Figuring out whether you should rent or buy your home is a big decision, and it’s something nearly everyone will have to deal with at one point in their lives. I’m going to discuss this question through the lens of someone who doesn’t have the financial ability to go out and pay cash for a house; that is, renting compared to a mortgage.

For those that do have the ability to buy housing outright, you may not want to tie up all your capital in a property without using some form of leverage anyway, as you can probably make it work harder for you elsewhere – like as a deposit on another investment property, or in the stock market invested in good quality low fee index fund ETF or LICs.

‘Rent money is dead money’

Rent money is dead money is a pretty common term that gets thrown around in the debate between whether you should rent versus buy. Like anything, you should factor in who is saying something as well as the intent behind what they are saying. In my experience, this is a phrase commonly coined by builders or mortgage brokers trying to promote their business and gain clients.

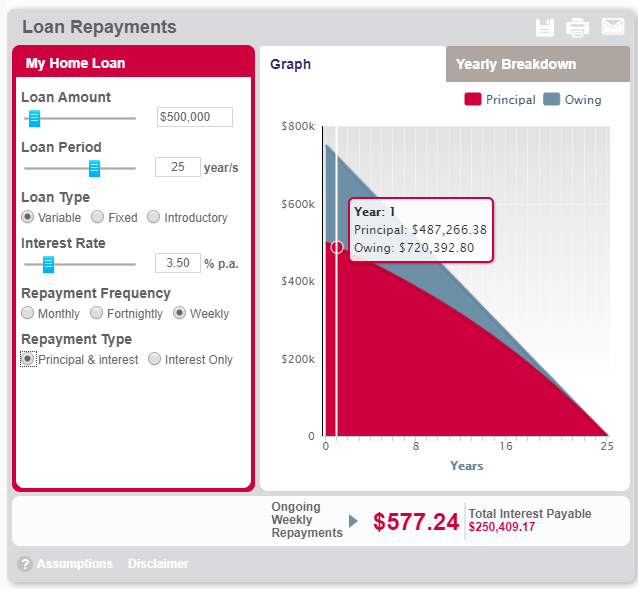

If rent money is dead money, then isn’t interest dead money too? Over a standard 25 year home loan with today’s average 3.5% interest rate on a $500K property, you will actually pay $750K over the period of the loan meaning you’ve been hit with a whopping $250K interest bill!

Of that, you’ll be paying on average $557 per week, every week, for the life of the loan. If you’re buying to live in your home using a standard P+I mortgage, a small (but increasing over time) portion is paying off your principle loan amount, and slowly building your equity. This is kind of like a forced savings plan, but where you can’t do anything with the money.

There are some desirable qualities of a mortgage

- Fixed loan amount

- Loan is in today’s dollars and inflation erodes the future value of the loan

- P+I loan pays down principle at an increasing rate, building equity

- You control the asset from day one and benefit from any Capital growth

- May only have to provide a very small deposit (although 20% is usually the gold standard)

At the end of the day, cash-flow is always king. Regardless if you’re buying a property to live in or as an investment, maxing out your serviceability and spending a high amount of your income on a mortgage is not a good idea. This means you might be cash-flow poor, and the risk of interest rates rising could mean that you can’t afford your repayments. In this situation, you will be forced to sell, likely at a loss!

Why buy a home

- Security for you and your family

- Potential opportunity for capital growth

- Primary Place of Residency capital gains tax exemption

- Don’t have to deal with a landlord – no spot checks or inspections!

- Can renovate to improve quality of life or add value to the property

Why rent

- Flexibility

- Choose where you want to live

- Lower cost of living than owning – no need for building insurance, rates/land tax etc

- No risk of interest rates rising causing mortgage stress

- Known cost to you each week

Rentvesting

So why choose between one or the other when you could do both? You could buy an investment property somewhere where the rental returns are much higher giving you a positive cash flow, and then rent where you want to live. In expensive cities, the rent is almost never in line with rental returns of cheaper areas – meaning you can easily have a great quality of life with an awesome place to live and still be living well below your means.

Cost of renting vs owning

For example, I rent a 1 bedroom apartment in Sydney. It was brand new when I moved in, and the agents had it listed at $430 a week. When I crunch the numbers of what it would cost me to own (with all the hidden costs fleshed out and included), it comes out to just over $530 per week on a 3.5% interest only loan. And what do I get for this extra cost? Stress over interest rates rising, expensive strata fees and cost of repairs, and to make up for all that, I get exposure to some capital growth? Unfortunately the Sydney apartment market has been quite speculative and seen a downturn in price due to a major oversupply – just like other capital cities. Personally, I would leave the city apartment ‘investing’ to the negative gearing ‘specialists’ (or should that be ‘speculators’) and focus on a cash flow positive detached house or duplex investment property instead.

