From the costs of dating to pregnancy-related costs, giving birth, raising a baby, then a toddler, a preschooler, and all the costs involved in raising a school-aged child, through to adulthood, there’s a lot to consider when it comes to family financial planning. So what is the real cost of raising children?

Introduction

“It takes a village to raise a child”

My Dad, June 28th 2022.

It is a widely held belief that the cost of raising a young family is incredibly high. I have heard people throw all manner of figures out there, with the most ridiculous being a cool Million dollars per child. This is just plain ridiculous, and I hope to dispel some of these common myths as I learn more about the real cost of raising children.

This article is the culmination of some in-depth research that is basically written for myself; that is, a cisgender Australian male who is capable of having children, who is on the path to Financial Independence, and who wants to start a family in the very near future.

There are an incredible number of variations on these themes for all the different strokes of folks out there – including fostering, adoption, IVF, surrogacy and many other ways of starting a family.

This article is also pretty broad, starting from step one of actually meeting a partner and following right through to the logical conclusion of kicking your baby birds out of the nest. It is not designed to ‘tell you what to do’, shame parents or virtue signal, rather it is my way of researching and budgeting what I will spend on raising my kids, and roughly how I am planning to do it, for your information and peer review so that this can evolve over time.

The idea is also really to end the thought experiment at age 17, or when my children graduate secondary schooling. Whether they stay at home to complete their tertiary education or move out on a scholarship (like I did) I guess doesn’t really matter as they aren’t really children any more – they are now adult children and ideally should have some form of employment by this time. I like to think I would be happy to support my adult children through their tertiary or vocational educations, but expect them to contribute to the household in some way. In any way, this is a long way in the future.

The Cost of raising children is not well defined

Having kids means your household cost of living will go up. However, just like other aspects of modern life, the amount you spend on raising children is a choice. In the same way people tend to lifestyle inflate when they get a raise at work, many parents with good intentions are duped into spending incessantly on their children.

This is partly due to very clever marketing that guilts parents into spending, and also the highly unethical marketing that is aimed directly at the children themselves. If you don’t believe me, check out any of the advertising seen during morning television ‘soft-news-o-tainment’ or children’s programming.

Budgeting to raise a child – government child cost index

“The new government budget standards found the estimated weekly costs for low-paid families to raise two children (a six-year-old girl and a 10-year-old boy) is $340 a week, or $170 per child. At the lower, unemployed standard, the costs of raising two children was $280 a week, or $140 per child“

Data from the University of New South Wales’ social policy unit suggested that the average Australian household spends somewhere between $100,000 and $300,000 for every child they raise to the age of 17. The approximate total costs were around $100,000 for families on welfare, $150,000 for “low-paid” families and the upper limit was for “average” families.

Ironically, ‘failure to launch’ is quite prevalent in modern society and it’s becoming increasingly normal for adult children to stay at home until well into their 20’s and even their 30’s, costing parents much more – perhaps a symptom of housing affordability?

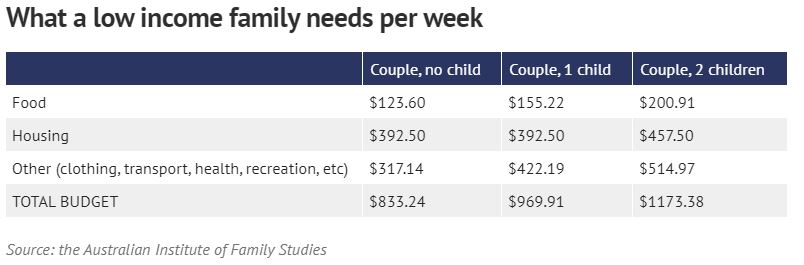

Low income family costs example

Take even this metric from the Sydney Morning Heralds article on child rearing – they suggest that a childless couple need $833.24 per week to survive. That is over $43,000 a year, and if we assume they managed to save the Australian average of $5000 per year, and that it was earned with a single income, that equates to a (before tax) salary of $61,000 and a savings rate of 10% (plus whatever they contribute to their super).

This doesn’t account for the tax savings you can leverage as a couple (such as investing in the lower earning spouse’s name, or contributing to the lower earning spouse’s superannuation etc), or any unemployment or family benefits.

Whilst this couple would be earning well below the national average of around $84,000, they are still comfortably above the National defined ‘Poverty line’ of $42,000 income – this is defined as 50% of the national average income. By my understanding, this ‘low-income’ couple could live pretty well, even having one ‘future parent’ at home.

FIRE family budgeting versus conventional family budgeting

My FIRE number is less than half their ‘low income’ figure at $380 per week, and does not necessitate dumpster diving or welfare to live an amazing, luxurious life. A good chunk of that is a saving of $142 per week on rent ($250 vs $392), $73.60 on food ($50 vs $123.6) and $237 in the ‘other’ expenses ($80 vs $317). What ‘other’ expenses could you possibly have that total up to well over half of your rent? I can think of one – Childcare!

Although probably not the best comparison, subtracting my FIRE number of $380 per week to the ‘low income couple – 2 children’ figure of $1173 per week, suggests that children in this case are somehow costing this family an additional $793 per week, or $350,000 each to raise to 17!

This is clearly at odds with the previous estimates, and I think it illustrates that the specific costs associated with raising children are not well defined. I suspect that the cost of raising children ultimately scales according to your income and level of lifestyle inflation, just like every other cost in modern society.

Summary of cost to raise a child

The point of this article is to pique your interest in the costs of raising a family, and to point out that available costing and budget estimates for the specific costs associated with raising children is not well defined. Rather than a numerical value, I suspect that the costs of raising children are on a sliding spectrum.

This could mean that the cost of raising children might be similar to our normal cost of living – meaning there is an ultimate ‘frugal’ baseline, but that due to lifestyle inflation, most people are flagrantly living at many many multiples above and beyond this baseline.

Throughout this article, I plan to unpack and explore this relationship, as I learn about and plan for my own future family. Please chime in with your own experience and knowledge to help me, and other readers, along the way!

The Cost of Courtship

I do not plan to raise a family on my own. Hell No! There are so many tasks and things to be done, honestly I don’t know how single parents do it! They are the superheroes of our society. I know because I was raised by a single Mum, and the sacrifices she made were incredible.

Currently, I am in a stable, committed relationship, and we have started having these kinds of conversations, especially as we both want a big family, but before this turned into a serious relationship, there was the cost of dating.

The Cost of finding a partner

For me, there was no having children without a partner. Most relationships start with an introduction or chance meeting, and progress naturally through dating, exclusivity, a relationship and finally into a marriage or civil union prior to having children. Although seemingly more often than not, ‘life’ happens and it doesn’t necessarily go in this order!

The Cost of dating

Dating can be really fun. It can feel a bit overwhelming at times, especially when it doesn’t work out, and it can sometimes be risky – but as we all know, high risk = high reward.

I am a bit of a risk taker, so tended to roll the dice with blind dates and meeting new girls. Oh how horrendously this has worked out for me in the past. I can’t even begin to describe some of the awkwardness I have encountered in my dating life – both from them and from me.

I have also met a heap of amazing girls though, some of whom I will be friends with for the rest of my life. Actually, some of my best ‘girl-mates’ came from friendships that naturally evolved from dating. Talk about the friend-zone haha!

Budgeting for dates

It might sound a bit tight, but I usually tried to budget no more than $100 for a date, and I think it’s a bit callous to go on more than one per week (with a different girl, that is). $100 gets you a pretty awesome date though, and the following ideas are a list of things I keep in the back of my head for dates, in a bit of a natural progression:

- Catch up at a local cafe for a coffee and a chat, or a take-away coffee and a stroll through a park or a bush-walk: $10

- Take-away Yum-cha or dumplings in the park or at the beach: $30

- Take them out for a ride on my motorcycle… IF I HAD ONE! Unfortunately, I sold my bike because it didn’t align with my spending and lifestyle goals on the path to Financial Independence.

