Strategic Asset Allocations can be a source of self-doubt and something any investor can change their mind on, but let’s look at the types of assets and how I manage my investment portfolio strategic asset allocation for my FIRE journey

Strategic asset allocation is important on your FIRE journey because there are just so many ways to invest: ranging from Shares, Cash and Fixed interest, Bonds, Precious metals like Gold, Real estate (both residential and commercial) and Property securities like REITs, even things like hybrids and CFDs, and finally, one of my absolute favorites – digital businesses and websites. But what are they, and in what proportion should I structure them?

This is one of the most agonizing questions when it comes to investing, the question which without a doubt presents the biggest of barrier to entry into investing, and a constant source of self-doubt for investors; Investment portfolio asset allocation. Should I have more stocks than cash, or should I have bonds as well as cash? What about precious metals or other commodities? How do these assets behave, and what is the optimum proportion to hold of each? What should the target allocations be?

This article will explore different asset classes, how to invest in them and how I personally tackle strategic asset allocation.

“The most fundamental decision of investing is the allocation of your assets: How much should you own in stocks? How much should you own in bonds? How much should you own in cash reserve?”

Jack Bogle, founder of Vanguard.

CaptainFI is not a Financial Advisor and the information below is not financial advice. This website is reader-supported, which means we may be paid when you visit links to partner or featured sites, or by advertising on the site. For more information please read my Privacy Policy, Terms of Use, and Financial Disclaimer.

Introduction

In this article, I won’t be reinventing the wheel or suggesting anything crazy, but I will present you with;

- Some of my thoughts on investing psychology and performance

- Different types of assets and how they work

- What I think a sensible investment portfolio asset allocation looks like, and finally;

- How I structure my personal investing portfolio.

Investment Portfolio Strategic asset allocation – CaptainFI’s Opening thoughts…

The following is my ‘Shotgun’ of opening thoughts when it comes to investment portfolio asset allocation, based on my limited understanding of investor psychology, market performance and my journey to FI. These are tidbits, quotes and gems I have come across during my financial education, and a few things I have expanded on or paraphrased as a quick brainstorm when I was asked to write this article by a reader…

- All investing involves risk. High risk = high reward.

- Shares are considered by the conventional financial industry as the riskiest asset class, but history has shown the most risky thing in the long term is actually not investing in them.

- The more years you have to invest, the higher your risk tolerance1 should be.

- The more streams of income you have, the higher your risk tolerance should be.

- Diversification reduces your portfolio risk in a particular asset class, for example geographic diversification i.e. local vs international shares, and concentration risk within a particular asset class – i.e. consider an index tracking ETF which holds hundreds or thousands of companies vs one individual company share.

- Non correlated asset classes tend to move or react differently to changes in economic conditions i.e. stocks vs bonds vs property vs commodities. Whether assets are correlated or not is up for debate!

- Volatility on non-geared equities really means nothing over the long term where it averages out to zero, but can be gut wrenching in the short term.

- Volatility on geared investments (such as leveraged ETFs) can destroy your investment capital very quickly, as the losses are magnified more than the gains due to loss crystallisation – I personally would never touch them!

- Human emotion2 and poor self discipline can drag an investment portfolio’s performance down into negatives very quickly, and eventually totally destroy it. Volatility is usually the trigger, and fear the motivation!

- Recognise that humans for whatever reason seem to be conditioned to hate loss more than they love gain. This results in a natural risk aversion.

- Those who claim to be financial experts, are often not. If you get your financial advice from media such as TV breakfast channels, you probably need to turn the TV off! Don’t listen to the media since their job is to sell sensationalised and exaggerated headlines (clickbait!)

- High fees erode your portfolio’s performance, and the majority of investors in actively managed funds underperform due to this factor in combination with human error in stock picking.

- No one can predict a market crash, and no one can consistently pick stocks.

- It would be very rare that when someone retires that they would never earn any income, sell something or receive money somehow.

- It would be very rare that during a severe market correction that someone wouldn’t be able to ‘tighten their belts’ and reign back their spending a bit.

- Most Finance / FIRE / FI / Investment bloggers make money from their blog which reduces their exposure to sequence of returns risk for their retirement, so take what is said with a pinch of salt and try to get as much independent information as possible to cross check

- Those who are in the accumulation phase need a sufficient emergency fund to cope with the ups and downs of life, but would do best to ensure the maximum of their money possible is invested in productive assets to counter the erosive effects of currency inflation.

- Those who have retired or are in the draw-down phase of life need a stable income to cover their cost of living, so need to hold a percentage of their portfolio as cash or fixed interest to smooth out volatility – I personally keep one year’s living expenses.

- Past performance is not indicative of future performance; the markets might be efficient but they certainly aren’t rational! This is due to human emotion being at play – Fear and Greed

- Most people die with a huge portfolio rather than running out of money

- Your Flex rate3 is the ability to reduce your spending in retirement – having a flex rate greatly improves your portfolio’s probability of surviving your retirement.

Portfolio Assets vs Liabilities

One of the most important lessons in the pursuit of Financial freedom, or FIRE (Financial Independence Retire Early), is to understand the difference between an Asset and a Liability. Put simply, an Asset is something you control that produces you money, and a Liability is something that costs you money.

Think that brand new SUV is an asset because you use it to drive to work and make money? 90% of people would call it an asset and list it as so on a home loan application, but the reality is that 99.9% of cars are a big, fat, liability! They cost you money every week, whilst also depreciating at an average rate of over 20%! Other examples of liabilities include Credit cards and personal loans, hobbycraft like Jetskis and boats, and motorcycles.

On the other hand assets, sometimes called productive Assets (because of the virtue of them producing gains or returns for their owners) come in several classes. The defining feature of income-generating assets is that they can put money back in your pocket. For example, the following investments are most commonly referred to as assets

- Shares

- Bonds

- Gold, and other precious metals and gems

- Real estate

- Collectables: Artwork, Wine, Vintage Cars and Motorcycles, Stamps, Baseball cards

Sometimes though, the lines between assets and liabilities can get blurred – for example if you own your own home (PPOR) do you consider it an asset or a liability? O

Portfolio asset types;

Sensible investment portfolio asset allocation comes down to two key factors – are you in the accumulation or growing phase, or are you in the draw-down or retirement phase?

