Not all debt is bad, so it’s important to know the difference between good debt and bad debt. Read on as we unpack how to use debt to get richer!

Introduction

I often hear that debt is bad, and actually, I spent most of my life desperately avoiding all forms of debt. I never wanted to borrow money, I just hated the skin-crawling feeling I got when I owed someone something. When I finished school and got a job, I drove a ten year old car because I didn’t want a car loan, and I wouldn’t even entertain the thought of a credit card.

When I discovered FI and the FIRE community, this reinforced that debt was bad. Reading the Barefoot Investor and Dave Ramsay’s Total Money makeover hammered the points of how bad debt is. Debt is like anti-investing or anti-dividends. It’s money you have to pay each week and get nothing for. Or is it?

There are actually two kinds of debt – Productive debt or Good debt, and Destructive debt or bad debt. Whilst desperately trying to avoid destructive debt, I also inadvertently made myself abstain from good or productive debt, like a mortgage.

Productive (good) debt

Good debt is debt that is used to buy an asset. A smart investor can use good debt to put more money into their pocket than it costs them. Essentially you use someone else’s money to buy an asset that produces an income or goes up in value. You need to be savvy, and a smart investor always looks at the cash flow on good debt.

A Mortgage

The best example I can think of is a mortgage or a business start-up loan. If you have a stable job, a good savings history, and a decent deposit you can approach a lender and apply for a loan to buy a house. The most common type of mortgage would be a principal plus interest for an owner-occupier loan for 80% of the property cost (80LVR) over a 25-year time frame.

If your mortgage payments and combined holding costs (insurance, utilities, council rates, etc) are less than what you were paying in rent – congrats, that debt is putting money back in your pocket every week!

Interest only loans

Even better, are a form of mortgage called interest-only loans1. These loans, as the name suggests, have interest repayments only, rather than a traditional home loan which is principal and interest (where you gradually pay down the value of the loan over the loan period). An interest-only loan is never paid off, and at the end of the term, you have to refinance or pay off the debt in total.

These are usually favoured by property investors that hold rental investment properties; because the interest payments are lower, you end up with a much better cash flow or positive gearing, putting money in your pocket from day one. A principal plus interest loan would mean you are gradually paying off the loan and generating equity in the property. Equity (or your percentage of ownership) is good, and you could even refinance down the track to pull out this equity for a future purchase deposit (called debt repurposing or a debt recycling strategy), but it’s not doing anything for you at the start.

Negative gearing a loan

Some people choose to negatively gear their properties,2 which means the cost of their loan and management costs are higher than the rent they receive. Usually, people are sacrificing cash flow today in the hopes of capital growth tomorrow. There are tax benefits to this strategy for those on top tiers of the income tax rate and has worked for thousands of property investors in a property boom. In a declining market negative gearing is just as dangerous as it is beneficial in a rising market. Personally, negative gearing is not for me, but you get the idea.

“While making a loss on an investment property or shares might initially seem counterintuitive, some people are willing to do this in the expectation that the capital gain (sale price minus cost of asset) when they sell the asset will more than offset that loss.”

treasury.gov.au/review/tax-white-paper/negative-gearing2

Starting a business

Other ways debt could be good for you is a small business loan – if you desperately need capital to launch your business then you could consider a small business loan from a lender such as a bank.

This could really accelerate your business allowing you to produce an income sooner. If you were an Uber driver, then a low-interest rate car loan could also be considered a form of business loan as you are then deriving an income from it. But these do have their risks, and you are locked into needing to make repayments which is a source of stress on a new business owner.

If you start a website business, there is very little financial outlay initially, which is why it appealed to me. You can read more about making money online HERE or you can read my review of the eBusiness Institute HERE which discusses making money through websites and online business.

Credit cards

Credit cards are not always a form of bad debt – spoofing credit cards for sign-up bonuses (called credit card or travel hacking3) can be a very lucrative source of free travel or cash bonuses, as well as using credit cards on everyday purchases for their cashback offers.

Destructive (bad) debt

Bad debt is debt that takes money out of your pocket. This is dumb debt. Debt that was used to buy liabilities, or was otherwise wasted. There are countless examples of bad debt being used in our society, but it essentially all boils down to living above your means. Credit cards, personal loans, payday loans, and car financing are all examples of bad (consumer) debt.

Credit cards with outstanding balances

Using credit cards to buy things you can’t afford is a seriously dangerous practice, which can harm your efforts to build wealth and lock you into a credit card debt cycle. The incredible interest rates charged on outstanding balances mean you pay a hefty premium if you can’t pay it off. To the tune of 20%! There are a number of other ‘synthetic’ credit cards or payment plans like Zip or Afterpay, where you can ‘Buy now – bleed later’, but I think it’s worth steering clear of these unless you have a tangible business case use for them.

“Your goal should be to pay off your credit card bills in full at the end of each month and set aside money toward your emergency savings.”

Suze Orman

No products found.