- Catch up for Gelati and a stroll through the nightlife: $20

- Picnic in the park: I go all out and would choose an assortment of fruits, snacks, cheese and wines: $50

- Take-off for a quick fly in a light aircraft – a couple laps of the field (called ‘circuits’) or to check out some local scenery: $100+

- Head out for a nice meal for dinner, Italian is one of my favourites. If you’re being very cost conscious just order the entree: $75-100

It is my belief that the guy should always pay for the first date. The woman is obliged to ‘pretend’ to pay and a little ‘back and forth’ should ensue where both parties offer to pay, culminating in the guy paying and getting to feel ‘like a man’.

What happens after the first date?

If the first date was a roaring success, then another should come a suitable time interval later. I would say at least 3 days later, but maybe the following week with an appropriate level of flirty texting and maybe a phone call or two in between. The second and third dates I think should be more equal, with the woman offering to pay, or at least contribute half.

How many dates should you go on before becoming exclusive? Well don’t hate me, but I think you get ‘three for free!’

That means you should be able to see and date whomever you want, whenever you want, until the third date. After the third date, it’s pretty clear that you are both interested in pursuing each other, otherwise why would you have bothered with the second or the third? I think that’s a logical amount of time and level of commitment to make it worth the effort of going exclusive.

Before three dates you don’t really know each other anyway, and it’s probably around this time that you are getting physical. You have all heard the old adage “Don’t …. on the first date” right, and I think it’s best to get to know each other and build up trust before you take a relationship to the next level.

Just watch the nomenclature here, especially if you’re not savvy in the dating game. Just because you are exclusive doesn’t mean you’re in a ‘committed relationship’ – it just means you are exclusively dating each other, and not ‘seeing’ anyone else. Even if you don’t ‘like putting labels on a relationship’ it is likely the other person will, and subconsciously you both need to provide small levels of commitment to each other for the relationship to grow.

Total: $100 per week or about ~$5K a year.

Love languages

Something that will help you immensely during the ‘dating game’ is understanding your love languages. Put quickly, your love languages are how you express your feelings. The most common description of the love languages are the following five (ranked in the order of mine!)

- Physical touch – love and affection through touching, cuddling, sex.

- Quality time – spending time together with no set purpose.

- Acts of Service – doing nice things for each other, i.e. cooking.

- Words of Affirmation – saying reassuring things eg “I love you”.

- Gifts – sacrificing money to buy thoughtful presents.

The Cost of Relationships

Once you transition from dating into a relationship, things all tend to settle down a bit. Lust stabilizes into the more meaningful love connection, and everything tends to calm down. Sometimes this is called ‘transitioning out of the honeymoon period’.

This is when you really start to get to know someone, learn all about them and fall more and more in love with them. Belts get tighter, nights get quieter and suddenly it is more acceptable to spend a night snuggling on the couch with a movie rather than heading out to a nightclub! (Personally, I would take this trade any day of the week!)

Your costs go down

I think that relationships cost less than dating, as it’s more about living your life together and doing things you both enjoy, rather than spending money on activities to try and impress one another. Actually, as you settle into a long-term relationship, you will likely find that instead of costing you money, it actually makes you money.

Sure, there are some small costs involved, especially when you want to spoil or buy gifts for your significant other, but the cost savings you can benefit from potentially living together and benefiting from the economy of scale and working together far outweigh any of these factors!

The cost of a relationship is stress if you aren’t on the same page financially

By far the biggest determining factor of how much a relationship is going to cost you, is whether you are both on the same page financially2. Sometimes a relationship can be classified as having a ‘spender’ and a ‘saver’, and it can be frustrating if you find yourself in the latter category. If this happens, just have an honest conversation and be upfront with your partner.

After all, money isn’t everything, but if you can agree on some common goals it’s going to make your lives much easier and less stressful. Some ways I have seen to help combine finances is to both keep a separate account each for spending money that can be used, no questions asked. Some good friends of mine use this system, and for anything over $500 they just ask each other to see if it’s worthwhile and aligns with their spending goals and financial goals.

However, there is no rule saying you need to combine your finances at all, and I know heaps of people who have families and still keep separate accounts. Often, they share a joint account and choose to contribute their share each which covers joint expenses.

Other costs of relationships – complacency

I have found though that one of the biggest costs of a relationship is not money, but actually your level of effort and enthusiasm for life. As everything tends to calm down, I certainly find this happens to me. I put in less effort at work, in the gym, and with my studies. This is a natural effect of the drop in the level of testosterone that happens when men enter stable, committed relationships.

The cost of break-ups

A bit of an unexpected cost of a relationship is when it goes south. Unfortunately, I have had a few pretty shitty breakups during my adult life, and they were not fun to go through. Once in 2013, another at the start of 2020, and another in 2022. These took a heavy toll on my mental health, as heartbreak always does.

As is tradition, I spent a lot of money, ate a lot of junk food and balled my eyes out afterwards. I also then rushed out into ‘rebound’ relationships and got physical far too quickly, seeking comfort and attention. As you can predict, these collapsed quickly and hurt everyone involved.

I bet you would have never thought I would make the connection between the cost of heartbreak and the cost of raising children, hey? I think it’s a valid point, and it’s all part of the journey to becoming an awesome Dad!

A more serious note to consider though when it comes to the cost of break ups, is if you are living together, considered defacto or have already had children, then you are a combined household. This means if you do choose to separate, that the combined household net work gets chopped in half, and you both walk away with half – potentially one with a commitment to regular child support payments. This can be an extremely tough time for both parties, and forced sales of assets always results in lower prices and more stress. This can be very financially destructive.

The Cost of Marriage

I will start this with, I believe Marriage is a pretty antiquated notion. Marriage equality is a pretty important topic for a lot of people out there, including myself, but personally, I don’t see any rush to get ‘married’ at all. At least, not in the public spectacle fashion that society has conditioned us all to want and waste on.

At its core, to me, Marriage is about making a life-long commitment to your partner, nothing more – nothing less. It’s a wonder then, why the average Australian spends over $60,000 on funding their wedding. Traditionally, this is covered by the father of the Bride – but I can tell you this much – if I have a daughter, I’m bloody well not dropping $60K on fancy Hors d’oeuvres and napkins for one day!

Consider this – instead of spending $60K, if the average newlyweds went on down to their local council / courthouse to get their marriage certificate, then spent an excessive $4,000 on hosting a massive, extravagant celebration at home, and then even went on an amazing $5,000 month-long honeymoon, then they still would have saved themselves over $50,000!

Invested into ultra low cost total stock market index ETFs, this $50K would reliably provide them with $2,000 per year of passive income, according to the 4% rule. This would never run out, and would fund an awesome 14 day holiday to Bali every year for their anniversary! Which one would you prefer? Some nice memories and photographs, or a lifetime of ‘free’ annual holidays to celebrate and relax together? $50K could also be a nice deposit on an investment property or family home!

Again, it’s not totally going to be my decision. Although I am happy with a civil union at the local court house, it’s likely my partner will not be. Either way, I am setting aside $10,000 for a ripper party and holiday, and my future father-in-law can cough up if he wants anything fancier than that!

Total: My budget is $10,000.

Summary – the cost of dating

I came out with a sum of $135/wk using my ‘frugal’ FIRE figures. Who knows how long you’re going to be doing that for, but I do know that even once you start a stable relationship, the costs don’t stop – they just turn into bigger (joint) expenses like moving costs, vacation costs, little gifts just because and then of course… potentially the cost of your very own home and setting up a nursery 😉

Ultimately, don’t get too strung out about the costs though. It can be a real ‘turn-off’ if you’re a bit savage about it all, or constantly calculating things. One of my ex’s complained that she hated my continual re-calculating of the car’s gas mileage during road trips (something that was just fun for me to work out) so it’s worth noting that what might be normal behaviour to you could be considered obsessive to another.