The Key difference here is that an investor’s risk tolerance (and proportion of cash) will change as they progress from the accumulation to the draw-down phase – logically, you will become more conservative, and need a higher percentage of cash as you get older and progress to the retirement phase.

Now, I will prefix with this discussion that whilst I am by no means an expert when it comes to finance, I have picked up a thing or two during my few short trips around the sun. I truly believe that the MOST riskiest thing you can do when it comes to investing is not to invest. We all know that Fiat currencies are not stable and are not backed by any standard – they are trust currencies, controlled by the central banks and they are designed in such a way that they slowly inflate over time, losing their purchasing power.

This means in our modern fiat currency societies with central banks, if you are not investing, you are doomed to work forever. This means you will never be able to retire. If you do not invest, you will therefore have to rely on welfare to stay alive once you can no longer work. That is not a nice position to be in!

So the question remains, how do I set my portfolio up? What asset mix do I include and in what proportion? Well, it’s incredibly simple. The simplest, more surefire way to reach Financial Independence and to steadily grow your wealth is to invest into two key asset types: Business and Property. Of course, you will still need a small amount of cash (and fixed interest) to ‘cash-flow’ your lifestyle and keep the wheels in motion, but I make a clear distinction that you can’t invest in cash or fixed interest, since this is simply currency – or rather, the absence of investing if you like!

As far as ‘all the rest’ go – it’s simply not worth your time and effort. Precious metals like gold and silver, commodities like barrels of oil, frozen orange juice concentrate, fine artwork, classic cars, vintage wine, antique furniture, jewellery, priceless Ming Vases, stamp collections… They do not put money back into your pocket, they do not cash flow. They only increase in value by proportion of what someone else is willing to pay you for them – otherwise known as the ‘greater fool principle’. I don’t understand these things properly, and I know there is significant cost overheads to store, protect and insure them. Accordingly, ‘investing’ in these types of things is not on my radar!

Furthermore, the concept of trading derivatives, futures, crypto or foreign exchange currencies is even more maddening to me. If there is one thing you take away from this, it is do not even consider it. If a financial advisor suggests to – run away from them as fast as you can, and make sure their hands are out of your wallet before you do!

So, let’s consider the various asset classes / main investment types;

Cash

Cash isn’t really an investment… I guess it’s the absence of investment. Cash has a 100% chance of devaluing thanks to inflation, so it’s not a great place to park lots of money, but you obviously need enough Cash-flow to live. I personally think you need just enough to get by, which means probably around a 6-month emergency fund in the accumulation phase, or 1-2 years of living expenses in the draw-down phase.

A great way to stash cash for a sinking fund (or emergency fund) is to use a High Interest Savings Account or Online Savings Bank Account.

Online banks usually offer the best rates for online savings bank accounts, but you can always choose to invest into money markets, term deposits or fixed-interest funds, too.

If you ask me though, cash is a poor investment and I personally am not holding much cash outside of my mortgage offset and my sinking fund in my ING bank account – I would rather have it invested.

Fixed Interest

Fixed interest investment is essentially a way to get a slightly higher return on your cash – similar to using a high-interest online savings account. When it comes to strategic asset allocation, it is technically a term used for an investment vehicle that provides a return in the form of fixed periodic payments and the eventual return of the principal at maturity.

The main characteristic of a fixed interest investment is that the investor knows with certainty the return they will receive (assuming the issuer does not default). They are generally seen as a fairly low-risk investment. The rate of return can be predetermined (fixed) or it can actually even be variable depending on the interest rate and is often referred to as the ‘interest rate’ or ‘coupon rate’. Fixed interest are investments include things like;

- Term deposits (also referred to as Fixed Deposits or Certificates of Deposits)

- Peer to peer lending such as Plenti peer to peer lending

- Money market funds, and

- Bonds

Term Deposits

Term Deposits are offered by banks or other financial institutions which are Authorised Deposit-Taking Institutions. They typically have a specific maturity date (usually 3, 6, 12 or 24 months, but can be up to 5 years) and offer a fixed interest rate over this time period.

There usually is a higher interest paid for longer term periods (although not always!), and because you are agreeing to lock the money away for a certain time period, there are usually penalties for withdrawing earlier (such as forfeiting interest) so they arent as liquid as a HISA or money market fund.

When they mature, you have the option to withdraw your funds (principal and interest) or renew for another term.

Investors typically use term deposits as a means to preserve capital and earn a fixed return. For example, when they have a known future expense and want to ensure their capital remains intact – especially important if volatile markets are causing anxiety over uncertainty.

Peer to Peer lending

Peer to peer lending (P-2-P or P2P), also known as “crowdlending” or “social lending,” is a method of financing that enables individuals to borrow and lend money directly to each other, without the traditional intermediation of a financial institution like a bank or credit union. Instead, the process is facilitated by P2P lending platforms that connect borrowers with potential investors.

One example that I have used is Plenti peer to peer lending.

Advantages of P2P lending is you can potentially earn higher returns compared to traditional fixed-interest vehicles (such as HISAs, term deposits, bonds or money market funds) as well as you get to diversify your funds across multiple loans.

However there is a higher risk of borrowers defaulting and P2P lending is usually not officially insured, meaning if a borrower defaults that you could lose your principle (you could think of it as a low credit rating bond or Junk bond).

Money Market Funds

Money market funds are ways institutions and individual investors can invest into cash without putting it into a high-interest online saver or term deposit with a bank. Vanguard offer a fixed interest index ETF (Exchange Traded Fund) in Australia – the Vanguard Australian Fixed Interest Index ETF (ASX:VAF), which can be bought or sold just like a share or any other index fund.

Bonds

Bonds4 are a type of fixed interest investment vehicle, and are a similar concept to a term deposit from your bank. You lend your money for a set period of time, and then at the end get it back, with some interest paid along the way. Except it can be a wider range of institutions borrowing your money; for example, governments or companies looking to raise funds. Bonds can also be bought and sold on a secondary market – just the same way shares are sold..

Ever heard of the term war bond? These were issued by the allied governments during the war to raise funds for war fighting equipment, an IOU to the citizens to be repaid back with the spoils of war. Bonds once issued can be bought or sold on a secondary market just like a stock. The thing about bonds is that when the interest rate drops, new bonds come out with a lower coupon rate (they pay less interest).