Cash flow

So are there any good cash flow investment properties, and can you get capital gains on them? The answer is yes, but you will need to do your homework. On average a cash flow positive property may experience less capital growth than expected with the more speculative negative gear ‘capital gains’ investment properties that seem to be so popular with high income earners for tax dodging. A decent cash-flow positive property will more likely experience the average capital growth rate of around 3-4%, which means it should outpace inflation and give you a slight increase in equity. It’s easy to say, but difficult to do – you simply have to get out, do your research and see if the deals stack up.

Costs of purchase and ownership

There are a lot of hidden costs and high cost barriers with properties, especially so for investment properties. For example, purchase costs include stamp duty, expensive inspections and legal fees. Similarly, when you sell a property you will incur an agents fee of around 2-3% of the sale price, listing fees, legal fees and capital gains tax on any profits you make.

Buying off the plan or building can be fraught with hidden fees, as builders usually won’t include the cost of landscaping, drainage, driveways or fences in their ‘complete package’. At every step of the way, someone is there ready to sneak their hands into your biscuit tin!

I’ve found a good rule of thumb with ownership is it’s about $100 a week in Australia for a standard 3-4 bedroom home. And don’t expect this to be a passive investment – not at all. You will need to spend considerable time and effort managing your property, even when factoring in paying a full time property manager (that likely charges $1000 per year plus 10% of the rent).

Cash on cash return

Another factor to consider is your cash-on-cash return, and not just the rental yield as compared to your interest only repayments and other holding costs. Realistically, you’ll need a 20% deposit to avoid Lenders Mortgage Insurance and to secure a good mortgage rate, so you’ll be tying up a decent amount of cash in your investment property.

From my numbers, I’ve found good IPs in Australia that can cash flow about $10 a week and cost around $300,000. That requires a $60K deposit, as well as about $10K in fees. So if you’re making 3% capital growth and $520 annual cashflow, that’s a cash on cash return of 13.6%. Not bad – but if there is no capital growth (you shouldn’t bank on it) your return drops to about .7%.

Rentvesting Mk 2

So living below your means is the name of the game to generate your surplus for investment, but if you don’t have a deposit saved up, can’t find a sweet cash flow positive investment property or you just flat out don’t want the stress or risk associated with owning property, then what should you do?

Consistently buy a high quality, low fee index fund ETF or LIC. There is a slight difference between the two, and my preference is the straight ETF like Vanguard total US market or Vanguard Australian shares, due to their lower fees and simple automated trust structure. Having said that, there is a few outstanding LICs with really low fees (AFIC ASX:AFI is $14 per $10,000 invested per year) that have great performance history.

On average, shares have provided a higher return than property, around 10%, and are truly the only form of passive income. I receive my dividends twice a year, print off a tax statement once a year and hand it to my accountant. That’s all I would have to do if I wanted – but I have a regular reinvestment plan (called DCA the Dip!) so I log in to my online broker and purchase a new parcel of index funds every fortnight.

Opportunity cost

With an investment property you can leverage with a mortgage and then hopefully see some good returns for the risk you have taken with the leverage. I would never advocate leveraging with ETFs (called margin loans). In the example above, with a realistic below 3% average capital growth, leveraging rewarded you with a Cash on Cash return of something below 13.6% (and only $520 of that was income taxable, which could be offset by further deductions such as depreciation on the house).

If you simply took that $70K you used to acquire the house, and buy ETFs, on average you’d get about 10%. So that might be $7000, split between dividends and capital growth of the shares. Like property, capital growth on shares is taxed (and if you hold for more than 12 months you get a 50% Capital Gains tax exemption). Similarly, the dividend is like the rent of the investment property, and is taxable as income. Australian shares usually come with franking (tax) credits because they have already paid tax on the companies earnings at the corporate rate – this means your dividends likely will have a significantly reduced tax burden.

The crux of it is that whilst a cash flow positive house by definition is making you money, the capital (deposit and buying fees) you had to use to secure the mortgage might be better invested elsewhere if you don’t get the capital growth you’re aiming for. Housing market crashes are a fact of life and just like the share market the property market is cyclical, but will go up over time. If there is growth, you might be able to make more money than you would if you just bought ETFs by taking advantage of leverage and borrowing money from the bank to control the investment property with a mortgage. Whether you get growth or not, it comes down to buying the right house, in the right area, and paying the right price. All very important skills that take years to learn and sharpen.