I will tell you though, from a bloke’s perspective, girls are attracted to a man that is financially secure. It’s not about money or gold digging or any of that, it’s about maturity; someone who is sorted financially ticks a massive box in terms of being able to securely provide for a family. Ultimately that is the biological drive behind dating isn’t it – the ‘raw primal instinct’ is just about survival and replication? Attachment theory is a really interesting aspect of psychology you can delve into to understand why we seek security and stability in our relationships. I wouldn’t go bragging about your ETF portfolio though to try and score a date, just be quietly confident and keep it to yourself.

The Cost of Pregnancy

The first stage of raising a child starts with the pregnancy. Well, I guess it starts with something much more fun, but it leads to pregnancy. Pregnancy might not be something you think of as being expensive, but it can be incredibly expensive and taxing for some parents.

Tips for planning your pregnancy

- Decide on Public or Private healthcare well in advance!

- Explore whether your job has a paid maternity or paternity leave policy

- Explore the Government paid Maternity and Paternity leave benefits and qualifications, as well as family tax benefits – if you worked at least 330 hours in the previous working year you should be eligible for up to 18 weeks of paid parental leave (split between Mum and Dad).

- Review your life insurance and income protection policies – these are likely tied up inside your superannuation

- Ensure you have updated your will, and consider establishing a testamentary or discretionary trust in the will.

- Nominate a trusted friend or family member as an enduring power of attorney for your affairs

- Create a family budget to work out just how much you need to spend on baby items, including both one-off and additional ongoing costs.

- Practice living on your new budget and set aside any surplus into your emergency fund or sinking fund for one-off items

- Consult your GP and get a referral to a fertility specialist for screening. If you need to explore the costs of IVF to successfully fall pregnant, these can be incredibly high and you should be prepared.

- All private health insurers and health funds have a 12 month waiting period for childbirth

- Your child may not be covered on your health insurance policy from birth in case they require hospital care immediately – check your policy

- Reproductive services like IVF may not be covered on your private health insurance policy

- In Australia, register for the medicare safety net. This means once you have paid a certain threshold of out of pocket medical expenses, you will receive a higher level of rebates from Medicare.

The cost of IVF treatments

Consider that for 1 in 8 parents, IVF is the only way to successfully fall pregnant. IVF treatments can cost upwards of $10,000 per cycle (3 week duration per cycle), and leave you $5,000 out of pocket for your first calendar year cycle after the Medicare rebate, and then you’ll have to cover the full cost of additional treatments yourself.

Studies show that on average, each cycle gives you a 20% chance of pregnancy and that 3 full cycles can provide a 40-50% chance of pregnancy. Although the stats here are a bit fuzzy and I am struggling to remember my engineering statistics math lessons.

I thought addition of probabilities was P(a or b) = P(a) + P(b) – P(a)*P(b), so the IVF scenario might look something like P(pregnant) = .2 + .2 + .2 – (.2*.2) – (.2*.2) – (.2*.2*.2) = 51.2%. 6 cycles of IVF comes out to something like 90%, however it’s important to realise this is based on a 20% chance of success each cycle, but this might actually not even be physically possible for all parents due to infertility. Canstar has a great article on IVF3.

Travel costs of pregnancy

If you live rurally, like some 7 million Australians, you might not have immediate access to healthcare. This could mean additional travel costs to your local regional center or capital city associated with pregnancy and childbirth. It’s likely driving is your only option, which can cost anywhere between 90c to $3 per kilometre depending on how frugal your driving habits are.

Opportunity cost of pregancy; lost income

Furthermore, it is usually not practical for a pregnant woman to work for most of her pregnancy. As a wanna-be daddy, I want to work hard now to make sure my partner doesn’t have to work, unless she wants to of course. When you consider the lost income and productivity over a 6 month period on the median salary, this cost can be well over $42,000 (without even calculating in the pickles and the ice-cream)!

The cost of miscarriage

Now, I want to bring up a taboo topic. Miscarriage. The stark fact is that statistics show one in four pregnancies result in a tragic miscarriage. Many go unreported due to the stigma and shame women feel. I would suggest the number is much higher than one in four. And no one talks about it.

During one of my past relationships, an accidental (and unknown) pregnancy led to a miscarriage which was absolutely heartbreaking. We didn’t know until it resulted in excessive bleeding and a trip to the emergency room. It was at 10 weeks.

At the time it was confusing and I didn’t know what to feel, but in hindsight, I am incredibly saddened and heartbroken for the loss of this amazing opportunity. Miscarriage often causes relationship issues, which it did for us. She doesn’t talk to me anymore – probably because it reminds her of what happened.

The cost of miscarriage on your mental and physical health is significant. Apart from the obvious emotional trauma, it can be extremely risky to a woman’s health, and financially devastating4 for some. Whilst miscarriage is more likely early on in a pregnancy, the later it happens the riskier it is to the mother’s health.

Because of this, many women die due to excessive bleeding and infections due to miscarriage every year. To further complicate this traumatic event, many hospitals or doctors will only operate in very specific situations due to religious or political beliefs (anti-abortion or pro-life considerations which I do not want to get into at all).

As a result, miscarriage can often be incredibly risky, and the result of this is significant healthcare costs5. This can be as high as $20,000. Even with private health insurance or Medicare in Australia, the average out of pocket expenses associated with a miscarriage can add up to well over $2,000.

Cost of maternity wear

There are also a lot of seemingly minor expenses which add up for pregnant women, such as clothing. Maternity wear is needed since a woman’s body changes shape remarkably. On the list might include Maternity jeans (or sometimes called stretchy jeggings), Maternity or Breastfeeding bras, leggings, wrap dresses, comfy tops and flat shoes – which can add up to thousands of dollars depending on your budget.

Miscellaneous costs of pregnancy

Other than clothes, miscellaneous costs can include things like specialist massages, physiotherapy, yoga sessions, pregnancy vitamins and birthing classes which can range from $50 to $100 per session and easily add up to over $1000 during the course of a pregnancy.

Summary of the costs of pregnancy

Whilst pregnancy doesn’t seem expensive, there are actually a heap of hidden costs. This is at least $1500 in direct costs for a natural pregnancy, increasing to over $55,000 to successfully fall pregnant under IVF (90% confidence), as well as over $40,000 in opportunity costs due to lost income.

The cost of Birth

The act of giving birth or having your child delivered can have some significant costs if you are not adequately prepared. Whilst not an authoritative source, I have done some research into the common costs of Public births under Medicare and compared them to what you might pay as a Private patient through your private health insurance.

“I am never gonna financially recover from this”

The Tiger King.

Choosing between Public vs Private healthcare when having a baby

You can choose between public and private healthcare options when having your child. In Australia, it is worth noting that we have world-class public healthcare through the Medicare system, which covers the majority of Australian births.

For healthcare expenses, the Medicare safety net kicks in when you spend a certain amount on health expenses within a calendar year – including Private patient expenses. This will mean you potentially get a higher amount back from your Medicare rebate, and this helps protect families from the high costs of birth complications.

Public healthcare when having a baby

Public healthcare in Australia is covered under the Medicare system. You will have minimal out of pocket expenses, however, there will likely be no continuity of care, you won’t get a choice of midwife or obstetrician, and you are more likely to have a shared room and shorter hospital stay.

Realistically, a public birth seems to be the sensible choice, with the only typical out-of-pocket costs being ultrasound imaging, pathology tests if done outside the hospital and medicines (Medicare offers a rebate for most). On average, these out-of-pocket expenses are under $15006. Most public hospitals have great reputations and offer a world-class level of health care, with good levels of comfort and post natal care. As such, almost 75% of all births in Australia take place in a public hospital.

However, you are at the whim of the public health system; at peak times (think Friday and Saturday evenings) the hospital can be overwhelmed with other emergencies which might divert resources. Similarly, if there is a sudden influx of births, there might not be enough resources for everyone to get an ideal level of care. Whilst the hospital will of course look after your health and safety, you might not get the level of extra help you could really need whilst you are in this incredibly vulnerable and sensitive situation.