This means the original bonds, with the higher coupon or interest rate, go up in value. Conversely, if there is high inflation and to combat this the RBA pulls the lever for interest rate increases, older bonds go down in value (because the newer ones pay more interest).

Bonds are also seen as a ‘safe’ alternative to shares, since they pay out a known income – great if you’re a retiree looking for regular grocery money. These factors mean that when the market drops and share prices fall, spooked short term investors (or even institutional investors under pressure from shareholders) may flood into the perceived safety of bonds; making bonds go up in price and showing how stocks and bonds move in opposite directions.

Bonds cover a broad range of investing options, but it typically refers to a fixed-interest contract or loan – similar to a term deposit with a bank. This is one of the ways companies or organisations are able to raise capital to expand their business or fund projects – they borrow it via a bond, with a promise to repay the loan at the end of the term, along with some interest along the way (the other way is by issuing shares in the company).

This interest payment used to be called a ‘coupon’, and the interest was referred to as the ‘coupon rate’, because the bond itself was a physical certificate that could be presented to the bank or financial institution which would be clipped to show that the interest or coupon had indeed been claimed for that period.

Bonds then are essentially loans, and you can enter into these loans in a broad variety of ways. There are corporate bonds issued by businesses and government bonds issued by a government treasury department. These bonds can range in quality and interest (or coupon) rates, typically, along the risk-reward spectrum – the riskier the bond, the higher the interest rate you get paid.

This is because with a risky borrower you might lose your capital (the bond) if they default or their business collapses – so you get paid accordingly more for taking the risk, to try and recoup your investment earlier.

Bonds are typically rated by rating agencies or analyst firms (like KPMG, Morningstar or Fannie Mae) and get allocated a Bond Credit Rating ranging from CCC to AAA scores – although different agencies might use other terminologies such as A- or A+.

“The bond credit rating represents the credit worthiness of corporate or government bonds. It is not the same as an individual’s credit score. The ratings are published by credit rating agencies and used by investment professionals to assess the likelihood the debt will be repaid.”

Wikipedia definition of Bond Credit Rating1

Just like Shares, you can invest in individual bonds through a Securities Exchange like the ASX, or you can get exposure to them through managed funds run by investing firms or banks. You can also access bonds through a bond index ETF, like the Vanguard Australian Government Bond Index ETF (ASX:VGB), or the Vanguard Global Aggregate Bond Index (Hedged) ETF (ASX:VBND) but Vanguard also offer versions of these as wholesale bond index managed fund investment options too.

With the index funds you benefit from broad bond market indexing and the risk of an individual bond defaulting doesn’t bother you too much since any one bond is usually a very small portion of the entire fund.

Recently, when we saw record low interest rates, bond interest rates were excruciatingly low. As interest rates rise, older bonds with lower coupon rates typically drop in value (for bond holders) because new bonds with higher interest rates are issued and these provide a higher income stream to investors – although companies and governments who have secured bonds with lower interest rates obviously benefit from this situation and they can use these ‘cheap loans’ to their advantage.

Some Bond investors choose to invest in the nation directly, buying government-backed treasury bonds – these are essentially an IOU from the government and a form of ‘bank free’ savings account. When a government sells you a bond (IOU) they can then use this money upfront for infrastructure projects or to pay off foreign debts. They promise to pay you back the amount of the bond (called the principle) at the end of the agreement term (called the maturity date).

For your efforts, you are given a fixed rate of interest called a ‘bond coupon’ or the ‘coupon rate’, which is agreed upon when you purchase the bond. This is often referred to as fixed interest in a portfolio.

You can buy bonds from companies too, which is another avenue for them to raise money without having to generate shares and give investors all the associated rights that a shareholder would have over the company. The basic concept is the same: you buy a bond and hand over the principle, and then receive the coupon rate until maturity, where you get your money back.

As an example, if you purchased a $100K bond with a 5-year maturity with a 6% coupon, you would theoretically receive $6,000 every year for five years, and then your $100K back at the end of the fifth year. You can see why fixed interest is such an attractive option for retirees then, who want a known source of income to live on.

So what happens when it goes wrong? This is where it all gets a little tricky. Companies can fail, or default on their debts if it all goes to shit. This might include not paying you your bond coupon rate or even worse not paying back your principle! If this happens, they can go into administration and liquidators could seize a company’s assets to pay off their debts.

It’s a complicated process but usually secured creditors such as banks that lend directly against assets will get paid first (or they take control of assets and then sell them), then will governments, bond owners, and lastly the shareholders.

Companies that are at a higher risk of defaulting will need to pay a higher coupon rate to attract customers to buy their bonds. That’s why treasury bonds from AAA rated nations (such as treasury bills), or other premium bonds normally pay bugger all and have a low coupon rate (such as a low treasury bill rate). More risky bonds, often called Junk bonds – such as CCC rated risky borrowers like start-ups, ‘sub-prime’ mortgage tranches or collateralised debt obligations have a much higher coupon rate.

If you’re keen on learning more about bonds as a financial instrument, plus seeing Margot Robbie in a bubble bath, do yourself a favour and Netflix the movie ‘The Big Short.’

Insurance bond

There is also a form of bond called an insurance bond, or investment bond, which works very differently to a conventional bond or fixed interest contract. It is actually closer to a long-term commitment into a managed fund, and offers some unique tax-effective income structures.

“An insurance bond, also known as an investment bond, is an insurance-related investment vehicle used primarily in the United Kingdom and Australia. The insurance bond is an investment instrument offered by life insurance companies in the form of a whole life or term life insurance policy. Insurance bonds best suit investors who use them for estate planning or who are interested in long-term investing. Also, insurance bonds have some tax advantages.”

Insurance bonds are long-term investments where your money is pooled with other bondholders and invested according to the terms of the bond. Currently, there are some significant tax advantages for high-income earners if you hold the bond for 10 years and meet the conditions of the bond, which can include making additional contributions. GenLife3 is a main provider of insurance bonds in Australia, and there is also a great episode of the Aussie Firebug podcast4 which delves a bit more into this.

Gold (and other precious metals)

Gold does not produce a dividend, but it has been used for thousands of years as a defensive asset and store of wealth. Many people like to own this tangible asset as it is liquid (you can sell it) and offers diversification from other asset classes (the theory being that its price is non correlated to other assets). There are many places you can buy physical gold and keep it in a safe (or under your pillow!), or you can also buy gold stocks on the stock exchange.

