UniSuper is an award-winning superannuation fund which is also one of Australia’s largest. Read this UniSuper review to consider if UniSuper delivers on low fees, strong returns and competitive insurance premiums.

The Good

- Award-winning fund

- Consistent low fees

- Consistent strong performer on returns

- Lowest cost MySuper option

- Competitive insurance premiums

- Positive online reviews

- Open to eligible Australian workers, although some products are only available to higher education workers

- Variety of investment options

- Industry fund, benefiting members

- Tools, calculators, podcasts, articles etc available on the website

The Bad

- Some products are not available to all members

- Concern the defined benefit option restricts returns

- Concern there may be a conflict of interest with employers playing such a large part in fund governance

- While UniSuper is a not-for-profit company, universities are largely government-funded, giving rise to at least a perception for the potential of governments being able to exert influence over the fund

- Some have questioned the sustainability of the fund1 in light of generous super schemes, staff layoffs and reduced hours

Verdict: With such low fees, positive reviews and awards won, UniSuper is a solid choice as a Super fund, but make sure you compare options.

Introduction

UniSuper is one of Australia’s largest super funds that also provides advice and insurance. UniSuper is an award-winning super fund2, named as Money Magazine’s 2022 Best Super Fund, Chant West’s 2022 Best Super Fund and Canstar’s Outstanding Value Award for Superannuation in 2023.

UniSuper’s default MySuper fund is also listed in the Top 10 performing funds3 in 2021 and 2022, as identified by the Australian Prudential Regulation Authority (APRA).

UniSuper is an Australian industry fund4 that was started in 2000 with the merger of 2 tertiary education super funds. Before 2000, UniSuper was the trustee for Superannuation Scheme for Australian Universities (SSAU). In 2000, when SSAU merged with the Tertiary Education Superannuation Scheme (TESS), the fund became known as UniSuper.

UniSuper is one of Australia’s largest super funds with more than $115 billion under management and over 620 000 members.

CaptainFI is not a Financial Advisor and the information below is factual review information, not financial advice. This website is reader-supported, which means we may be paid by advertising on the site, or when you visit links to partner or featured sites. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

What kind of super fund is UniSuper? Is it an industry super fund?

UniSuper is an industry super fund for employees of the research and higher education sector, such as universities. This means it is designed for profits to benefit its members, unlike retail funds where profits are also designed to benefit shareholders.

Is UniSuper a government fund?

UniSuper is not a government fund, rather it is an industry fund run by a not-for-profit company. That said, the Australian university sector is largely government funded, so the Australian state and federal governments are a large source of member contributions.

Is UniSuper an Australian company?

UniSuper is an Australian company. While UniSuper as it is now started in 2000 with the merger of 2 funds, UniSuper has been involved in superannuation for 40 years, as it was trustee for SSAU before the merger.

Who is UniSuper owned by?

UniSuper is an Australian company overseen by a corporate trustee named UniSuper Limited.

“UniSuper began with a single, compelling idea: we can deliver better value. We’re now one of Australia’s largest super funds, with more than 620,000 members and over $115 billion in funds under management.”

unisuper.com.au/about-us4

UniSuper has a shareholder employer group of 37 Australian universities which are all represented on a Consultative Committee5 by a 50/50 mix of employers, and employees such as general and academic staff. Amongst other things, the committee is responsible for nominating 4 directors to the board and approves and reviews changes to the trust deed. In the past there has been concern there is a conflict of interest6 in uni employers being so actively involved in the governance of the industry superfund.

UniSuper’s daily administration is managed by UniSuper Management Ltd, which is a wholly owned company.

What are the super options through UniSuper?