What Childbirth costs are covered by Medicare?

As a Medicare card holder in the public system, healthcare costs during your pregnancy and birth are mostly covered by Medicare with little to no gap fees or out of pocket expenses. However, depending on your choice of care and where you give birth, Medicare may not cover all, and instead only subsidize a portion of your costs (i.e. if you want a private hospital or at-home birth).

The following information is adapted from the Medicare Schedule7 (comes directly from Medicare PDS), and describes what is covered during pregnancy and childbirth;

During your pregnancy

- Free (or partially covered) care from midwives and obstetricians in public hospitals, outpatient clinics, community clinics, birthing centers or publically funded home birthing programs

- Free or partially subsidised care from a private obstetrician, eligible midwife or doctor in a ‘shared care’ arrangement

- Subsidised tests and imaging such as ultrasounds

During the birth of your baby

- Free (or partially covered) care from midwives and obstetricians in public hospitals, outpatient clinics, community clinics, birthing centers or publicly funded home birthing programs

- Partially subsidised care from a private obstetrician, eligible midwife or doctor in a private hospital

After the birth of your baby

- Free (or partially covered) care from midwives and obstetricians in public hospitals, outpatient clinics, community clinics, birthing centers or publicly funded home birthing programs

- Free (or partially covered) home care from midwives during the week after being discharged from a public hospital, public birth centre or publicly funded homebirth program

- Free or subsidised care from private obstetricians in hospital during recovery, and check-ups several weeks after birth

- Free or subsidised visits or appointments with eligible private midwives

- Free or subsidised care from GPs and obstetricians after you are discharged from hospital

For your newborn baby

- Free or subsidised care from an eligible private midwife

- Free or subsidised care with a private pediatrician (child specialist)

- Free (or partially covered) maternal, child and family health services from midwives and nurses

What is not covered by Medicare

- Hospital admittance as a private patient in any hospital

- Gap fees or copays for private obstetricians, eligible private midwives or your own private doctor caring for you during pregnancy or after

- Fees associated with private midwifery during labour and birth at home that are not covered through a registered public homebirth program.

- Out of pocket private hospital expenses, such as medicines

Private healthcare when having a baby

Private healthcare however can be expensive, but you get continuity of care, your choice of hospital, midwife and obstetrician, and you can get a private room and potentially extend your hospital stay if you wish.

Out of pocket costs for a private birth

As an example, the following expenses are typical costs of a private birth;

| Description | Cost |

| Practice Fee | $1400 |

| Excess or deductible (this will depend on your policy) | $500-2000 |

| Obstetrician appointments x 10 | $50 per |

| Scans / ultrasound imaging x 4 | $295 per |

| Anesthetist | $700-1000 |

| Pediatrician appointments x 2 | $200 per |

| Total (minimum) | $6,000 (approx) |

However, I will say that I have not had personal experience with this, but I have been told that this is likely to be on the lower end of the cost of a private birth, with no complications.

It is common for births under private healthcare to still cost parents around $10,000 in out of pocket expenses with significant gap fees which aren’t very transparent or clear at the time. Called ‘Post baby bill shock’, bills will just randomly turn up in the mail, even months after the birth.

It is difficult to obtain information relating to fees and charges online or prior to the birth, but you are entitled to obtain ‘informed financial consent’ by directly asking your healthcare provider.

“The ABC called 40 obstetricians, across all capital cities and some regional areas, and found huge variances in the cost of giving birth through the private system. For the obstetrician’s fees alone: the cheapest price we found was $2,145 in Hobart and the most expensive was $8,500 in Sydney. When you add up the costs of scans, and a complicated birth requiring extra medical attention, out-of-pocket expenses can reach up to $20,000.”

Gap-fees after Private health insurance claim rebates

After private health insurance rebates, the average cost of having a child is around $2000-$3000. But you will still have to front the out of pocket expense and submit a health insurance claim to get your money back, sans the co-pay (or gap).

Every pregnancy and birth is unique, and depending on your policy and level of private health cover, some complications can end up costing tens of thousands more. Without private health insurance, the costs of these services at a private hospital could be far in excess of $30,000!

Summary of the cost of Birth

So what’s my bottom line? I am almost entirely convinced to go with the public health system for the birth of my children. They are better experienced because they handle the majority of births, they have ‘unlimited’ government resources and better equipped in case of any complications, and ultimately it is a fraction of the price of Private treatment.

In terms of purely the costs, I am budgeting $2000 out of pocket for each public health system birth. This is because despite Births in a public hospital being ‘free’, there are still some hidden costs that Medicare doesn’t cover and I don’t want to get caught out – on average, this is below $1500, and I have applied a safety buffer. On average, private births cost double this, as well as the expensive ongoing premiums you pay.

The cost of The Early Years

Now that you actually have a baby, let’s have a look at some of the individual costs of raising a child and see what we can come up with. This section will focus on the early years, from newborn to age 5.

The early years of your child’s life can be very expensive, as there’s a fair amount of stuff that you do need. And because of how fast children grow, they can outgrow clothes and other equipment like booster seats and prams frustratingly quickly. Some of the major expenses in this age group include equipment like prams, bottles and car-seats, as well as nappies, formula and, of course, child care (daycare).

Opening thoughts on lifestyle costs

In our adult lives, we can pretty much spend almost as much as we want to on our cost of living. It’s called lifestyle inflation and usually, as we earn more, we spend more. This is the vicious ‘paycheck to paycheck’ cycle that keeps the majority of the population poor and forces them to be wage slaves.

Take a ridiculously ‘high’ standard of living and indulgence in fancy restaurants, food, holidays and add to that personal debt like unpaid credit cards, a car loan, student loans, a mortgage and you begin to see what I am talking about.

In a similar manner, parents can pretty much choose just how much they want to spend on their children. If you must have brand new luxury or designer equipment, clothing and accessories for you and your children, then of course child-rearing is going to be ridiculously expensive.

The cost of raising children

Some detailed estimates put the average ‘essential’ cost of raising children in Australia as high as $350,000 each, with a further $300,000 in opportunity costs due to lost income, productivity and earning potential.

However, just like when it comes to personal finance and your ‘pre-baby’ life, if you consciously make use of the second-hand economy and bring your essentials back to the bare necessities, you are likely to come out much further ahead financially than the average parents. You will also live better than 99% of parents around the world due to your Aussie privilege providing things like Medicare, clean tap water and reliable electricity.

By the way, here comes my first estimate: $7 extra in household electricity consumption per week, per child, or $364 per annum.

Sleeping arrangements

Some parents like to have a designated nursery in an extra spare room for their child, but some parents simply opt to have the cot in their bedroom, especially for the first few months.

This can be hands-down one of the most expensive things about having children. It’s pretty reasonable, I think, to afford each child their own room, but in my family, we shared rooms as young kids and it was fine. When we became teenagers we got the luxury of our own rooms when we moved to a bigger house. Individualised posters on the walls was epic!

Depending on where you live, a bigger house can be very costly. In Sydney, for example, an extra bedroom usually makes an apartment cost another $50-100K, and for a house this can be $100K+, translating to approximately an extra $50-100 per week in rent. In the country or outer suburbs though, it doesn’t seem to make as significant of a difference than it does in the city – maybe around half to two thirds of the cost.

Total: Average $60 per week per room – two kids to a room was fine for our family (under 12) – $3000 per year.

Equipment

One-off and replacement equipment costs add up. Because I don’t really ever buy anything new, I have scouted the costs for these on second-hand forums like Gumtree and Facebook Marketplace.

- Pram: $400

- Cot and (new) bedding: $300

- Baby bag: $50+$200 contents

- Cradle / baby car pod: $300

- Change table: $50

- Bottles, express pumps and steriliser: $300

- Baby food jars or pouches and blender: $200

- Toys: $200

Total: $2000+ once off, then $200 per year maintenance/replacement

Vehicles

Depending on your working situation, financial situation and where you live, it’s either going to be essential or probably just a sensible and practical idea to have a vehicle. This means in an emergency you have a way to get to the hospital or urgent medical care. It is also going to make everyday life a lot easier, although is not a necessity and there are many billions of parents worldwide who raise their children without a car.