I personally don’t have much invested in Gold, other than micro investing through Bamboo, but an easy way to get gold exposure is to buy a Gold ETF.

The best one I found was Perth Mint Gold (ASX:PMGOLD) which you can actually convert to physical gold if you want by surrendering your shares, but other industry experts also recommend ASX:GOLD (I cover an in-depth review of both in my article investing in gold in Australia). Having said that, I prefer having my money invested in profitable businesses through index share ETFs as well as my digital businesses.

Warren Buffet (regarded as the most successful investor in the world) once said he could buy the biggest block of gold around and he could just stand around and marvel at it all day – but it still wouldn’t do anything for him; which is why he is focused on buying productive assets like stocks. Gold is a defensive play, a non-productive asset that is really just a hedge against inflation, a bet against the economy and a tool of fear; in the long term, it underperforms productive assets. But in the short term, it could move in the opposite direction to stocks as people fear an impending crash.

Some people may try and time the market and flip gold; by buying gold and hoping for a stock market crash, they think that gold will go up in value and they will then be able to sell it and buy good quality stocks at a discount. Gold has historically increased in price roughly in line with inflation, so it has been a ‘store’ of wealth when compared to holding cash (fiat currency). Some people go so far as to delineate between money (gold) and currency (fiat dollars).

Well, let’s not start the conspiracy theorist debate about fiat currencies going to zero and Gold being the only safe asset… YES, Gold is money. Gold is a store of wealth. Fiat currency is currency, not money. Gold slowly grows in ‘currency value’ over time because it is a hedge against inflation; as the fiat currency slowly inflates as per Reserve Bank controls, you need more of it to buy the same amount of gold. But the gold itself doesn’t really do anything.

Depending on which time-frames you look at, Gold has outperformed Stocks and other asset classes in the short term, but long term it doesn’t perform as well as other asset classes.

Property

Real estate or property is a huge asset class globally. Everybody needs a place to live, right? and everybody needs a place to work? Real estate can range from something as simple as a small detached (freestanding) house on a block of land, to commercial property such as a towering 100-floor apartment complex, all the way to a giant mega-factory used to produce Boeing Airliner Jets (like in Seattle, USA!)

For some reason, property is more of a religion than an asset class in Australia. There is good reason too – it’s a solid asset class and there are countless hundreds of thousands of Australian investors who have become financially independent by investing in property (there are also a lot who have become bankrupt, too!). I personally made a solid return of over a quarter of a million dollars on my small residential property development investment.

Property is an active investment, and is not as easy and passive as owning stocks. One might even think of property investing as a full-time side hustle or even a personal business! Now property isn’t just property, and the three things you must learn about property when it comes to building your portfolio is of course;

- Location

- Location

- Location

Seriously, as a novice property investor myself, when I came across from regional Australia into the big smoke of Sydney, I almost spat my coffee out when the realtor told me the 1 bedroom 1950s build pokey looking apartment I was looking at was worth over 10 times my yearly take-home wage. It is seriously insane, the hot property market in inner Sydney and Melbourne has fuelled ever-increasing prices, and for the price of a one bedroom apartment there, you could actually buy an entire farm where I am from. It just seems crazy!

“Once you have a property in mind, compare the income you expect to your outgoing expenses. If there is a shortfall, consider whether you can cover the expenses long-term. Also, work out whether you could cover all expenses short-term if you had no tenants for a while. Research the property market to decide how to get an investment property. Where and what you buy will affect your return on investment.”

moneysmart.gov.au/property-investment

The absolute secret weapon when it comes to property investing is leverage. You can buy the asset using the bank’s money, and finance an interest-only loan to help make the property cash flow positive. This in itself is a hedge against inflation, since you’re borrowing today’s dollars and paying them back with tomorrow’s dollars, which have inflated.

Anyway, the point of this is to raise awareness that there are only certain types of property that you should ever consider adding to your portfolio, so these are the four main rules I use to screen investment properties;

- Must be cash flow positive (or at least neutral) – this usually requires good dividend yield

- Must be within 15km of a CBD – this usually results in a good potential upside for capital growth

- Interest only loan with a 80% LVR (20% cash deposit) – this reduces the risk of me defaulting and gets me a better rate

- Ideally, brand new property – this reduces maintenance cost and tenant vacancies, and also gives me a depreciation schedule to save on tax.

Property Securities – Real Estate Investment Trusts

Online investments in property can be pretty daunting for some, but some experienced property investors are more than happy to buy a house online, sight unseen. For beginners though, this is a pretty risky option – an alternative to gain exposure to the property market online is through a share in a Real Estate Investment Trust (REIT)5 – or ‘A-REITs’ as they are sometimes called in Australia.

“REITs allow anyone to invest in portfolios of real estate assets the same way they invest in other industries – through the purchase of individual company stock or through a mutual fund or exchange traded fund (ETF). The stockholders of a REIT earn a share of the income produced – without actually having to go out and buy, manage or finance property.”

reit.com/what-reit 5

These are companies that essentially allow investors to pool their money together and use their collective purchasing power to buy lots of properties – and not just low-cost residential housing either – some A-REITs control some of the biggest and most expensive real estate in the country. These include;

- Retail property: Shopping centers (Malls), Grocery stores, Department Stores, Hardware Stores, Outlet stores and Markets

- Industrial property: Factories, Construction facilities, Warehouses and Logistics / Distribution centers

- Residential property: Freestanding homes, Apartment buildings, Duplexes and Student accommodation

- Office buildings: Office parks and business centers right through to skyscrapers

Some of these are privately owned companies, and some are publicly traded on the stock exchange through the ASX. For Example, the Bunnings Warehouse Property Trust6 (ASX:BWP) controls over (AUD) $2.6 Billion of real estate – which they lease to Bunnings Warehouse7 hardware stores. BWP buys the land, builds the shed, sets the terms of the rental leases, collects the cheque, reinvests some of it into new developments and then distributes the leftover as a dividend to its constituent shareholders.

Not all A-REITs hold property, and some are actually just big development corporations that gobble up cheap land releases through negotiations with councils and state government. Remember, although it seems criminal to gift hundreds of millions of dollars worth of real estate to a company, it is in the government’s interest for land to be developed because the developed land is then subject to council rates and property taxes, providing guaranteed income to the government and councils which can be spent politically.