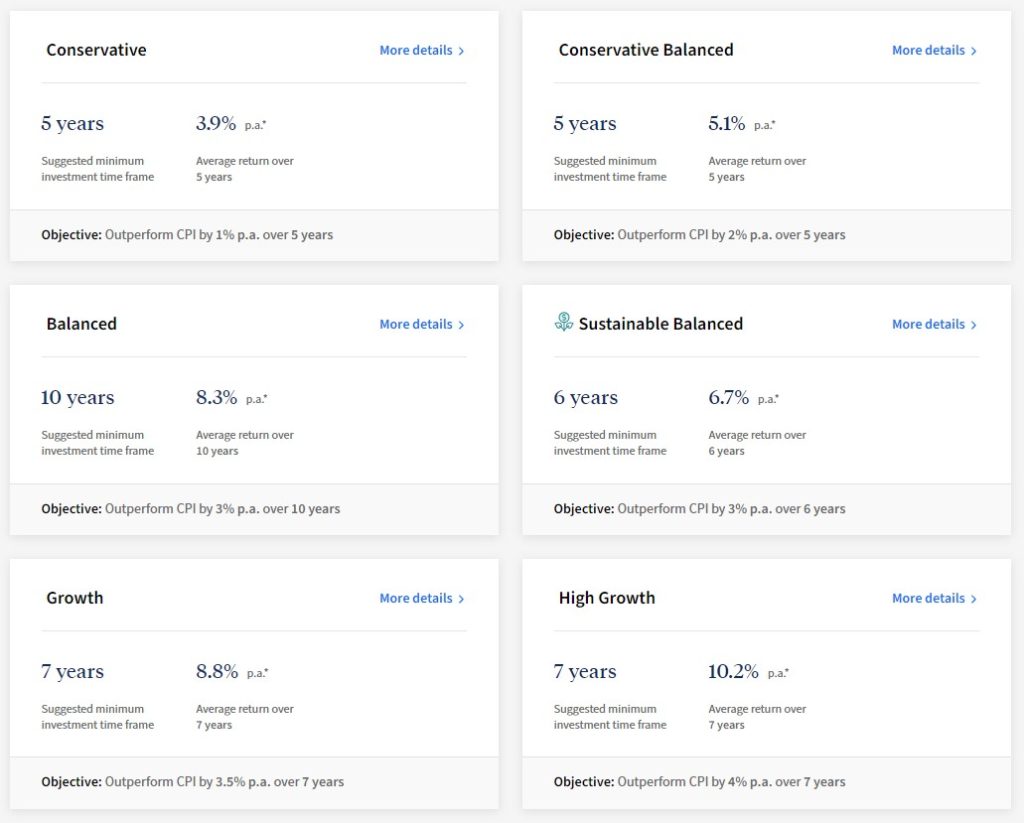

UniSuper offers a number of investment options7 as part of its super fund. The different options cater to members differing risk profiles. UniSuper offers the following pre-mixed investment options, each with a specific aim:

· Conservative – aims to outperform the Consumer Price Index (CPI) by 1 percent each year over 5 years

· Conservative Balanced – aims to outperform the CPI by 2 percent a year over 5 years

· Balanced – aims to outperform the CPI by 3 percent a year over 5 years

· Sustained Balanced – aims to outperform the CPI by 3 percent a year over 6 years

· Growth – aims to outperform the CPI by 3.5 percent over 7 years

· High Growth – aims to outperform the CPI by 4 percent over 7 years

· Sustainable High Growth – aims to outperform the CPI by 4 percent over 7 years

UniSuper has a number of other superannuation options, including:

· Defined benefit division (DBD) – intended to provide reliable growth so the member is reasonably sure how much they will retire on. There has been some criticism of this option in the past, that it limits the potential for member returns and puts too much burden on new members.

· Accumulation 1 – intended for those working in the uni sector and getting 10 percent super

· Accumulation 2 – intended for those in the DBD option for less than 2 years

What are UniSuper’s fees?