For all you hardcore FIRE people, you might have to give up your ‘low income single dad8‘ style cars! Driving a beat-up or small car is fine, as long as it is mechanically serviceable and safe to drive. However, odds are that your sub-$2000 price point Barina or Yaris isn’t going to win you any awards with your significant other if they are struggling to fit baby equipment like prams in and out of them.

Going out and buying a brand new Kia Carnival 8-seater is going to set you back somewhere between $40,000 to $70,000 depending on the level of add-ons you choose. Even a decent second-hand one is still around $5,000 to $10,000. Whilst it is a bit of overkill for the first child, this might be a realistic option for larger families.

On the top of concerns for most parents is always the number of seats, size / space for a pram, and safety rating. Personally I am going for a second-hand Kia Carnival (but might settle for a Toyota Tarago) because I want a lot of kids and modularity to move seats in and out, but your standard 5-seater station wagon makes a great choice and has plenty of room. If you’re not already driving one, $5,000 is more than enough for a modern wagon with oodles of room.

Total: Should be no more than $5000, and I don’t think you can even call this an isolated baby expense…

Clothing and shoes

Babies and young children grow pretty quick, so these expenses can add up.

If you want to buy new clothes, baby and toddler clothes can be bought new as cheap as $10 ‘per set’ in places like Target and K-mart, but you can spend $100s per outfit on designer stuff. It’s likely you’ll need new clothes every few months or so, a cost which can add up to around $500 per year.

If you’re not fussy, you can pick up bags of free hand-me-downs from family or friends, as well as buy cost effective second hand bundles from other mothers or op shops. I’ve seen bundles of 20+ ‘sets’ of clothing for under $10 on Gumtree and Marketplace. Most parents can’t seem to give them away, and end up donating them to goodwill.

Shoes are another annoying cost, which I constantly hear about from the dozens of friends of mine with children. On average they are paying about $30 for a new pair every 3 months, depending on how quickly the kids trash them. These get progressively more expensive as the kids get bigger, and if you opt for higher quality shoes that last longer, they’re commensurately more expensive. On average, it’s about $120 a year.

P.S. I would get smacked with the wooden spoon if I wrecked my new sneakers, and instead often wore a pair of leather Blundstone boots as they were much harder wearing and lasted longer (they’re now also super fashionable and expensive!).

Total: Between $120 and $620 a year.

Baby food and formula

There is a lot of stigma and shame around breastfeeding mums, which is just ridiculous. Breastfeeding is a natural and beautiful thing, and should be encouraged freely without shame or staring. There is also a societal shame for mothers who can’t breastfeed, which is just as bullshit! Not every mum is going to be able to breastfeed, and this isn’t a reflection on how good of a mum they are.

For mums who can’t breastfeed or express milk, formula is really the only option. The cost of formula really depends on your baby’s appetite and how much you use it to supplement breastfeeding, but parents can spend up to $2,000 per year9 when feeding exclusively on formula.

Ideally, you would breastfeed as long as possible, but this just isn’t an option for many people. Breastfeeding is basically free, and provides a number of health benefits for both mother and child – weight loss and lower risk of breast cancer for mum, weight gain for bub and bonding between the two are just a few!

Pediatricians recommend solely breastfeeding for the first 6 months, and then slowly introducing small amounts of other food into a baby’s diet, including formula supplements and some ‘solid’ foods after then.

Baby food is expensive if store bought in small jars or pouches. I’ve seen these on the shelves for around $1.50-$2.00 each! These can be made at home with all-natural ingredients using equipment you likely already have in your kitchen (pots, pans and blenders). Keep it simple and smooth, with a variety of pureed fruits and vegetables. I have many friends who fill up their own jars or pouches to take on outings, since kids seem to need to be fed small amounts frequently. My niece chomps her way through about 5 a day!

As they grow, most babies become capable of increasingly solid foods as they teeth between 6-12 months of age. Providing teething aids like hard biscuits help your babe through this time, as well as just basically giving them small amounts of what you yourself are eating. There are certain foods that should be avoided however, like unpasteurised milk or honey.

The World Health Organization10 recommends breastfeeding for at least two years, but it is very common in parts of the world for mums to breastfeed up to age 4 or 5, for health and bonding reasons. Ultimately, mothers should do what their instincts tell them to do, and not worry about other people’s opinions or expectations.

Total: Breastfeeding is nearly free, but even a frugal parent would expect to spend at least $500 to $1000 per year on additional baby specific food such as supplemental formula and ingredients specifically bought for making baby food. For purely formula and store bought baby food, this could be as high as $2000 to $4000 per year.

Total: $500-$4000 per year.

Feeding a toddler and growing child

Once your child has transitioned to a solid diet and gets bigger, their calorific needs increase. Estimates for 2 year olds are up to 1500 calories per day, and a five year old is up to 2000 calories. For reference, a grown man usually needs 3000 and I consume around 4000 because of my active lifestyle.

Based off the calorific assumption alone, I would generalise that a child would then eat much less than half as much as I do. I budget for around $50 for groceries per week, which usually works out to around 35,000 calories of whole-food, plant-based foods (and luckily I am able to grow $20 worth of these so I only spend around $30). Ignoring the benefits of scale, and assuming the child’s diet is identical to mine, this would cost $25 per week if I bought it all.

Having said that, I realise that there are a number of extra things people tend to only buy for their fussy children. When I have children I also plan to have access to a large garden (i.e. moving out of my current small place), so my ability to grow food will increase. I am betting that this increased food production will offset the increase in expenditure, and keep the food costs at around $25 per child, per week.

Total: $1300 per year.

Nappies

Nappies are a big expense11, especially disposable nappies. On average, these are 30c each and in the first year alone a newborn can get through 5 or 6 per day! This slowly tapers down as the child gets older, so overall you can expect to pay around $40 per month or more in disposable nappies for a total of approx. $500 per year.

It isn’t for everyone, but if you choose to use reusable nappies (and have a good washing machine) then FuzziBunz cloth diapers brand new are about $20 each. I’d hazard a guess you’d probably need at least ten (or more), and then a variety of increasing sizes for as your child grows. If you budgeted $600 for 30 brand new FuzziBunz cloth diapers, it would probably get you out of trouble for ages 0-3.

I have also seen second-hand ‘sets’ (which can be washed and sterilised!) for under $200. Obviously reusable is better for the environment and generally better for sensitive baby bums and legs, but it’s not possible for every parent and this article is not about virtue signalling – parenting is hard enough as it is!

However it’s not just the one-off cost of buying the reusable diapers, you’re still going to need to clean and wash them on a very hot cycle, probably every day (along with a bunch of other stuff). A load of washing sets you back 50c according to the Australian Tax Office, so expect to budget about another $200 per year for this increased water, electricity and soap usage.

Around 2 to 3 years old is when most parents begin toilet training their kids, but it’s normal for this to be a long process over many months with plenty of accidents along the way. Most children are generally potty trained by the age of 3 to 4, but it can take months or even years to properly night train your child. This might mean investing in ‘pull-ups’ or other big boy and girl nappies until the ages of 5-6. Pull-ups aren’t as expensive as nappies, and can be reused after a dry night, with an estimated cost of $20 per month.

Total: somewhere between $1300 to $2000 per child from ages 0-6, depending if you choose disposable or reusable nappies.

During your child’s formative years, especially under 4, education and socialising are super important. These are the years when your baby’s brain is in overdrive, and it is establishing its core neural pathways and learning behaviors.

Whilst you won’t exactly be forking out for a private school education just yet, you will still want to focus on educational toys and activities for your child.