Developers can then either turn around directly and on-sell this land, ‘land bank’8 (hold onto it because they know it will go up in value) or start developing and seeking legal approvals for zoning and building. The land can be sold for significant profits once development approvals have been made, or once it has been subdivided into smaller lots.

For some projects, developers will work with builders to either sell ‘off the plan’ designs such as residential housing or physically build a site (Apartment complex or shopping center) and then either hold onto the asset or sell it to another REIT, private equity firm or superannuation fund.

This is a highly profitable game, and property development is a major part of the Australian economy9.

There are a lot of other A-REITS that you can check out. Some of the most notable, and probably names you might recognize from banners, construction sites and shopping malls (and rough assets under management) include;

- Goodman Group: (AUD) $55 Billion in assets

- Scentre Group (AUD) $55 Billion in assets

- DEXUS Property Group (AUD) $34 Billion in assets

- Mirvac Group (AUD) $18 Billion in assets

- Stockland Corporation (AUD) $18 Billion in assets

- GPT Group (AUD) $25 Billion in assets

- Charter Hall Group (AUD) $40 Billion in assets

- Shopping Centres Australia (AUD) $3.2 Billion in assets

- BWP Trust Retail (AUD) $2.4 Billion in assets

- Growthpoint Properties Australia (AUD) $300 Million in assets

- Westfield: (AUD) $29 Billion in assets

It is worth noting that the assets under management is different to the market capitalization or size of the company, however it’s pretty impressive!

Personally, I directly invest in real estate where I can use leverage to maximise my cash flow – so I have no need to directly invest in REITs. However, I invest in broad market stock Index funds across global markets, which include some REITs (for example, REITs make up about 3% of the US S&P 500 index).

Business

We can invest in profitable business in two ways: We can buy stocks, or we can start our own business. Starting your own business is a lot of work, can be gruelling, and statistically 9 out of 10 start-ups fail. Still, if you are determined and willing to put in amounts of effort, sweat, blood, tears and long hours, you can make it work and run a successful and profitable business.

If you want to have a go at running a business without all of the risk and overheads of your traditional bricks and mortar physical business, you should check out online businesses. I’ve been running a portfolio of websites for the past 5 years and it has been a very rewarding hobby that has now turned into a small business and provides a great cash flow – check out my articles and podcast interviews with online business owners about making money online .

But if you’re like 99% of people and a bricks and mortar business sounds too hard and you would rather be a passive investor, you can simply buy a partial share in a business through the stock market.

Shares are one of the easiest forms of online investment in Australia. I have written extensively about my experience doing this and how you can buy simple, broad market index funds like Vanguard ETFs (Exchange Traded Funds).

Inside the world of the stock market and stocks, are a multitude of financial products and ways to own them. All you really need to know is that by owning a stock you are owning a slice in a productive (and hopefully profitable) business. A low cost, stock market index fund ETF is easily the best way to take advantage of the benefits of the stock market if you are serious about becoming financially independent, and potential early retirement.

I started my online investing journey in Australia in managed funds (and technically also in my superannuation), transitioned briefly to trying to pick stocks with tips from newsletters (underperforming the market), and then finally made the important realisation that an indexing approach is the safest and smartest method for someone like me to make my online investments in shares.

The concept of shares (also called stocks), and specifically buying of stocks through low-fee index fund ETFs is explained in my articles on Index funds and Investing In Shares In Australia For Beginners.

You can get access to Australian shares by buying ETFs such as Vanguard’s VAS or Betashares A200, or if you’re interested in international markets, you can opt for international shares by buying ETFs such as VEU or VTS.

Once you find a good online share trading platform that you like, it’s very straightforward to set up a buy order to trade online and get shares in your name. Just make sure you keep in mind how much you’re investing and the relative brokerage fees.

You can find guides on how to do this here on the blog, as well as reviews of various online share trading platforms, such as Pearler, Self Wealth and CommSec.

Buying individual stocks can be tempting (and I have done it, and still do hold interests in individual companies), but I reckon by far the best strategy is to buy all of the stocks (Yes, all of the stocks) and use this as either your entire portfolio, or as the ‘core’ of your portfolio (90% or more). It is very simple and easy to do with the advent of ETFs, specifically a total stock market index ETF – these can give you instant diversification into all of the world’s biggest ‘blue chip’ companies for an ultra low management fee. For Example, just using the three Vanguard funds VAS (Australia), VTS (America) and VEU (Total world ex US) gives you instant ownership of thousands of publicly listed companies; practically this is the best outcome anyone could ever hope for.

FIRE portfolios are generally share-heavy – because it is easy to get cash flow from dividends or selling portions of shares. Generally speaking, most people aim to have a large percentage of their FIRE portfolio in stocks, regardless of their age. We are all investing for the long term here, and long term the riskiest thing is actually not owning businesses.

Mutual fund or actively managed investment is where a fund manager actively tries to pick stocks for you – which is basically like throwing darts at a dartboard whilst blindfolded! When it comes to investing I am a smart investor and take my advice from the best – Mr Warren Buffet himself. And what Does Warren Buffet say?

“Buy what is Value, and a low cost stock market index fund practically makes the most sense, most of the time.”

Warren Buffet, CEO Berkshire Hathaway (and the world’s greatest investor)

When investing in stocks (or anything for that matter) you really need to consider the fees and charges involved. Consider that a mutual fund charging 4% is 100 times as expensive as the Vanguard ETF. Vanguard takes only .4% of your profit compared to the mutual fund which takes 40% of your profit. 40% was the average fee to return percentage paid by private investors calculated by Stockspot.com across the entire financial industry in 2019.

Modern ETF funds like Vanguards VTS, VAS and VEU funds have Rock bottom Management expenses. VTS has a management fee of something like .04% or $4 annually for every $10,000 you have invested. An investment this size should on average produce you $1000 of passive total returns each year – meaning your fee is only .4% of your total profit.

Online business – websites

There are many ways in which you can invest in online or digital businesses in Australia, and this can be a very powerful tool to reach Financial Independence if done correctly. I have been experimenting with this over the past few years, building a portfolio of profitable websites myself, and honestly, I have had to pinch myself when I have seen the cheques in the mail and the cash being deposited into my bank accounts.