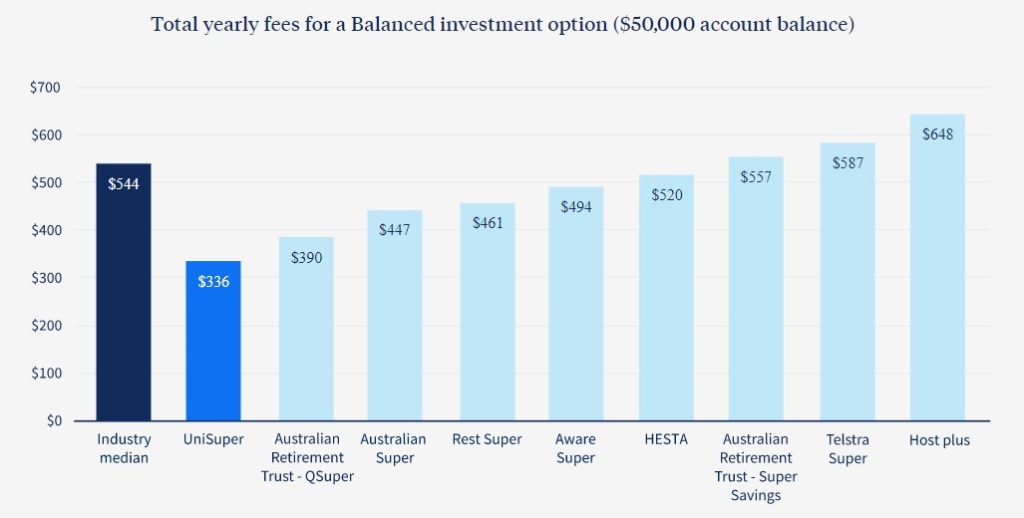

As with any super fund, UniSuper charges a number of fees8 in relation to investment and administration costs. The following UniSuper fee and costs are based on UniSuper’s MySuper balanced investment option, for ease of comparison.

· Administration costs and fees – $96 or 2 percent per year of your account balanced, whichever is less

· Investment costs and fees – 0.40 percent per year

· Transaction costs – 0.08 percent per year

So, for a MySuper balances of $50 000, each year you will be charged $96 admin fee, $200 investment costs and $40 transaction costs, for a total of $336 fees a year. In comparison, Hostplus Indexed Balanced fees are higher, making UniSuper a competitive option.

“Like most super funds we deduct investment fees and transactions costs, typically from investment earnings before they are added to your account balance. We’re able to keep this fee low because our expert in-house investment team manage a lot of our funds themselves, more than the average super fund.”

unisuper.com.au/super/products-and-fees8

How does UniSuper perform9?

UniSuper is one of Australia’s largest super funds and it has also won a number of awards such as Canstar’s Outstanding Value Award for Superannuation in 2023, Chant West’s 2022 Best Super Fund and Money Magazine’s 2022 Best Super Fund.

Using UniSuper’s MySuper balanced investment option to aid comparison, UniSuper has been a consistent high performer amongst Australian super funds. For the 10 years to December 2022, UniSuper has return 8.45 percent per year, compared to 8.22 percent per year against other industry super funds and 7.46 percent per year for the industry median overall.

Past performance is not a guaranteed indicator of future performance however.

UniSuper is has also been voted top for lowest super fees out of 92 funds by Chant West Super Fund Fee Survey for June 2022.

Check out UniSuper on Rate City HERE: UniSuper Performance Review | RateCity10

What are UniSuper insurance policies?

UniSuper offers the usual range of insurance products along with their super fund options. TAL is the provider of UniSuper insurance cover11. TAL is a large insurance provider and partners with a number of Australian super funds. Members can access the following insurance products12 through UniSuper:

· Death cover – UniSuper offers Death cover for those aged 75 or under. Your level of cover depends on your age and how much cover you choose. Death cover can be paid out if you die or have a terminal illness

· Total and Permanent Disablement (TPD) insurance – UniSuper provides TPD cover under the age of 70. Your age and how much cover you chose dictates how much cover you have. While there are eligibility criteria, TPD is paid out if you suffer a permanent disability and can’t work.

· Income protection insurance – For those under 65, UniSuper provides Income Protection (IP) cover. IP covers up to 85% of your income for a period of 2 or 5 years, with a waiting period of 30, 60 or 90 days.

The following example shows the cost of insurance premiums through UniSuper for a 30 year old male earning $100 000 per year in a white collar job.

· Death cover – approximately $115 per year for $500 000 cover

· TPD cover – around $155 per year for $500 000 cover

· IP cover – While UniSuper offers cover up to 85 percent of your income, other funds may only offer 75 percent. So to aid comparison, this example looks at 75 percent cover. For a waiting period of 30 days for 2 years cover – premium of around $150 per year, for 90 days for 5 years cover – premium of around $350 per year

How does UniSuper invest my super13?

UniSuper invests in the following sectors, in varying proportions:

· Australian and International shares

· Australian equity income

· Global environmental opportunities

· Global companies in Asia

· Listed property

· Australian bonds

· Diversified credit income

· Cash

Advantages of UniSuper

- Award-winning fund

- Consistent low fees

- Consistent strong performer on returns

- Lowest cost MySuper option

- Competitive insurance premiums

- Positive online reviews

- Open to eligible Australian workers, although some products are only available to higher education workers

- Variety of investment options

- Industry fund, benefiting members

- Tools, calculators, podcasts, articles etc available on the website

Disadvantages of UniSuper

- Some products are not available to all members

- Concern the defined benefit option restricts returns

- Concern there may be a conflict of interest with employers playing such a large part in fund governance

- While UniSuper is a not-for-profit company, universities are largely government-funded, giving rise to at least a perception for the potential of governments being able to exert influence over the fund

- Some have questioned the sustainability of the fund1 in light of generous super schemes, staff layoffs and reduced hours

FAQs about UniSuper:

When was UniSuper founded?