As your child progresses from a toddler onward, their needs for social stimulation outside of the family unit increase. Before then, it’s very difficult as they haven’t really developed enough yet. Socialising is important as it gives kids a chance to:

- Practice their own speech – start, continue and finish a conversation

- Make sense of other people’s body language and other non-verbal communication

- Negotiate and solve problems when they don’t get what they want

- Understand hidden social rules and cultural norms

- Manage group dynamics and fit in with other kids

- Recognise the effect of their actions on others

- Develop empathy and see things from another person’s point of view

- Begin to understand and regulate their own emotions

- Be flexible and use lateral thinking to solve problems

- Work together in a team

Social groups and junior sport

Early education and childcare centres are a great way for this to occur in a community or social type situation, so many parents opt to send their child in at least one day per week (this also gives mum and dad a break!). We will explore the specific costs of childcare and preschool later.

Great ways to help your kids develop their social skills are play groups with other local parents, where they learn to play and work together with other children. Sometimes these are community run, or sometimes they could just be family, friends or local parenting groups you find online such as on Facebook groups.

Many of these are free, but might set you back a nice cup of coffee or so. These are also valuable support and social networks for parents, too, where you get to have a chat and unload, and of course discuss your kids to figure out all the weird stuff that is going on is actually pretty ‘normal’.

Some parents enroll their kids in ‘Pee-Wee’ junior sport as young as 4 which I think is a great opportunity for risky play, socialising and teamwork. But having said that I’m not quite sold on pushing activities on children too hard while they are too young. Registration can start at $200 per year to join teams or clubs, however ‘elite’ programs can cost as much as thousands per year!

I had a few friends that were ‘forced’ (encouraged) to play things like tennis, music, gymnastics and dance classes very young and they weren’t allowed to quit. Sometimes I went along with them, because my mum was awesome and she let me float about and sometimes join in on things. Allegedly one time I cried until I was allowed to do ballet with my sisters, but after a while lost interest.

Educational Toys

Educational and complex toys are great to help stimulate your child’s imagination and develop their creativity. These might include puzzles, building blogs, Duplo (large lego), train sets or doll houses. Parents and children are both aggressively (and unethically) marketed to for these toys, which can cost hundreds of dollars per unit, and end up costing you thousands per year if you indulge.

I had a number of people get in touch to let me know they use toy libraries or ‘toy banks’. There are a number of free toy libraries associated with your local council library, and commercial toy libraries can be subscribed to for under $150 per year. Both of these allow parents to sign out toys similar to books from a library, usually around 5 toys for up to 2-4 weeks at a time.

These are awesome and not only save you the costs of buying new age appropriate and educational toys as your child develops, but you can also donate your old toys to them and it prevents them ending up in landfill (of course, dangerous, broken or crappy ones still end up in the trash). The variety of different toys and different stimulation is great, and if your child simply won’t part with a toy you can always buy it outright from them or replace it with something similar.

Risky play

I am a massive advocate of ‘real-life’ or ‘risky’ play, where kids get to explore and learn by climbing trees, playgrounds, playing in dirt, skin their knees and hammer nails into wooden blocks and get splinters. They learn real life risk management skills such as ‘maybe I shouldn’t climb this if I can’t get down’ and ‘gee that hurt when I landed on my face’. This education also happens to be nearly free! With five teachers in my family, including one early childhood development teacher with over 40 years’ experience teaching, this is something we all agree on.

This might also mean getting your young kids involved in helping with digging, weeding, composting, mulching and planting your vegetable garden and not plonking them in front of a screen. Realistically, they won’t actually be much help, but it’s quality time you are spending together and setting a great example.

Teaching kids to grow plants is super important, and helps them connect with nature and understand their place in the world, as well as develop their motor skills (hand-eye coordination), empathy, attention to detail, self discipline and patience. All valuable skills to set them up for a good financial future.

Animals and pets

I was super lucky to spend a good portion of my childhood in the country and the bush. Not only did I get a lot of ‘risky play’ but I also got a lot of great exposure to animals.

Psychologically, animals and pets can help children develop empathy, deal with anxiety, develop responsibility and understand the bigger picture. It used to melt my heart to see my 1 year old niece picking grass to hand through the fence to help feed the ‘tik tiks’ (chickens). She also had no qualms picking them up, and the chooks were well handled; she and they were both calm and gentle. She loves her daily job of checking the eggs for Nanny, and carries her precious egg bounty very proudly into the kitchen.

At the age of 2, she probably didn’t understand fully when the cat died, but she did place a tissue up to her aunty’s face and say “All better now, not sad”. Her language is incredible and I am amazed every time I visit at just how much she has grown and developed. Nonetheless, dealing with the circle of life and understanding death and grief is a valuable outcome of having animals.

Physically, having animals is also very beneficial. The exposure to dander, dirt, hair and other micro organisms like bacteria that they introduce to the house are actually really good for your kids immune system, and help to prevent allergies. This is another reason why I like ‘outdoor’ playing.

Animals and pets can be expensive though (read my post about the real cost of dog ownership). So this is more of a bonus if you grow up on a property or farm, but can be expensive in suburbia or in an apartment. Estimates of dog ownership are $3000 initially, and then $1500 per year thereafter – and ours were no exception (costing $10,000 on one occasion for surgery).

I also like cats, although they are jerks. Estimates are $500 initially, and then a further $500 per year – but please keep them indoors. Smaller animals like guinea pigs, rabbits, mice, frogs or hermit crabs can be more affordable and still provide benefit, but could still cost you hundreds per year in feed and other costs.

Screen time

Although screen time is super useful when you need a break, specialist advice is ZERO screen time under 2, and then a maximum of 1 hour a day until school age when they are using it for educational purposes (i.e. iPads and laptops at school).

I don’t purport to understand how hard this is as I am not a dad yet, and this isn’t about virtue signalling or shaming parents. My nieces and nephews LOVE the screen and beg me to play PlayStation, or watch Wiggles or shark videos on YouTube with them. Even when I visit my friends with younger children (below 2), they are incredibly curious about my iPhone and will often sneakily take it (even right out of my pocket!) and find somewhere quiet to hide as they try swiping or tapping to make it do something.

Summary

It’s super hard to put a cost on these education and socialising costs, and childcare and school costs are explored further below. As a stab, I would guess it is at least $20 a week, or around a thousand dollars per year (excluding child care) split between planned and ad-hoc expenses. If you choose to introduce a family pet like a dog or a cat to help your child, this is a fantastic idea but has upfront costs and will cost thousands more per year.

Total: $1000 – $2500+ per year (if introducing pets).

Childcare

Childcare or daycare, is a large expense new parents might have, and can be a massive financial burden on a family. From conversations with friends I have found that between the ages of 1-5, people spend an average of $70,000 on ‘full time’ daycare per child, or approximately $300 per week for a standard school term, after government rebates.

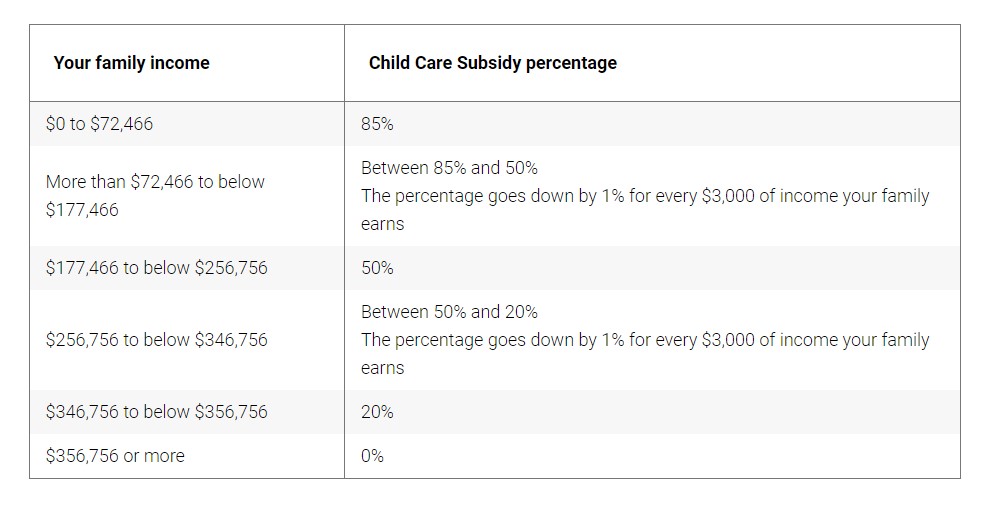

If both parents are working, this is usually an unavoidable expense. Help from family and friends can only go so far, and even with one parent staying at home, sometimes they will just need a break. Costs for one day a week still average around $60, although there is a sliding scale of child care subsidy rates depending on how much your family earns.