Personal car loans

Another bad example of debt that I see is personal auto loans. I look at the carpark at my airport and I usually look out to a sea of big 4WDs and other luxury cars. I wonder how many of these cars were purchased for cash, versus how many are on payment plans. All for a big car which from what I can see spends most of its time depreciating out in the weather (Sun and Hail).

The irony is that buying an expensive car using finance might make you look wealthy on the outside, but it’s a surefire way to keep you poor. Those expensive interest repayments are destroying your wealth, whilst the liability itself (the thing that the loan is secured against- the car), just continues to drop in value – on average by up to 20% per year over the first 5 years!

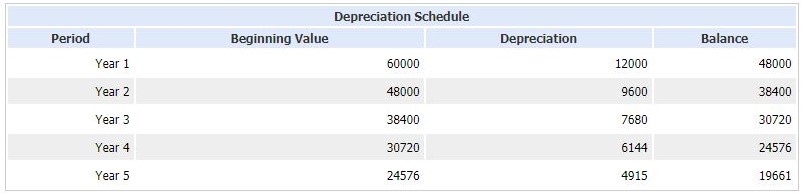

5 years is the most common car loan period, although people are increasingly taking out 6 and 7-year car loans to get lower monthly repayments or afford a higher loan amount (but costs them more in the long term).

If you purchase a $60,000 vehicle on a 6% finance over 5 years, you would end up paying 60 monthly repayments of $1160 (before any additional fees or charges) which adds up to almost $10,000 extra over the life of that loan! At the end of the period, you would be left with a car worth less than $20,000 – meaning you had spent $10,000 and lost $40,000 for a total loss of $50,000 over 5 years – $10,000 per year is VERY expensive motoring, and we haven’t even insured, maintained or put petrol in the thing yet! In contrast, I spend on average approx $3,000 on TOTAL vehicle costs for an entire year, with maybe $500 or so of depreciation (the car is currently 18 years old, I service it myself – and it drives like brand new!)

I’m not always against car loans, and there might be circumstances where using a 0% interest rate finance (or delayed payment plan) on a sensible ex-demonstrator (show vehicle) or second-hand small car might be a smart choice if you need a reliable vehicle for work. But you’re generally always going to get a cheaper option buying secondhand for cash, so there isn’t really any excuse to end up saddled with a loan.

Personal holiday loans

Ugh. If you can’t afford to pay for a holiday, you probably shouldn’t go. Maybe check out something cheaper – I love doing road trip holidays and camping or hanging out at the beach or river, which is nearly completely free (other than the cost of some fuel, beer, and food). Racking up thousands of dollars on a personal loan because you’re scared you won’t have another opportunity to go on a Contiki tour is not a sensible choice.

Pay day loans4

Payday loans are some of the shonkiest practices I have ever heard of. The sad thing is this kind of predatory lending takes advantage of some of the most vulnerable people in our society; statistics show the highest percentage of payday loan users are single mothers, struggling to make ends meet. Payday lenders gouge exorbitant fees and interest rates, and you want to stay as far away from this destructive debt as you can.

No products found.

Summary

In conclusion, debt isn’t always a bad thing and used effectively it can make you money. But having any form of debt does present you with a level of risk that needs to be managed – economic circumstances can change and you want to make sure you aren’t going to be left drowning in inefficient debt, unable to make your repayments.

MoneySmart.gov.au provides some useful info on managing debt, which you can check out here5. But I will leave you with something from one of the world’s greatest investors, Warren Buffet;

‘You don’t need to use debt to make money, and someone who doesn’t understand debt certainly has no place getting into it”

Warren Buffet, CEO Berkshire Hathaway

What you choose to invest in, and any loans you may choose to take are going to be individual decisions based on your personal financial situation but if you’re not sure what to do, it’s always best to speak to a financial adviser who can advise you as to the best course of action.

Do you have experience getting into debt to build wealth? Let us know your thoughts in the comments!

Reference List:

- ‘What is an interest-only loan and how do they work?’, Loans.com.au. Published (updated) on March 7, 2022. Accessed online at https://www.loans.com.au/home-loans/what-is-an-interest-only-loan on Nov 30, 2022.

- ‘What is negative gearing?’, Treasury.gov.au. Accessed online at https://treasury.gov.au/review/tax-white-paper/negative-gearing on Nov 30, 2022.

- ‘What is credit card hacking, and what are the risks?’, Rachel Rasker, ABC. Published: Sep 19, 2022. Accessed online at https://www.abc.net.au/everyday/credit-card-hacking-explained/101443606 on Nov 30, 2022.

- ‘What Is a Pay Day Loan? How It Works, How to Get One, and Legality’, Matt Ryan Webber, Investopedia. Published (updated): July 20, 2022. Accessed online at https://www.investopedia.com/terms/p/payday-loans.asp on Nov 30, 2022.

- ‘Get debt under control’, MoneySmart.gov.au. Accessed online at https://moneysmart.gov.au/managing-debt/get-debt-under-control on Nov 30, 2022.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.