doing this is just multiply it by 25. That will give you your FI number! this is the amount of assets that you need invested for you to have hit FI. As a rough example if your annual living costs are $40,000 then you need $40K times 25 which is $1,000,000 invested in your portfolio. If you had a million dollars in diversified ultra low cost index fund, then you can live off the dividends and if you drew that down at a 4% safe withdrawal rate you would never run out of money for the rest of your life

This is 4% safe withdrawal rate or how we multiplied by 25, that’s based on an internationally recognised study called the trinity study which basically gives you a 95% chance that over a 30 year period your portfolio is going to survive all economic downturns and continue to provide you passive income during your retirement adjusted for inflation. Remember again you don’t have to be invested purely in stock market ETF there area huge number of smart people who have been able to reach FI using property and other investment strategies you really refer to that step one of educating yourself and coming up with a strategy and some goals and that’s going to be a huge step towards reaching FI

A big part of any FI strategy though is a large cash buffer. Whilst your working and building we recommended having at least a couple of grand in your emergency fund and over time boosting that to a reasonable level so some suggest 3 months worth of wages, some suggest 6 months worth of wages its a really personal choice you just have to figure out what is right for you Me personally I look at if i was to retire early I probably want to keep at least a years or maybe even two years worth of cash on hand. This buffer is just in case there was a market downturn so I didn’t have to sell my shares at a loss or crystallise selling them at a discount. Ideally if there is a downturn you just want to leave those stocks in there to recover over time, and also if there is a downturn that is a great opportunity for you t o be buying more. The reason i would keep such a large cash buffer is 1. As a bit of insurance for my cost of living and 2. If there is a downturn it enables me to move maybe half of it into buying at a significant discount some more ETFs.

The last tool or the last little feather in your cap as you strive towards FI is of course a tax leverage retirement account – your government retirements account which are FAN bloody TASTIC. everyone who is considering FI should really consider investing more of their cash into their retirement accounts. Of course Im talking about the american 401K and roth, Canadian IRA and Australian superannuation.

The rules they change from country to country so you really need to understand your scheme but the basic principle is that the government wants to encourage you to invest for your retirement. This means you are less reliant on the aged pension and social security. So they will give you a tax discount for investing for your retirement. Remember there are different schemes they are all slightly different some you pay less when you contribute, some you don’t pay when you withdraw some you do. Each has unique advantages and disadvantages and to be honest this could be the topic of hours of discussion but all I wanted to do is highlight they these schemes exist and you should figure out which one is appropriate for you.

Me personally I do something called salary sacrifice where I make a concessional contribution which is the maximum I can into my superannuation, In Australia that’s $15,000 per year that individuals can concessionally contribute into their super, and I have pretty much been doing that from day 1 which is why I have got an awesome super balance which will keep me sorted when I’m old. Of course i’ll need some kind of early retirement portfolio so i am splitting investing between super and traditional directly taxed investment accounts and real estate- but by contributing that $15,000 pre-tax contribution into my super I m actually only seeing a loss in my paycheck of something like $8000. ID have to get the exact numbers worked out for you but your saving on all that income tax. For a lot of Australians the average tax rate is 37 cents in the dollar you can check it out on google, but salary sacrificing is a great idea if you start early and contribute your cap you don’t see the money gone and it means a heap when it comes to your security in retirement.

so there it is guys, that’s Captain FI’s take on what is financial independence, why you should be working towards it and then how you can start working towards it with 8 pretty simple steps. I hope you guys took a lot out of it and if you have any feedback or questions for me let me know. In aviation the debrief is almost just as important as the flight we usually spend hours talking about what we have done and ways we can improve – so let me have it in the comments. Head over to CaptainFI.com you can leave comments there or email me through the contact form or head over to Facebook at the captain FI or Instagram as Captain_FI hit us up, send us a message or leave a comment and let me know what your thoughts are.

Thanks for listening to another episode of the Captain FI podcast. To read the transcript or check out the show notes, head over to www.CaptainFI.com for all the details

If you have a question for the Captain, make sure to get in touch. You might even make it on the airwaves. You can reach me online through the CaptainFI contact form or get in touch through the socials. I’m active on both Facebook and Instagram, as well as a number of online finance and investing forums.

Remember, The information on the show and the links provided are for general information only and should not be taken as constituting professional financial advice. You should always do your own research when making any financial decisions, and make sure its appropriate for your personal circumstances.

Music “Cheery Monday” and “Wallpaper” by Kevin MacLeod License: CC

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.