This means high-income families will effectively pay more for their child’s daycare – at the national median family income of $195K you will be paying half, and above $356,756 you are expected to pay the full balance.

NB. This figure comes from the Australian Bureau of Statistics13, which in 2022 determined the Australian median income to be $1,875 per week ($195K annual gross family income), and the standard family household to consist of two working parents.

So what is the actual cost then? Around Australia, the full cost is estimated at around $120 per day, per child. This number is also rising faster than inflation, at a cost of around 10% per annum! This varies depending on the centre and location; in rural areas you might expect the ‘sticker’ price to be $100 per day, however in inner Sydney this could be in excess of $200 per day.

When I spoke to the director of an outer Sydney suburb childcare centre, I was quoted $128 per day for a 0-3 year old, and $114 per day for 3-5 year old (before government subsidies). However the fees in Sydney varied significantly, and when I rang a centre in the city, their fees were incredibly nearly double!

Another consideration is the level of service the centre provides. Most of the higher cost centres are considered ‘full-service’, that is, they will cover expenses like nappies, baby wipes and food for your child. Check your enrollment PDS, because some of the more affordable centres may require you to bring some of your own supplies for your child, indirectly raising the cost (which also is frustratingly then not included in the subsidy).

There are other alternatives to daycare such as paid nannies, however these costs are significantly higher (estimated $500 per day and above) as they do not benefit from the economy of scale experienced with a family or centre-based childcare. Child care centres have minimum staffing requirements but usually employ one worker for every ten children (for ages 3-5). For quite large families with closely spaced children though, in-home childcare and nannies might be a cost-effective alternative.

Finally, if you are financially independent and have specifically chosen not to work so you can raise your children, this is something that doesn’t need to stress you out. It’s likely your combined family income will be well below the $67K gross income meaning you would get the full 85% subsidy, and with the rebate, one day of childcare a week would likely cost under $40 per week. Just be aware some rebates are attached to minimum employment hours too, so a full FIRE lifestyle might not get the full rebate.

Summary: This expense is far too broad to generalise, but the average Australian can expect to pay somewhere north of $60 per day for childcare, after the subsidy rebate. High-income earners can expect to pay more like $100, and those in capital cities like inner Sydney might pay $200 per day.

Total: $2000 for one day a week on low income, with an average of $14,500 per year for 48 weeks of full time enrollment, up to a maximum of $48,000 for high-income earners in capital cities.

Medical costs and health insurance

Oh boy. First up, if you are wondering about the difference between public Medicare and private health insurance have a read of this article.

Family private healthcare plans can be expensive, and in Australia private healthcare isn’t strictly necessary since we have an amazing universal healthcare system called Medicare. However, for high-income earners or high-net worth individuals who are happy to pay for the convenience of speedier healthcare and increased privacy, it can be well worth the cost.

The average (single) Australian pays a total of $3000 per year for combined hospital, generals (extras) and ambulance cover. The average ‘nuclear’ family with 2.5 kids can expect to pay significantly more; an average ‘standard’ level of private healthcare insurance costs around $15,000 per year, with a ‘gold’ standard low-deductible policy at nearly double that.

Medical costs for the first five years of year child’s life are highly variable and depend heavily on the child and any potential health issues. Unfortunately some disabilities can be incredibly expensive and not all are supported fully by Medicare and the PBS. You really need to spend a good amount of time researching what is available, understanding the level of risk, the level of ‘customer service’ you are happy with, and what you could afford or are happy to pay. Remove fear and marketing from the equation, and focus on the facts.

Total: $0 – $30,000 per year.

Summary of the cost of the early years

The early years of childhood sure can be expensive. Especially if you want brand new stuff, and if both parents work and you need to use daycare or childcare. Furthermore, the skyrocketing increases in the cost of private health insurance for young families place new parents under more financial pressure.

The cost of the School years

This is a big one isn’t it. The cost of schooling directly stems from your choice to send your child to a public vs a private school. Other than school costs, you also have to consider the increasing costs of food, sports, hobbies or other extra-curricular activities and things like allowances.

There are extensive debates about which is better and I don’t pretend to fully understand your experience, situation or rationale in deciding what you think is best for your child’s education.

The cost of schooling

I will say however that not only I, but all of my siblings, and all of my cousins were raised through the public schooling system. I was a right prat of a child and got expelled from a number of them (My Tally needs both hands and feet to properly count them all!), but my other brothers and sisters did not.

Among this latest generation of the family are four qualified PhDs, four Post Graduates (Masters level), Two full time academics, a retired Pilot (me!), an Aerospace Engineer (I also did this for a while too!), a Land weapons systems Engineer, two teachers and a Medical student. Not bad for a free public education hey? I am actually seen as the ‘dumb’ one of the family because all I did was fly a $100 million dollar aircraft!

School fees

Estimates for average school costs from kindy (preschool) to year 12 vary wildly between the different types of schooling within the education system, and can range from;

- Public school: $6500 to $50,000 (depending on your income and where you live).

- Catholic School: $240,000

- Private School: $500,000 (Average $180 per day!)

Public government schooling is allegedly free, however all of the surveys and data I have found online has shown the average total cost to be closer to $50,000 in fees and charges over the 13 years of schooling. Low-income families however can qualify for certain rebates and welfare which covers this, and my Mum paid approximately $500 per year for me and my siblings primary and secondary school fees

Total: From $500 (welfare) to $4000 (public) to $40,000 (private) per year

Books, technology and equipment

This can include many unexpected expenses when it comes to family finances. School stuff is expensive, especially if your child is required to have technology such as iPads or Laptops. This is more common in Religious or Private schools, where you might expect to fork out $2000 every year or two for tablets and laptops.

For public schools however, my costs were a lot more reasonable at around $200 per year. In my secondary schooling years, I also qualified for Aus-Study youth allowance, which covered these costs and allowed me to buy a laptop.

Total: $200-$1000+ per year

Uniform fees

Another killer for snooty private schools are the ridiculous and expensive uniforms, blazers and boater hats that can run into the thousands. I mean, do you WANT your child to be bullied?

I wore a crisp uniform when flying, but that was as a grown man and a professional – if they are anything like I was, I doubt my children would be able to maintain theirs without getting muddy or crumpled. I had a hard enough time with a white shirt (and still do to this day). Also, having to get changed for phys ed? That sounds like a lot of extra work and I don’t like the sound of my future kids getting undressed at school.

I went to public schools and we wore neat, comfy blue or black pants and a white or yellow polo or cotton shirt with the school emblem. Some of the girls wore blue pleated skirts or checkered dresses, and we all had to wear a broad brim sun hat (No hat = No play). It was suitable for the classroom, walking to and from school, and all out warfare on the footy pitch at recess and lunch.

Total: $100 (public) – $500+ (private) per year.

Excursion and other extra in-curriculum activity costs

These really depend on the school and again, vary significantly between public, religious and private schools. Speaking from experience, my Mum used to cough up at least an extra $200 a year to cover these additional costs.

These included school movie nights, ‘school sleepover nights’, trips to zoos, museums and galleries and once to the formula one races – this was a high school physics experiment to time them around the corners, then later weigh them with pit crews to calculate tyre friction coefficients!

Total: $200+ per year.