“The majority of online revenue strategies aren’t that complicated. Like any business venture, your online income takes time to grow. You need to be willing to devote the time and energy required to get your idea off the ground, and you need grit to stick with it even if your journey is slow when you first start out.”

forbes.com/sites10

Let’s cover some of the basics of online businesses in Australia;

There are a few ways to invest in online business in Australia, including;

- Partnering or Investing directly with a start-up or established company that operates in the online space

- Buying a website (digital property) from places like Flippa or Empire Flippers, and monetising it

- Designing, Building and operating your own website (digital property) and monetising it

- Growing a large following on social media (such as Instagram or Facebook) and then monetising it

So what’s the common denominator and easiest way to stay in control? Creating content, getting online traffic, and monetising it. There are many ways to monetize your online business, and examples include;

Advertising partners – Sell advertising space on your website (or social media) to advertising agencies: The easiest way is Google Adsense, and then later you can upgrade to MediaVine for when you have more traffic (MediaVine will pay higher commissions). There are a number of advertising agencies other than these two which can offer bespoke advertising services for unique industries with great commissions. I currently use Google Adsense on all of my sites.

Direct advertising – Sell advertising directly to companies and skip the middle man. I currently directly advertise with some businesses where I charge a monthly flat fee for a banner, side bar or injected advertisement on certain parts of the websites. Ideally, you want to transition from advertising partners like Google Adsense into direct advertising contracts – it makes the site a lot cleaner, and it is more profitable.

Affiliate marketing11 – this is a form of marketing where you refer a product and usually, for each signup or sale, you receive a small commission or bounty. I participate in some affiliate marketing programs, but only where I really like the product.

Affiliate marketing is super easy and the simplest one to use is the Amazon affiliates program where you typically receive 1-8% of the final sales price as a commission. However, remember that affiliate programs aren’t very lucrative, and really you are just making a shit load of money for your affiliates and not much for yourself – so don’t go overboard.

Digital products – You could offer digital products such as courses, guides, coaching or eBooks – this is essentially content that you have hidden behind a paywall. For example, you can download the Aussie FIRE eBook from this website for free when you subscribe to the CaptainFI mailing list – but some other bloggers will make you pay for this.

E-commerce12 – E-commerce covers the selling and shipping of physical products online. Examples include Drop shipping and arbitrage, but you could also work with a partner like Teespring or Redbubble which are Print on Demand services that you could use to sell T-shirts, Stickers or other merchandise which you design. Personally, I don’t do e-commerce anymore because I found it took a lot of time, the risk was high (if a product is crap it will ruin your reputation, and you have very little control over the quality aspect) and I wasn’t very successful.

Lead gen. Lead Generation13 is a very powerful tool where you essentially ‘rustle up’ business for a company. It is essentially a form of affiliate advertising and is typically related to your core blog content or niche. For example, on my Aviation blog, I talk a lot about different flight schools because this is one of my areas of expertise. I get inquiries all the time about what particular school a student should use, or what degree or course they might start. Because the cost of training for commercial pilots can be well over $100,000 and take many years, these referrals are actually quite valuable for the schools.

I am able to sell these ‘leads’ to certain businesses. But it is not just flight schools, we have done this with many other niches such as mechanics and automotive garages and it is very easy to create a business directory or lead generation site for local businesses.

If you want to learn more about online investments in Australia and how to make money online using websites, check out this article explaining how I make money online, as well as my review of the eBusiness Institute.

Collectibles

Collectables are a name I give to a variety of items that might be worth investing in as they are known to appreciate over time faster than inflation. In general though, these collectables do nothing productive but instead, take up space and gather dust as you wait for someone to pay more for them than you did (the greater fool principle). Some collectables like famous artwork can be worth hundreds of millions of dollars and represent an amazing investment from a cultural standpoint, but may incur a serious cost of ownership. A few types of collectable assets are;

- Wine

- Artwork

- Classic Cars

- Stamps

- Coins

- Certain types of memorabilia

- First edition books or papers

For example, a particularly well vintage wine such as Penfolds Grange might sell on release for upwards of $700 a bottle these days, however ten or twenty years later that same bottle (if kept under strict cellar conditions) might be worth substantially more. For example, Penfolds first commercial release of Grange in 1952 was sold at $1 a bottle (a very high price by 1952 standards). Today, nearly 70 years later that same bottle sells for over $16,000 – representing a rate of return of over 15%.

Of course, there are costs and risks associated with storing such items (the wine might spoil, your beanie baby collection could get stolen etc etc) so it’s not all beer and skittles, and personally, I prefer to keep this asset class to a minimum. I think most of those on the path to financial independence are interested to some degree in minimalism and so might be against owning ‘stuff’ like this.

Investment portfolio asset allocation – putting it all together

OK so now we have a bit more of an understanding of a few of the different asset classes, but there are far more out there. How do we put them together to make a portfolio? And then what about further subdivisions within an asset class? Well, this is the crux of the problem.

“Asset allocation is the process of dividing funds between different asset classes including cash, bonds, property and shares. This takes place as spreading resources across different asset classes can help diversify the portfolio’s holdings, which is an important way to manage risk.”

bt.com.au

No one really knows how different asset classes will perform in the future, and those who tell you they do and can quantify risks in the future are either liars or fools. You can get somewhat of an idea by quantitative analysis of old data, but past performance is no indicator of future performance.

What is risk anyway? Risk is conveniently described as the probability that something bad will happen. So can we assign a probability that the stock market will fall or crash? Unfortunately, no one can predict the performance of the market; whilst efficient, it is certainly not rational.

The old data shows that in the long term, investing in stocks is the highest-yielding asset. We can also look at company fundamentals or so-called ‘technical stock analysis’; would you buy a company because they are the ‘next hot stock’ and are tipped to grow massive, or would you buy a company with low debt, great sales performance, a powerful business ‘moat’ (such as trademark or copyright on a novel process) and a track record of increasing dividends? I know what I’d be investing in.

We know the risks associated with trying to pick stocks, and the benefits (financial and psychological) of omitting this process altogether and adopting an index-based investing approach.