Summary

In summary, the decision as to whether to rent or buy is a pretty personal one. For me, I love the flexibility and low cost that renting gives me. It lets me rent an awesome apartment at a significant discount than what it would cost me to own, especially when factoring in the risks of ownership and the pretty grim capital growth prospects for inner city apartments in the over-pumped Sydney property market at the moment.

I consider myself a rentvestor, so I still actively engage in investing. This is mostly through index investing in ETFs but also through the pursuit of cash flow positive, reasonably priced rental properties in ‘cooler’ markets such as regional towns and smaller capital cities. I think this is the best way I can risk manage my approach to reaching FI and getting FIRE’d!

Alternatively, you could follow in the footsteps of Nomad Numbers and slow travel the world, for half the cost of actually working and living at home!

What’s your take? Are you an experienced property or share market investor, and do you rent or buy based on your current living situation? Let me know below!

Get FI!

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.

Thanks for writing this article. My husband and I are trying to decide if we should rent or buy in the area we moved to in the U.S. I love our current rental and the fact that it’s stress free and a fixed cost. We don’t have to keep a certain amount of savings for house repairs earmarked. However, we are paying $17k a year for rent this year and I feel like I’d rather put that to use as building equity in a property. We’re looking at properties less than $250k USD to live in and then eventually rent out and to perhaps accrue properties that way, one after another. On the other hand, I can see putting all of the money we are holding in a high yield savings account waiting for a real estate purchase in index funds and just sticking with the easy peaceful renting route. Hopefully, we can make a decision either way in the next six months.

G’day Faith,

Renting does sound like such a lot of money – doesn’t it! I live in Sydney and my annual rent cost is just over $28K per year for a one bedroom apartment (OUCH!). When I look at how much it would cost to buy this apartment, its actually a market average of $650K. If I stumped up $130K for a deposit, I’d be up for $21K per year in interest only repayments (4%), or just under $30K per year if I was paying back principle plus interest (3% P+I). The real trap is the additional ‘owning’ costs of the apartment which adds each year an extra $8K.

– $4K in strata

– $2K in insurance

– $2K in council rates

This means I can rent the apartment for $28K or I can own it for $38K and be paying it down, a difference of $10,000. Yes while renting I don’t get exposure to capital growth of the asset, but to achieve $10,000 the apartment would need to grow at a minimum of 1.5%, or when including tax ‘grossed return’ a minimum of 2% (due to the tax implication of paying capital gains tax – even at a 50% reduction due to a 12 months+ holding period). On average, over the long term property generally increases at around this rate which is very close to inflation. If it did grow at this rate I guess based on an overall consideration you would be breaking even. The other factor to consider is when renting, you don’t need to stump up the $130K deposit which means this can be invested in either index funds or a separate investment property. Based on the stock markets return of 10%, this would give us at least an extra $13K, or approximately $10,000 after tax return (depending on your tax bracket). This means the difference in opportunity cost between renting and buying is actually $20K, requiring a breakeven capital growth of 4% for the apartment. If you manage to receive the PPOR capital gains exemption then this number would be 3%. It comes down to are you willing to take that risk? Will you sacrifice your cash flow now for potential capital gains later? With the market the way it is in Sydney, I for one would never be buying an apartment (massive oversupply). Money isn’t everything though, and there is some massive psychological benefits to home ownership especially when raising a family.

Interesting thoughts. It all depends on the location really. Buying in New York City? Hell no. Buying further out west in jersey, maybe. Just depends on what the rent is costing vs mortgage. Don’t forget when you pay the mortgage when the house goes up in price you gain equity… with renting you get nothing

Hi,

What about buying house in today’s market in Sydney. We thought of buying couple of years ago but the only options were in West Sydney (40-50km form city) and dropped the idea of buying too far. So, tried to save more for a bigger deposit. But now, the market has again gone up and the prices are going crazy. This makes me nervous and anxious that the way prices are going up! Buy house now and live so far or do not invest and lose potential capital growth considering how the prices are skyrocketing!

Hey Sandeep. It honestly looks pretty scary even just reading some articles or seeing what property spruikers, agents and mortgage brokers are publishing on social media. Its as if you would be crazy to not rush out and buy buy buy or you will miss out now or never haha. I would just sit back, observe and don’t make any rash decisions. If I were you I would be figuring out ways to leave Sydney 🙂