UniSuper as it’s known today was founded in 2000 with the merger of 2 tertiary education funds, SSAU and TESS. Before that, UniSuper was the trustee for SSAU.

Can anyone join UniSuper?

UniSuper is an industry super fund for the research and higher education sector, it is open to eligible Australian workers from other industries to join14. However, it’s important to keep in mind that some fund products are only available to those who work in high education.

You can join online through the UniSuper website, however, if you work for a member uni, then it’s best to signup direct through them. Signing up online is for those who don’t work for a member uni.

You can check out Canstar’s review of UniSuper HERE: UniSuper Superannuation – Review & Compare | Canstar15

Is UniSuper a good super fund?

All things considered, UniSuper comes across as a competitive fund. It consistently ranks in the top 10 funds, has low fees, competitive insurance premiums and strong returns.

UniSuper is also rated as 4 out of 5 for transparency, customer service, insurance options, income protection, rates and fees on Productreview.com.au16. On a forum where disgruntled reviewers traditionally come to air their grievances, the reviews seem overwhelmingly positive.

Conclusion

UniSuper is one of Australia’s biggest super funds with over 620 000 members and more than $155 billion under management. As well as super, the award winning fund also provides advice and insurance.

Despite UniSuper’s consistent performance, there has been some concern in the past with employer involvement in the fund’s governance, potential for government influence and the potential of investment options like the defined benefit option to limit member returns.

However, UniSuper is a fund that has been recognised for its consistent low fees, strong returns and competitive insurance cover. Overall, UniSuper’s MySuper default investment options has been a top performing fund for the past few years, making UniSuper worth considering for your super fund.

You can also take a look at my other Super reviews:

Australian Super Review – What You Need To Know

MLC Superannuation Review: How do they measure up?

Reference List:

- How the University revenue crisis will test its generous super system, Charlotte Grieve, SMH. Published: May 25, 2020. Accessed online at https://www.smh.com.au/business/banking-and-finance/how-the-university-revenue-crisis-will-test-its-generous-super-system-20200524-p54vus.html on May 3, 2023.

- We’re a multi award-winning fund, UniSuper. Accessed online at https://www.unisuper.com.au/about-us/who-we-are/awards-and-ratings on May 3, 2023.

- The 10 top super funds in APRA’s performance test, Michael Read, AFR. Published: Dec 17, 2021. Accessed online at https://www.afr.com/policy/tax-and-super/the-10-top-performing-super-funds-in-apra-s-performance-test-20211217-p59ie9 on May 3, 2023.

- https://www.unisuper.com.au/about-us/who-we-are

- Committees, Unisuper. Accessed online at https://www.unisuper.com.au/about-us/who-we-are/our-people/committees#Consultative%20committee on May 3, 2023.

- Our unis are stealing their staff’s futures, Daryl Dixon, The Canberra Times. Published: April 19, 2018. Accessed online at https://www.canberratimes.com.au/story/6160378/our-unis-are-stealing-their-staffs-futures/ on May 3, 2023.

- https://www.unisuper.com.au/investments/our-investment-options

- https://www.unisuper.com.au/super/products-and-fees

- Looking for an industry super fund?, Unisuper. Accessed online at https://www.unisuper.com.au/industry-super-fund#:~:text=APRA’s%20data%20shows%20that%20the,First%20Super%2C%20Hostplus%20and%20UniSuper on May 3, 2023.

- UniSuper superannuation, rate City. Accessed online at https://www.ratecity.com.au/superannuation/uni-super on May 3, 2023.

- https://insurancecalculators.tal.com.au/unisuper

- https://www.unisuper.com.au/insurance/types-of-insurance-cover

- https://www.unisuper.com.au/investments/our-investment-options

- https://www.unisuper.com.au/campaigns/join-us#:~:text=Now%20anyone%20can%20join%20the,be%20age%2015%20or%20over

- UniSuper superannuation, Canstar. Accessed online at https://www.canstar.com.au/providers/unisuper-superannuation/ on May 3, 2023.

- UniSuper, Product Review. Accessed online at https://www.productreview.com.au/listings/unisuper on May 3, 2023.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.