But even an index investing approach will still fluctuate and subject investors to some gut-wrenching volatility as the stock market moves and are continually priced every few seconds! At its extreme, volatility can also mean ‘crash’ with a short bear market causing prices to fall by 20% or more within a week or so. Any less than that is usually called a ‘correction’. The good news is that these bear markets are usually short-lived and tend to recover within a few years; which is why a sensible cash buffer, a low cost of living and a diversified stream of passive income will allow your portfolio to be ‘crash-proofed’!

Investment Portfolio asset allocation for the Accumulation phase

During the accumulation phase, it is assumed that you are earning more than you need to live, and rather sensibly stashing away the excess for the future and your retirement (whether that be conventional or FIRE).

You will need a sinking fund for your bills, and a small emergency fund (6 months living costs) to deal with life’s little ups and downs, so that you don’t leave yourself short if you can’t cover it from your income. This will prevent you from being short and having to sell any of your assets, and deal with the associated headaches of potentially selling at a loss, sacrificing future compounding gains, and of course accounting and tax annoyances.

Personally, I used to keep a fairly small amount of ‘cash’ in my emergency savings – usually around $2000 – however this was because I had a fairly reliable source of income, and a very low cost of living. $2000 represented about one month’s living expenses, and proved to be more than enough for my personal circumstances. If you had a less stable income such as self employed or a contract worker, you would likely need to have a larger emergency fund or ‘buffer’, I would suggest between 3 to 6 months of your living expenses which could be closer to or even more than $10,000. These days, I keep closer to two years living costs in my emergency fund!

Forms of cash and fixed interest include high-interest savings accounts, term deposits with banks, Peer to Peer lending, Money Market funds and even Bond ETFs. I personally keep my emergency fund in my mortgage offset account, and avoid any term deposits or bonds because in my opinion that defeats the purpose of an emergency fund – I can’t access them quickly or penalty-free.

Because you are in the accumulation phase with strong income-earning potential, you can afford to take on extra risk – so I personally take on geared investment properties. Your wage or income usually gives you the serviceability to support a couple of investment properties, but eventually the bank will ‘cut you off as you reach your max – it all depends on personal circumstances but for the usual punter its usually around $1M of debt or 3 to 4 properties.

To summarise: A sensible allocation for the accumulation phase might include one or more cashflow neutral or positive (positively geared) investment properties that meet the sensible criteria, as much in ETF (or LIC) index funds as you get your hands on, online businesses, and a small cash buffer or emergency fund in a mortgage offset account, high-interest savings account or P2P lending platform to keep the wheels turning smoothly, the size of which depends on your personal circumstance such as family, cost of living and reliability of your wage – smaller emergency funds mean you have more invested but are at higher risk for emergencies where you are needing a lot of cash (or perhaps you find yourself out of work).

Investment Portfolio asset allocation for the Drawdown phase

So how long does your capital need to last you? Well, if you’re anything like the average retiree you are going to retire at 65, and probably live at least another 20 or 30 years. We all know of the Trinity study and the 4% withdrawal rule or safe withdrawal rate to know how much we need to have invested, but what about the proportion of stocks and bonds? What about if you are FIREing and retire at 30 – You might have another 65 years ahead of you! Does that change the portfolio allocation drastically?

The simple answer is No – it doesn’t really change. We want to continue investing in profitable business and real estate for the long term, and continue enjoying our reliable dividend and rental yields whilst experiencing good upside potential for capital growth. Depending on your personal circumstances and future plans for your portfolio, you begin slowly selling off chunks of your portfolio to fund your retirement at your chosen rate, but will however, want to increase the amount of cash you keep on hand to a more ‘comfortable’ level for your personal circumstance or ‘stress’ level.

Recent research and updates to the trinity study using Monte Carlo mathematical simulations confirms this. Using the most up to date data, they show that over time the addition of fixed interest such as cash, bonds or P2P lending to your portfolio lowers your success rate – i.e. increases the risk to your portfolio that you will run out of money before you die!

[Source https://thepoorswiss.com/updated-trinity-study/]6

However, those who have retired or are in the draw-down phase of life need a stable income to cover their cost of living, so they need to hold a percentage of cash or fixed interest to smooth out volatility. This cash or fixed interest causes a bit of portfolio drag, but it ensures they don’t have to sell shares at a big loss if the market drops sharply in a bear run – because they obviously still have bills to pay, and it’s likely dividends might be cut. As they draw down their cash reserves over a certain period the market ideally recovers and their dividend payments bounce back, and we are back to bull market conditions.

From the graph above you can see that over a 30 year period, there isn’t actually THAT much difference between a 100% stock and a 75% stock portfolio – Point of note here, the word ‘Stock’ could be thought of as being representational of ‘that which is not cash’. As you increase the time-frame the negative effects of ‘bonds’ becomes more apparent meaning for longer time-frames, you want as LITTLE fixed interest as possible – just enough to keep you feeling comfortable and satisfy your cash flow requirements.

Suggestions to get started working out what a sensible percentage of cash or fixed position is for you could be;

- Your age divided by 5,

- 10% of your investment portfolio, or;

- One to Two years of your living expenses*

*This is the best option of them all, because this depends on your cost of living and therefore is the closest metric to what you might actually need!

Depending on your appetite for risk, most people in the retirement phase like to consolidate and remove debt, for example selling investment properties and taking the profits, paying off the mortgage completely, or simply paying down the mortgages to a level that makes you feel more comfortable or they become positively geared and you can begin to live off rental payments. Whilst we know technically keeping an interest only loan forever and never paying off the debt is the smartest way from a business or purely monetary point of view to own property, this can be an unacceptable level of stress for a retiree. Investment properties are still a lot of work though, so maybe that should be pseudo-retiree!

Crash proofing your investment porfolio

While you can’t predict a crash, you can’t really ‘crash-proof’ your portfolio – the capital value of your shares will go down! The trick here is just not to sell them when they have gone down; don’t worry about the price – capital values are irrelevant if you don’t plan to sell anyway and are looking to dividends for income.

Consider dividend yield; during the 2008 Global Financial Crisis, share prices dropped around 50%, but their dividends were only cut by around 20% – hence why investors in Aussie Dividend shares like Peter Thornhill were not really that worried – the old school ‘Grand-daddy’ Listed Investment Companies he had invested in continued to churn out pretty solid fully franked dividends. Further, a solid cash buffer accounts for the reduced dividend during such a market recession, and you can draw this down until such time as the dividends or market recovers.