Out of School hours Care14 – OSHC or OOSH care

OSHC or OOSH care are state regulated before and after school programs which help working parents, especially single parents. This enables you to drop your child at school earlier, and pick them up later. Usual hours might be from 7:00 to 8:30 am when school starts, and when school finishes at 3:30pm to 6:00pm when you can pick them up. Sometimes it runs during pupil free days or on school holidays, and even during school holidays which is usually called vacation care.

OOSH care usually has a variety of entertaining and fun activities for your child, and I can remember just playing sport with other kids as well as watching cartoons when I used to go. I went to many different schools so participated in a bunch of different OOSH programs, and one even had a ‘Breakfast Club’ where you got to eat brekky for free – I always opted to make pancakes!

The costs for OOSH care vary from state to state, and also between schools. The average costs range between $20 and $40 per session, but when I attended it was free because my Mum was able to access this as a single parent low income benefit.

Total: $0 – $19,200 per year (depending on income and welfare benefits – my Mum paid $0).

The cost of extra-curricular activities

Extracurricular activities for school age children can quickly add up to be quite costly if you are pushing your child to undertake every activity under the sun!

Specialist advice from child developmental psychologists, however, is to not push your children into taking on multiple commitments too soon, but rather to encourage them to stick with one or two hobbies or sports that they themselves enjoy.

Overloading your child’s schedule can put a lot of pressure and stress on your child, which they are not old enough to properly deal with. This will likely result in rebellion and undermine your relationship.

As a child I switched between playing school footy, karate lessons and swimming depending on the season, and I also was a member of the Scouts and the Army Cadets at one stage. All up, Mum reckons this cost her about $200 per year.

Sporting club memberships can start to get very expensive, with my local team junior footy membership costing $400 per year. This can ramp up quickly with age grades, and ‘elite’ level sporting clubs and associations (like track and field athletics or gymnastics) for school age children can cost thousands per year.

Total: $200 – $XXX+ per year (you can pay as much as you want!)

The cost of pocket money

I think kids should get a little bit of pocket money, or an allowance, for doing jobs to support the house-hold. Whilst I don’t like the idea of training them too hard into selling their time for money (conventional ‘working’), I think this is an overall net gain because they begin to take responsibility with money.

Accordingly, my kids will likely need to plan to cover some of their own expenses; toys, camps, holidays, mobile phones, cars and other luxuries. Of course in the end I will likely chip in or ‘match’ their contributions, but you get the idea.

I will also 100% be following the ‘Barefoot three jar idea’ and encouraging them to live simply and invest themselves in quality items (which they need to look after) and assets from a young age. I think a good starting point is $5-10 per week depending on chores completed, scaling as is age appropriate. I am totally in agreement with the Barefoot though – from around 12 onward, the allowance stops, and it’s time to get a part time job stacking shelves or delivering newspapers.

Come to think of it, I got my shelf-stacking supermarket job as a 14 year old after doing my year 10 work experience at a local shopping center. Before that, I mowed lawns, weeded gardens, washed cars and picked up trash in my neighborhood and local shops to make a buck.

Total: $260 – $520 per year.

The cost of food

Growing kids need to be fed. A lot. My Mum claims she couldn’t afford to feed me anymore and that is why I had to leave home and go off to uni!

From ages 5 to 17, a child’s calorific needs scale from around 1500 all the way up to the standard adult requirement of 3000+ calories a day depending on age, gender and how active they are. I would even suggest that a teenage boy might even consume something similar to my 4000 calories a day, especially if they are cycling or walking to school, training hard, and playing sports.

Using a similar argument for the food calculation for age 2-5, but rather treating them as ‘mini adults’ from age 5 onward that need 66% of my calories on average, that works out to be about $35 in food per child per week.

“$35 per child?!” I can hear some of you shout at your screens! “My child eats more like $35 per meal!”. This might be the case if you’re feeding them scotch fillet and lobster tails, but I plan for my children to eat the same simple diet that I do – a majority (flexible) plant based, whole food diet.

Factoring in the occasional treat and meal out at around $13 per week, this comes out to a total of $2500 per year, per child. This doesn’t factor in any of the savings of growing food at home, which I would estimate to save up to nearly 40% of my current grocery bill some weeks.

Total: $2500 per year

The cost of gifts

This is another massive problem area for many parents who just want the best for their child but honestly results in so much waste. Gifts that I give to my niece, nephews and friends children often receive thanks from the parents, but are a bit hit and miss with the kids. Unless it’s candy or chocolate – in which case the kids love it, but the parents aren’t too appreciative!

I am budgeting around $50 per gift, which realistically would come twice a year: Birthday and Christmas

Total: $100 per year

Summary of cost of school years

For some parents, as their child transitions to school age they might be able to save money previously spent on childcare. However, these costs are also replaced by other increasing costs of Food, clothing, schooling and hobbies and interests like sports. If you choose to send your child to a religious or private school, you can also bank on a significant increase in costs as they begin.

The bottom line

I came out with a sum of $135 per week using my ‘frugal’ FIRE figures. When I looked at average costs, for the average annual income of $82,000 in Australia (per parent) for two parents, using full time childcare, average private health insurance, upper estimates for costs and activities and fully paying public schooling, the figure was much higher at $400 per week, per child. For private school and ‘gold’ standard health insurance, it was shockingly over $1000 per week per child.

Captain FI’s personal family planning budget – One off costs

In terms of one-off costs, I am budgeting $10,000 for wedding (and honeymoon) costs, $2000 for each 9-month pregnancy, $2000 out of pocket for each public health system birth, $2000 for (second hand) baby equipment for my first, and another $1000 for miscellaneous costs for each child. This is a total of $7,000 for baby number one, and then $5000 each thereafter.

My ideal plan would be to space them out every other year, although I don’t really get the ultimate say in the matter. This does not include the cost of IVF or lost opportunity costs for my partner being off work – these figures alone can add up to over $100,000 per child on average! I’m hoping that my partner doesn’t mind being at home with me and the kids too much – but if she wants to go back to work, then I am more than happy to man the fort!

Captain FI’s personal family planning budget – Ongoing costs

As for ongoing costs, I am budgeting an additional $150 per week (per child) or $7800 of annual expenses (for 17 years each) onto my FIRE number, to provide a 10% financial buffer / margin of safety over the initial frugal estimate of $135 per week per child. This brings my FIRE portfolio requirement up by about $91,000 investments per child during stage one (of my three stage) retirement system. This is roughly ‘back of the napkin’ calculated using a draw down of 9% over 17 years, based on the assumptions behind the 4% safe withdrawal rate.

How many kids can I afford?

I want as many kids as my partner will agree to (up to 6), and am also increasingly excited to finally get that Kia Carnival 8-seater minivan I have had my eye on (and budgeted $20,000 for along with the proceeds from selling my current ride).

Overall, for 6 kids, this means around $50K in one-off costs, and an additional $546K in ETF investments, for a total requirement of $593K above what I need to just support myself and a partner. I currently need about an extra half a million, and hope that a good chunk of this will come from my partner’s net wealth, her potential earnings over these next few decades, and of course, the semi-passive income generated from my online business ventures, property investments as well as any part time work in ‘early retirement’ that I might get up to.

But what about holidays?!

Careful readers will note I failed to account for holidays and vacations, which become increasingly more expensive with the number of children you have – perhaps this can be the subject of a future article! I don’t tend to take big vacations since I actually really dislike travelling and all the associated headaches and lines and cues, single-use items and expenses of being away from home. But I do love roadtrips, and travelling to stay with family and friends. Perhaps the Kia Carnival can come in handy for some road trips with the family?

I like to think that we would live on our baseline level of calculated investment returns, and then any spending above this we would need to creatively think ‘How can we afford this’ by embarking on projects or cutting back in other areas.

I also really want to build a life that we don’t need to holiday away from! A lovely acreage, beautiful house, large family and many pets would be something we hopefully wouldn’t want to leave too often!

Closing remarks on the costs of raising a child