There is no magic solution, there is no reward without risk. If you want to think you have a magic solution, go pay a financial advisor heaps of money to get a false sense of security. They will tell you to invest in non-correlated asset classes like the ‘all weather portfolio’… In reality, in my limited experience and opinion, the best you can do is invest in all equities and keep a sensible cash buffer to even out the volatility; maybe a year or two of expenses. The more important thing in this equation is to be frugal and keep your expenses low.

Keeping this cash buffer is the key to not having to sell during a market downturn when you’re in the drawdown phase. As you transition from the accumulation phase (where you only need a very small cash buffer due to your regular high income) into the drawdown phase, you might consider a small holding of bonds or fixed interest to complement your emergency cash buffer.

Flex Rate – your ability to tighten your belt

Your flex rate is your ability to either tighten your belt or earn a bit extra when the going gets tough. By being able to reign in your spending, earn some income (or a combination of the both), you can massively increase your portfolio’s chance of success – that is, ensuring your portfolio outlives you. The flip side to this means that when you factor in your flex rate, you can then draw down your portfolio at a higher withdrawal rate for the same risk of portfolio success (or failure if you are a pessimist!). And a higher drawdown rate means you can fund your retirement with a smaller nest egg meaning you can retire (or semi-retire) sooner – making flexibility a key element for early retirement planning.

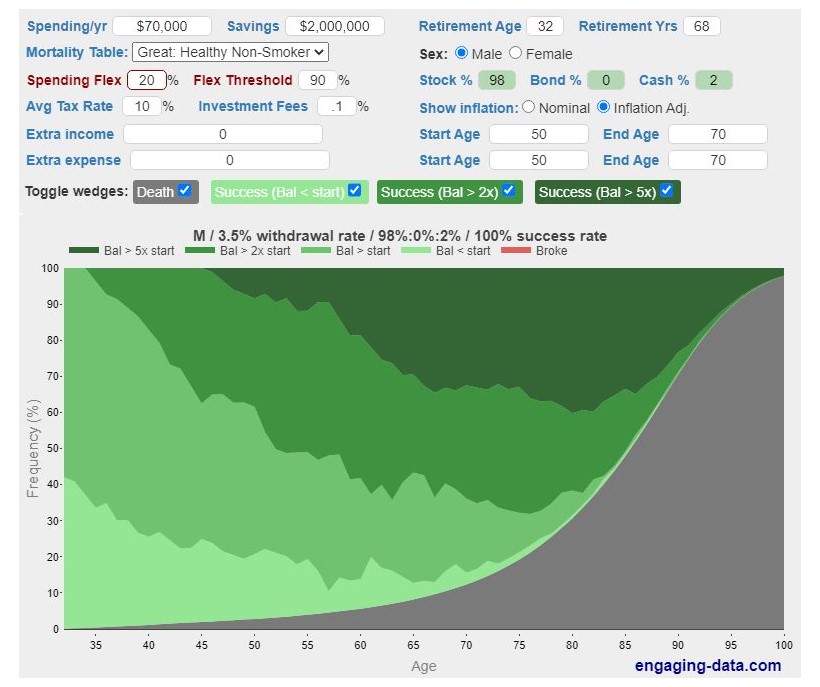

This online tool from https://engaging-data.com/will-money-last-retire-early/7 is amazing and allows you to visualise your spending with a huge array of inputs. For example, I have input some of my current details below (based on the Family FIRE lifestyle) to see the chances of portfolio success. The lack of ‘RED’ colour shows that for this portfolio, there is a 100% success rate meaning I will NEVER run out of money – this won’t ever happen at a 3.5% withdrawal rate at a 20% flex rate.

If I adjust the spending/yr up to $80K (4% rule) there is now a 94% success rate with only a sliver of red seen – however, if I increase my flex rate to 30%, this completely disappears and my portfolio success rate goes back up to 100%! Fun to play around with. This calculator also crucially shows the result of factoring in extra income (and expenses) for certain age periods – such as costs of raising children, or potentially the aged pension.

CaptainFI’s Investment Portfolio Asset Allocation Strategy

So How do I do it? Check out the above graph, or read over my Investing Strategy or Monthly Net Worth Updates to see exactly what I am doing and exactly what is in my portfolio right now. To use a bit of a misleading finance lexicon I am ‘very aggressive’ because I own mostly Shares (index fund ETFs), Businesses and Property – both within my Superannuation and in conventional brokerage accounts.

Summary of Investment Portfolio Asset Allocation

Hopefully this helped you understand some of the options available for you to invest your money. Investing is very different for everyone and the best way for you to invest will depend on your personal financial situation as well as the reasons you’re wanting to invest, your risk tolerance and your time frame for investing.

I hope this article has reiterated the importance of investing smartly for the long term in profitable and productive assets like Businesses and positively geared property8, and avoiding speculative investments like gold, frozen orange juice concentrate or Ming Vases (or even worse, trying to day trade!).

I also hope that you are aware of the drag penalty of holding too much cash, and how inflation destroys you when you do it. Of course, investing is a very personal thing and there is no one size fits all solution, so decide on your investment objectives, give it a go and find out what works best – Let me know in the comments what works for you!

Personally, I am not a financial adviser, but I do not invest in bonds and didn’t keep a lot of cash on my journey to FIRE. I think a disciplined investor could just stay completely exposed to stocks and keep a healthy savings buffer of cash to get them by in any economic downturn (which on average are incredibly short-lived). By any measure, someone chasing financial freedom should be throwing as much as possible into growth assets such as stock ETF and good quality real estate as much as possible rather than defensive plays such as Cash, gold or fixed interest.

Personally, I prefer to invest in good quality and low-fee stock market index fund ETF, real estate like my rental property and websites, over say Gold or collectables. I prefer to have my money invested in productive assets which are making the world a better place, and which have very low overheads or cost of ownership. I also value portability which is a major advantage an ETF has over something like a wine collection (plus I’d probably just drink the wine!).

The FIRE movement is becoming increasingly popular but just remember, financial independence means different things to different people. It’s always best to do your own research, and if you want further advice regarding what to invest in, it may be best to seek advice from a professional such as a financial advisor.

Captain FI is a Retired Pilot who lives in Adelaide, South Australia. He is passionate about Financial Independence and writes about Personal Finance and his journey to reach FI at 29, allowing him to retire at 30.